For many, the choice of retirement plan type is made for them by their employer, or as an after-effect of a distant decision to create an account themselves, or perhaps, to roll something over from one firm to another. Because these choices are often littered with dense financial & legal jargon, as well as the fact that plan choices are often not their own, the public is all too often oblivious to the features, benefits and risks of each plan type.

For individual savers looking to understand the strengths and weaknesses of the wide range of retirement savings vehicles, we created this guide. In the United States there are at least 18 different types of retirement plans that fall in four discrete categories: individual retirement accounts, defined benefit plans, employer-sponsored plans, and small business plans. Moreover, business owners and managers make a variety of discretionary choices in implementing their plans (such as eligibility requirements, matching contributions, non-elective contributions, vesting schedules, hardship provisions, investment menu, etc.) that have meaningful impact on plan participants.

Key Attributes of Retirement Plans

Taxes

Retirement plans impact taxes paid by participants based on contribution type and withdrawal timing. Traditional plans like IRAs and 401(k)s use pre-tax contributions, thereby lowering taxable income at the time of contribution, but taxing withdrawals as income later. In contrast, Roth IRA accounts use after-tax money for contributions and create no tax impact when withdrawals are made. With respect to pensions, employers contribute to pension plans on behalf of employees and pension beneficiaries are taxed on the pension benefits as income when paid. 457(b) plans allow early withdrawals without penalties but are still taxed. All plans offer tax-deferred growth potential, with Roths providing tax-free growth, helping savings compound faster. From the participant’s perspective, if tax law were to remain unchanged (or similar) throughout the beneficiary’s life, then determination of what is most advantageous for a retiree depends only on the individual’s expected income tax bracket at the date of withdrawal/payments. Alternatively, if tax law does change – which is imminently possible – then the retiree must contend with both tax bracket changes as well as income level changes upon retirement.

Contribution Limits

Retirement plans have varying contribution limits based on plan type and participant role. Traditional and Roth IRAs have relatively low annual limits ($7,000 in 2025, or $8,000 if age 50+), while employer-sponsored plans like 401(k), 403(b), and 457(b) allow much higher contributions ($23,000 in 2025, or $30,500 with catch-up). SEP IRAs and Solo 401(k)s allow self-employed individuals to contribute both as employee and employer, potentially reaching $69,000 annually. SIMPLE IRAs offer moderate limits ($16,000 in 2025, plus $3,500 catch-up). Defined benefit and cash balance plans have limits based on actuarial calculations, often allowing six-figure contributions for older participants. Each plan’s structure influences saving potential and tax strategy.

Flexibility, Withdrawals, Distributions & Penalties

Retirement plans have differing rules on withdrawals, distributions, and penalties. Most, like Traditional IRAs and 401(k)s, impose a 10% early withdrawal penalty before age 59½, plus income tax due on the amount withdrawn. Roth IRAs allow tax- and penalty-free withdrawals of contributions anytime, and qualified earnings withdrawals after age 59½ if the account is at least five years old. Required Minimum Distributions (RMDs) generally begin at age 73 for Traditional IRAs, 401(k)s, and similar plans, but Roth IRAs (unlike Roth 401(k)s) are exempt during the owner’s lifetime. 457(b) government plans allow penalty-free withdrawals upon separation from service at any age. Inherited IRAs have special rules, often requiring full distribution within 10 years. Some plans, like pensions and cash balance plans, pay out on a fixed schedule, limiting flexibility.

Investment Choices & Participant Control

Investment choices vary widely across retirement plans. IRAs–specifically self-directed IRAs–offer the broadest range, including stocks, bonds, real estate, private equity, and more. Employer-sponsored plans like 401(k)s, 403(b)s, and 457(b)s typically limit participants to a menu of mutual funds or target-date funds selected by the plan sponsor. Pension and cash balance plans are usually managed by the employer, giving participants no investment control. Thrift Savings Plans (TSPs) for federal employees offer a small selection of low-cost index funds. SEP and SIMPLE IRAs function like traditional IRAs, offering broad choices through custodians. Overall, self-directed plans provide the most flexibility, while employer plans prioritize simplicity and oversight.

Vesting & Employer Match

Vesting and employer matching vary by plan. In 401(k), 403(b), SIMPLE IRA, and similar plans, employers may offer matching contributions, often subject to a vesting schedule (e.g., graded over several years or cliff vesting after a set period). SEP IRAs and pensions usually provide immediate full vesting, but only employers contribute. Cash balance plans also use employer-only contributions, with vesting schedules allowed. Solo 401(k)s have no vesting issues since the business owner is both employer and employee. Vesting rules affect how much of the employer’s contributions a participant keeps if they leave the job early.

