For affluent investors and families seeking to protect their wealth, minimize taxes, and ensure a smooth transfer of assets, trusts are a fundamental component of estate planning. Among the different types of trusts, an irrevocable trust offers unique advantages and protections that other estate planning vehicles do not.

What Is an Irrevocable Trust?

An irrevocable trust is a legal entity that holds assets for the benefit of designated beneficiaries while being managed by a trustee. Unlike a revocable trust, an irrevocable trust cannot be modified, amended, or revoked once it is created, except under very specific legal circumstances. This finality is what makes it so powerful–it removes assets from your taxable estate, protects them from creditors, and ensures long-term financial planning strategies remain intact.

Why Would Someone Use an Irrevocable Trust?

Wealthy individuals often use irrevocable trusts for one or more of the following reasons:

- Estate Tax Reduction – Assets placed in an irrevocable trust are removed from the grantor’s taxable estate, helping to reduce estate tax liability. Given the federal estate tax exemption in 2024 is $13.61 million per individual ($27.22 million per married couple), affluent families may find irrevocable trusts crucial in mitigating tax exposure.

- Asset Protection – Once assets are transferred into an irrevocable trust, they are no longer considered the grantor’s property. This means they are generally shielded from lawsuits, creditors, or other financial threats.

- Medicaid Planning – Individuals planning for long-term care may use an irrevocable trust to structure their assets so they qualify for Medicaid benefits without having to spend down their wealth.

- Charitable Giving – Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs) – both sub-categories of irrevocable trusts – allow individuals to donate assets while receiving tax benefits and income distributions.

- Legacy & Control – Unlike outright gifts, an irrevocable trust allows the grantor to control how and when assets are distributed, ensuring financial discipline and multigenerational wealth preservation.

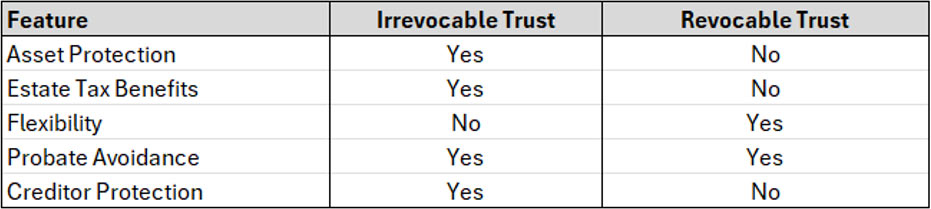

How Irrevocable Trusts Compare to Other Trusts

Irrevocable trusts differ from revocable trusts in several key ways:

While a revocable trust provides flexibility and avoids probate, it does not offer the tax and asset protection benefits that an irrevocable trust provides. High-net-worth individuals often leverage a combination of both trust structures to balance control and protection.

Pros & Cons of Irrevocable Trusts

Pros:

- Reduces estate tax liability by removing assets from the taxable estate.

- Protects assets from lawsuits and creditors.

- Ensures financial discipline by controlling distributions to beneficiaries.

- Can provide income benefits, particularly with CRTs or Grantor Retained Annuity Trusts (GRATs).

- Helps with Medicaid eligibility for long-term care planning.

Cons:

- Loss of control over assets once transferred.

- Complexity and legal costs associated with setting up and maintaining the trust.

- Irreversibility, making it difficult to make changes if financial or personal circumstances change.

- Potential gift implications on tax returns if contributions exceed the IRS’s annual gift tax exemption limit ($18,000 per recipient in 2024).

Hypothetical Examples

Let’s examine a few real-world scenarios demonstrating the power of irrevocable trusts:

Example 1: Estate Tax Planning

John and Susan, a married couple, have a total estate worth $40 million. If they pass away in 2024, their estate tax exemption ($27.22 million) leaves $12.78 million subject to federal estate taxes, which could result in a tax bill exceeding $5 million. By transferring $10 million into an irrevocable life insurance trust (ILIT) – a relatively popular sub-category of irrevocable trusts- they remove those assets from their taxable estate, significantly reducing their estate tax liability.

Example 2: Asset Protection

David, a surgeon with a net worth of $5 million, worries about potential malpractice lawsuits. By placing $2 million in an irrevocable trust, he shields those assets from potential future claims, ensuring his family’s financial security.

Example 3: Medicaid Planning

Barbara, age 65, owns a home worth $800,000 and has $500,000 in savings. She transfers these assets into an irrevocable Medicaid trust to start the five-year look-back period, which is required for some irrevocable trusts. After five years, these assets are no longer counted for Medicaid eligibility, allowing her to qualify for long-term care benefits without depleting her estate.

Is an Irrevocable Trust Right for You?

For affluent individuals and families, an irrevocable trust can be a highly effective wealth preservation tool. However, because of the complexity and permanence of these trusts, it is critical to work with an experienced financial advisor who understands tax-efficient estate planning strategies.