Employer-sponsored retirement programs tend to be nuanced. That said, there are generally two types of plans: defined benefit and defined contribution.

While cash balance plans fall into the former camp officially, they operate more like a hybrid of the two.

What Are Cash Balance Plans?

In the simplest of terms, a cash balance plan is a defined benefit plan that also includes a contribution element. Under this plan, employees receive a guaranteed amount when they retire — which makes it a defined benefit. Moreover, employers make fixed contributions to employee accounts each year according to a predetermined formula — drawing similarities to a contribution plan.

However, unlike other plans, these contributions and account balances are “hypothetical” until a participating employee leaves the company, at which point the employee can receive a lump sum or begin receiving annuity payments.

How Do Cash Balance Plans Work?

Under a cash balance plan, eligible employees have hypothetical account balances that grow annually through pay credits and interest credits.

- Pay Credits: Employer contributions, which are typically a percentage of a salary.

- Interest Credits: Guaranteed interest on the account balance, which could be a fixed rate or tied to an index, such as 30-year treasuries.

For instance, a 50-year-old executive earning $300,000 annually works at a company that offers a cash balance plan with a 6% pay credit and a 4% interest credit. Each year, the employer adds a pay credit of $18,000 (6% of $300,000) to the employee’s hypothetical account, and the balance earns a 4% interest credit.

![]() Employer contributions are pooled and invested by the plan trustee, as opposed to individual employees governing their own portfolios like in a 401(k). The plan trustee will manage these assets to, ideally, generate a return that’s in line with or above interest credits. Excess amounts can be used to lower future employer contributions, while shortfalls would necessitate higher contributions in subsequent years.

Employer contributions are pooled and invested by the plan trustee, as opposed to individual employees governing their own portfolios like in a 401(k). The plan trustee will manage these assets to, ideally, generate a return that’s in line with or above interest credits. Excess amounts can be used to lower future employer contributions, while shortfalls would necessitate higher contributions in subsequent years.

Cash balance plans are typically more predictable and dependable than defined-contribution plans, but they’re also more complex to administer and often require an actuary to do so properly and compliantly.

How Cash Balance Plans Compare to Other Retirement Plans

Cash Balance Plan vs. Traditional Pension Plan

While both are defined-benefit plans, traditional pension plans are based on an employee’s total years of service, often with an emphasis on end-of-career earnings. In other words, they’re backloaded.

Traditional plans are designed to incentivize employees to stay long-term with one employer, whereas cash balance plans are portable and, in that sense, can be more employee-friendly.

Cash Balance Plan vs. 401(k) Plan

With a 401(k), retirement account values are directly tied to market performance. Employees contribute pre-tax dollars, choose investments, and hope for growth. In contrast, cash balance plans offer a predictable, employer-guaranteed benefit — employees don’t bear the investment risk; employers do. That means that these accounts are typically invested very conservatively, predominantly in low-risk fixed-income securities.

