It’s easy to put off saving for retirement, especially during the lower earning years of your career. However, it’s critical to remember that no matter how little you’re earning, it is never too early or too late to start contributing to retirement accounts like a 401(k). Whether you’re balancing debt repayments, building up an emergency fund or prioritizing other financial goals, it can still make financial sense to contribute to a 401(k).

How Much Do You Need to Earn Before Contributing to a 401(k)?

There is no set amount you need to earn to begin 401(k) contributions. This means you don’t have to wait until your earnings increase to kickstart your savings. You do have the freedom to decide how much of your income goes into your 401(k) whether that’s 1% of your salary or 15% or more. The ultimate consideration is how much you can afford to contribute after factoring in your other expenses and financial priorities. While it’s recommended people contribute 10%-15% of their income to a 401(k) annually, do what you can afford. Contributing any amount is better than contributing nothing and ensures your money is housed in a vehicle where it can compound and have growth potential.

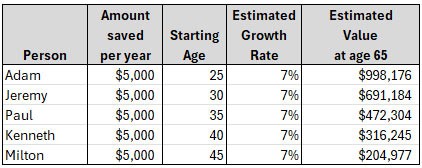

The table below (Exhibit 1) illustrates the stark contrast that exists when a person starts contributing in their mid-20’s versus their mid-40’s:

Exhibit 1: Comparison of compounding, with various starting ages

In terms of plan qualifications, there are only two, which include being at least 21 years old and having at least one year of service with an employer. That said, there are contribution limits. The most you can contribute to a 401(k) is $23,000 in 2024 and $30,000 for those 50 and older, but you don’t have to contribute the maximum.

Utilizing Dollar Cost Averaging Opportunities

Another reason to consider contributing to a 401(k) no matter how much you earn is because of dollar cost averaging (“DCA”). This is an investment strategy that involves regularly investing a set amount of money into a security or portfolio regardless of the price. The goal is to reduce the impact of market fluctuations (volatility) on your investments by buying more shares at lower prices and fewer shares at higher prices. DCA can help investors avoid the risk of investing a lump sum at potentially higher prices, which can help an investor build wealth over time by consistently adding money to the market. Adding the same amount of money at regular intervals can help investors avoid the temptation to time the market and make predictions about price movements. Remember that DCA is a risk mitigation strategy and not one that attempts to maximize an account’s return.

When the market is experiencing downward swings, you may end up getting shares for cheaper or at a ‘discount’ because of your consistent purchase of shares. But as we have stated in previous articles, markets generally tend to increase, and if they go up during the time you are employing a DCA strategy, you might miss out on potential gains you could have had if you had invested the whole amount in one fell swoop. But when you are investing consistently in a 401(k), your investing money as you earn it, which negates this potential concern. One thing is certain, waiting until you earn a certain amount before you contribute to a 401(k) could mean missing out on potential market opportunities.

Making The Most Of Employer Matches

Some employers will match what you contribute up to a certain amount, essentially giving you free money. Finance experts recommend at least contributing the minimum to a 401(k) to take advantage of potential employer matching. For instance, an employer may match 100% of what you contribute up to, say, a cap of 6% of your salary. That means if you earn a salary of $75,000 annually, your employer will match you up to $4,500, which is 6% of your salary. To get the full benefit of the $4,500 from your employer, you’d need to contribute 6%, which is $4,500 to your 401(k) for the year. Even if you can’t afford to contribute enough to get the full match, getting a partial match still ensures you secure some free money for your retirement account.

No matter how much you earn, it can be good to leverage that “free” money from your employer. Using the matching example above, if you waited until you were earning six figures before contributing and that took three years, you would lose out on $13,500 of “free” money during that period.

If you need help deciding how much to contribute to a 401(k), consider reaching out to a financial professional today.