When planning for retirement, it’s essential to understand the various savings vehicles available and how they align with your financial goals. Two prominent options are the 401(k) plan and the Simplified Employee Pension Individual Retirement Account (SEP IRA). While both offer tax-advantaged growth, they differ in structure, contribution limits, and suitability depending on your employment status and business structure. Let’s delve into these differences to help you determine which plan might be more appropriate for your situation.

Understanding the 401(k) Plan

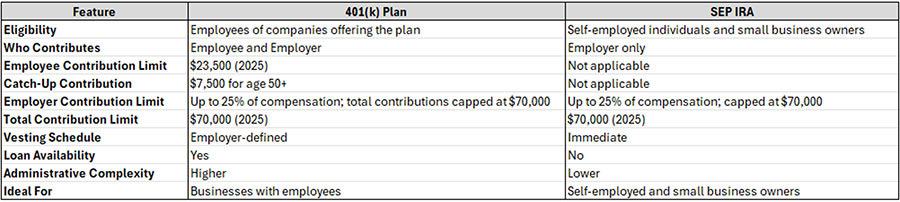

A 401(k) is a retirement savings plan commonly offered by employers to their employees. As an employee, you can elect to defer a portion of your salary into this plan, reducing your taxable income for the year. Employers often enhance this benefit by offering matching contributions, effectively augmenting your retirement savings.

For 2025, the contribution limits are as follows:

- Employee Contribution Limit: Up to $23,500.

- Catch-Up Contributions: If you’re aged 50 or older, you can contribute an additional $7,500, bringing your total potential contribution to $31,000.

- Combined Contribution Limit: The total of employee and employer contributions cannot exceed $70,000.

One notable feature of the 401(k) is the option for participants aged 60 to 63 to make “super catch-up” contributions. Starting in 2025, this allows for an additional $11,250 in contributions, further enhancing the plan’s appeal for those nearing retirement.

Exploring the SEP IRA

The SEP IRA is tailored primarily for self-employed individuals and small business owners. In this arrangement, only the employer makes contributions on behalf of eligible employees, including themselves if they are self-employed. Employees do not contribute to this plan.

Key aspects of the SEP IRA include:

- Contribution Limits: Employers can contribute up to 25% of an employee’s compensation, with a cap of $70,000 for 2025. For self-employed individuals, this typically translates to about 20% of net earnings.

- Vesting: Contributions are immediately 100% vested, granting employees full ownership of the funds upon contribution.

- Flexibility: Employers have the discretion to decide whether to make contributions each year, providing flexibility based on the business’s financial performance.

Comparing the Two Plans

When deciding between a 401(k) and a SEP IRA, consider the following factors:

- Eligibility and Participation: A 401(k) is generally suited for businesses with multiple employees, offering both employer and employee contributions. In contrast, a SEP IRA is ideal for self-employed individuals or small business owners seeking a straightforward retirement plan without the complexity of employee deferrals.

- Contribution Potential: The 401(k) allows for higher total contributions when combining employee deferrals and employer matches, especially advantageous for those aiming to maximize their retirement savings. The SEP IRA’s contribution is solely employer-funded, which may be limiting if the employer’s profits fluctuate.

- Administrative Complexity: SEP IRAs are renowned for their simplicity and low administrative burden, making them appealing for small businesses. 401(k) plans, while offering more features, come with increased administrative responsibilities and potential costs.

- Loan Provisions: 401(k) plans often permit loans, allowing participants to borrow against their savings under specific conditions. SEP IRAs do not offer loan provisions, meaning funds are generally inaccessible without penalties until retirement age.

Conclusion

Choosing between a 401(k) and a SEP IRA depends on your specific circumstances, including your employment status, business structure, and retirement savings goals. If you’re a self-employed individual seeking a simple, flexible retirement plan with high contribution limits, a SEP IRA may be appropriate. Conversely, if you own a business with employees and wish to offer a robust retirement plan with both employer and employee contributions, a 401(k) could be more suitable.

It’s advisable to consult with a financial advisor to assess your unique situation and determine the most beneficial retirement plan for your needs. They can provide personalized guidance, ensuring your retirement strategy aligns with your long-term financial objectives.