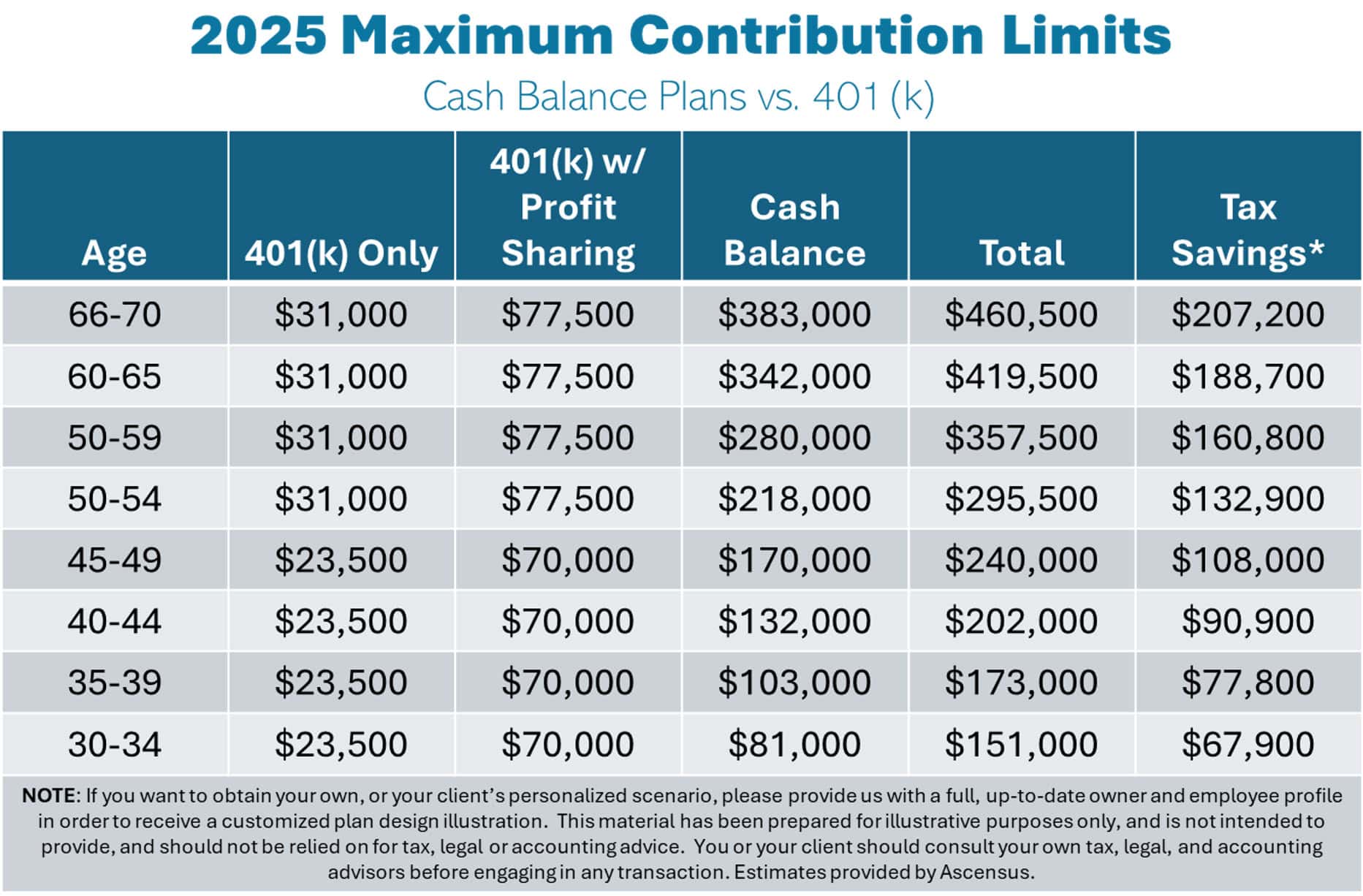

One of the biggest advantages of cash balance plans over 401(k) plans is the contribution limit. For high earners, cash balance plans allow for much higher annual contributions.

The Pros and Cons of Cash Balance Plans

Pros For Employees

- Higher Contribution Limits: Cash balance plans allow for much larger annual contributions compared to defined-contribution plans. Employees (especially high earners) can set aside considerable retirement contributions in a relatively short period of time.

- Tax Efficiency: Contributions are tax-deferred, which can help significantly reduce taxable income.

- Predictable Benefits: The defined benefit structure bakes in guaranteed growth, providing certainty around retirement funds.

- Reduced Investment Risk: Employers are responsible for making contributions and managing participant plans — not employees. In turn, employees do not bear the investment risk.

- Portability: Like 401(k)s, vested balances can be rolled over into an IRA or another employer’s plan if an employee changes jobs.

