“US Debt Downgraded” sounds ominous. But the reality is more nuanced.

On May 16, Moody’s officially joined Standard & Poor’s and Fitch in downgrading the US government’s credit rating, lowering it one notch from Aaa to Aa1.

While a downgrade is never ideal, an Aa1 rating is still a very high credit quality. The US Treasury market is among the largest, most liquid, and most trusted in the world. And although the move underscores legitimate issues, it doesn’t imply the country is at risk of default.

Let’s break down what the downgrade actually means, what prompted the decision, and why investors can largely take it in stride.

What Is a Credit Rating and Why Does It Matter?

Credit ratings are essentially report cards for borrowers — and in this case, the borrower is the US government.

Assigned by major credit rating agencies like Moody’s, S&P, and Fitch, these ratings assess a country’s ability to meet its financial obligations. The highest possible rating (Aaa for Moody’s or AAA for S&P and Fitch) indicates that the borrower is extremely likely to repay its debts on time and in full.

Fewer than a dozen countries hit the trifecta with top ratings across the board, including Australia, Canada, and Germany.

For investors, these ratings help gauge risk. Higher-rated bonds (i.e., investment grade) are considered safer, while lower-rated ones (i.e., junk bonds) typically offer higher yields to compensate for greater uncertainty.

So when a country’s rating drops, it raises concerns and signals that debt dynamics are becoming less favorable. In the case of the US, the downgrade doesn’t mean Treasuries are suddenly risky though. It simply factors in rising deficits, political gridlock, and the sustainability of government debt levels.

A Brief Timeline: The Three Big Downgrades

The US government has held a near-spotless credit record for most of its history. However, over the past 14 years, each of the three major rating agencies has taken the rare step of downgrading America’s credit, citing rising debt burdens and political dysfunction as the driving forces.

S&P Downgrade (August 2011)

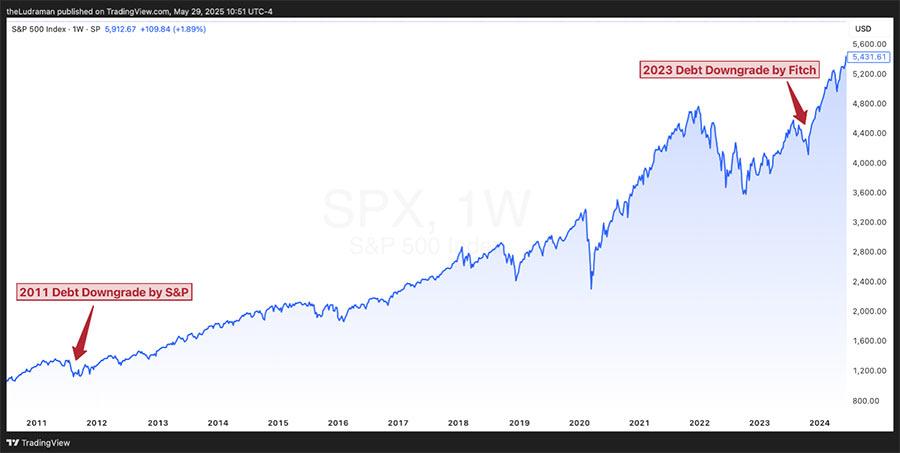

Following a tense standoff over the debt ceiling, S&P downgraded the US credit rating for the first time ever, lowering it from AAA to AA+. The move came just days after a tense debt ceiling standoff in Congress. S&P pointed to concerns about political brinkmanship and the government’s long-term fiscal trajectory.

The decision was met with intense backlash, including public criticism from the White House and Treasury Department as well as a sharp sell-off in equities. Adding to the storm, S&P’s president Deven Sharma announced his resignation shortly afterward. Although the company said his exit had been planned for months, the timing raised eyebrows and added to the drama.

Fitch Downgrade (August 2023)

Twelve years later, Fitch followed in S&P’s footsteps. The agency cited a deteriorating fiscal outlook, rising general government debt as a share of GDP, and “repeated debt limit standoffs and last-minute resolutions.”

As before, the White House and Treasury disagreed with the downgrade. The move sparked short-term market volatility, ironically pushing investors into the very Treasuries that were downgraded.

Moody’s Downgrade (May 2025)

Moody’s eventually joined its peers, centering its decision on unsustainable fiscal trends and a lack of effective long-term debt reduction measures. Different year, same story.

The ratings agency estimates the federal deficit will reach nearly 9% of GDP by 2035 — up from 6.4% in 2024. It also projects the federal debt burden will expand to about 134% of GDP in the same time frame, compared to 98% in 2024. Per Moody’s rationale:

“While we recognize the US’ significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics.”

While all three downgrades are symbolically significant, it’s worth emphasizing that none of them suggest a default is likely. They’re cautionary notes about the trajectory of US debt and governance.

Should Investors Be Worried?

In short: not necessarily.

While a US credit downgrade is a headline-grabbing event, the US remains one of the most creditworthy borrowers in the world.

Treasuries are still the backbone of global finance. The US dollar is still the world’s primary reserve currency. And demand for government bonds has shown resilience, even during past downgrades.

That’s not to say there won’t be volatility. When S&P issued its downgrade in 2011, equity markets tumbled — but Treasuries rallied. Investors still viewed US debt as a safe haven, and that perception hasn’t changed dramatically.

Exhibit 1 (Source: TradeWeb)

The aftermath of Fitch’s downgrade in 2023 was similar: markets quickly regained their footing. To date, Moody’s downgrade has elicited a muted response, but it may trigger some short-term volatility. Regardless, for long-term investors, the practical impact on diversified portfolios is likely to be minimal.

Investor Takeaways

Here’s what investors should keep in mind:

1. Treasuries Are Still Considered Safe

Downgrades are not irrelevant. They call attention to deeper structural issues, particularly around policy concerns. Even so, with a Aa1 rating, US government bonds are still high quality.

2. Short-Term Volatility Is Possible, But Unlikely to Be Severe

Markets may endure some turbulence, especially in fixed income. That said, as history has shown, downgrades don’t typically lead to lasting volatility.

3. Fiscal Discipline Matters

The downgrade serves as a reminder that growing deficits and political dysfunction aren’t without consequence. Over time, they can contribute to inflationary pressures or upward pressure on interest rates.

4. Focus on What You Can Control

Ominous headlines aside, investors should prioritize portfolio diversification and long-term discipline. A single ratings change doesn’t alter the fundamentals of your strategy.

Ultimately, success comes from spreading risk thoughtfully and buying high-quality assets, then letting time in the market compound your returns.