Cons For Employees

- Complexity: Cash balance plans are, in general, more complicated than other standard plans, such as a 401(k). Employees may need to work with a financial professional to assess their individual plan.

- Capped Upside: Due to their fixed nature, cash balance plans do not allow plan participants to manage their accounts and possibly achieve outsized returns.

Pros For Employers

- Key Employee Retention: The predictable, tax-efficient, and high-earning nature of cash balance plans can appeal to key employees and, as a result, help retain them.

- Tax Deductions: Employer contributions are tax-deductible, which can significantly reduce the company’s taxable income while rewarding owners and employees.

- Plan Flexibility: While plans must satisfy nondiscrimination testing, they can be structured to offer tiered benefits based on position, tenure, and performance.

- Cost Predictability: Cash balance plans provide more predictable costs compared to market-dependent 401(k) plans, enabling companies to manage financial commitments more effectively.

- Plan Combination: Cash balance plans can be combined with 401(k) profit-sharing plans to help facilitate substantial tax-deferred savings.

Cons For Employers

- Complexity: Setting up and maintaining a cash balance plan can be complex and may require additional administrative resources and expertise, such as an actuary.

- Funding Requirements: Cash balance plans must meet minimum funding requirements, as mandated by the IRS. Consequently, these plans may not be suitable for companies with unpredictable or volatile cash flows.

Special Considerations and FAQs for Cash Balance Plans

Who benefits the most from cash balance plans?

While they must comply with nondiscrimination testing, these plans can favor high earners on an absolute dollar basis, potentially enabling substantially higher retirement contribution limits.

For employers, cash balance plans are ideal for mature businesses with sustainable profits and stable headcounts.

Are cash balance plans insured?

Cash balance plans are usually protected by the Pension Benefit Guaranty Corporation (PBGC), which insures benefits up to certain limits.

How long do cash balance plans take to vest?

Employee benefits in a cash balance plan must fully vest by no later than three years of service.

For additional information about cash balance plans, visit www.lindenthomas.com, or call (704) 554-8150.

*(Plan Limits) $23,500 for 401(k) plan; $7,500 catch-up (age 50 or older); $46,500 profit sharing. Amounts shown in the chart do not include the additional catch-up contributions for participants aged 60-63. This hypothetical chart assumes a 45% tax bracket of combined federal and state taxes and taxes are deferred. The following assumptions also apply:

- Maximum annual contribution amounts for the cash balance/defined benefit plan are calculated using 4% interest rates and assuming no pre-retirement mortality and using the latest available applicable mortality tables.

- The maximum cash balance amounts assume a 3-year average compensation of at least $280,000 (the maximum annuity limit for 2025), and prior years of service.

- The amounts needed to fund the cash balance/defined benefit plan may be reduced by a participant’s prior highest 3-year salary history if it is less than the IRS maximum annuity limit (as shown above) or below the IRS maximum compensation limits under 401(a)(17) (e.g., $350,000 for 2025, $345,000 for 2024, etc.) and other deduction limits may apply.

- The amounts needed to fund in the cash balance/defined benefit plan will also be reduced if a participant participated in any prior cash balance/defined benefit plan of the employer or a related employer.

- Further, amounts shown may be reduced if the cash balance/defined benefit plan is not covered by the Pension Benefit Guaranty Corporation (PBGC), which may limit the amount available to fund in any paired 401(k) profit sharing plan of the employer. (Plans typically not covered by the PBGC are professional service businesses with fewer than 26 active participants.)

- It is also important to note that amounts shown are estimates and will vary depending on an employer’s demographics of owners and employees along with a myriad of other factors and considerations.

Important: if you want to obtain your own, or your client’s personalized scenario, please provide Linden Thomas & Company with a full, up-to-date owner and employee profile in order to receive a customized plan design illustration.

This material has been prepared for informational and illustrative purposes only, and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. You or your client should consult your/their own tax, legal, and accounting advisors before engaging in any transaction.