ERISA, Fiduciary & Asset Protection

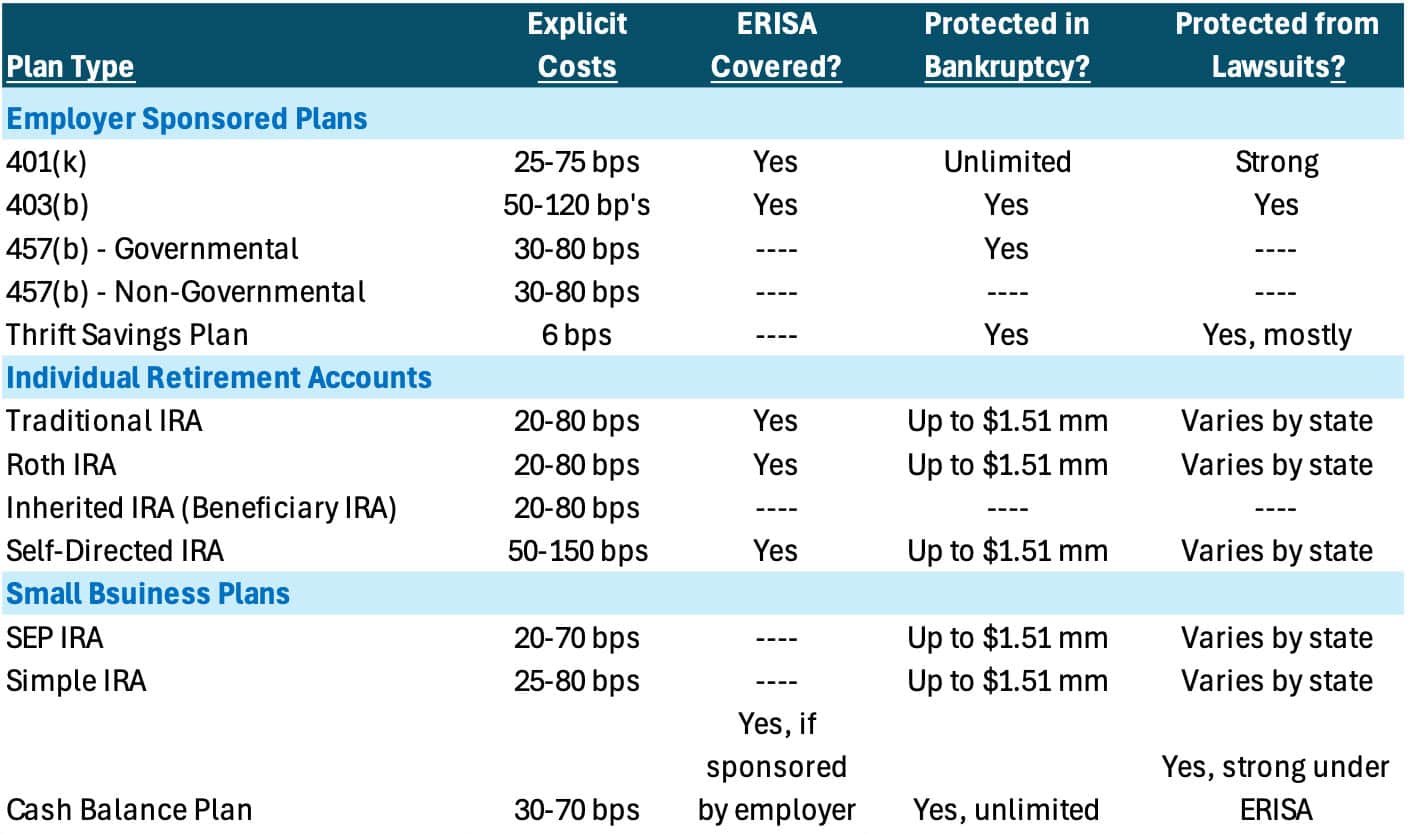

ERISA-covered plans like 401(k)s, 403(b)s, pensions, and cash balance plans offer strong federal protections, shielding assets from creditors and lawsuits in bankruptcy. IRAs, including Traditional, Roth, SEP, and SIMPLE IRAs, are not ERISA-covered but still have substantial bankruptcy protection under federal law (up to ~$1.5 million, inflation-adjusted) and varying state-level lawsuit protections. Self-directed IRAs may be more vulnerable due to non-traditional assets. Governmental 457(b) plans are not ERISA-covered but generally protected by sovereign immunity. Non-governmental 457(b)s lack strong protections and are considered employer assets until paid out. ERISA status significantly impacts legal security of retirement funds.

Portability

Portability varies by plan type. IRAs (Traditional, Roth, SEP, SIMPLE) are highly portable, easily transferred or rolled over between custodians. 401(k), 403(b), and governmental 457(b) plans can typically be rolled over to IRAs or new employer plans upon job change or retirement. Pensions and cash balance plans are less portable, often offering lump-sum payouts or annuities, with limited rollover options. Non-governmental 457(b)s are usually non-transferable and must stay with the original employer. Portability affects how easily participants can consolidate accounts or maintain tax-deferred growth potential when switching jobs.

Administrative Cost & Complexity

Retirement plan costs and complexity vary widely. IRAs (Traditional, Roth, SEP, SIMPLE) are low-cost and simple to administer through financial institutions. In contrast, employer-sponsored plans like 401(k)s, 403(b)s, and pensions involve higher administrative costs, compliance burdens, and fiduciary responsibilities. Defined benefit and cash balance plans require actuarial services and are among the most complex. Solo 401(k)s offer high flexibility but require filings once assets exceed $250,000. Self-directed IRAs can be complex and costly due to due diligence and custodial fees for alternative assets. Generally, greater contribution limits and control come with higher administrative demands.

Side by Side Comparisons

When comparing retirement / deferred compensation plans, these are some of the key dimensions (features) that make one plan more or less attractive to a participant:

As you can see, there is a wide range of features, benefits and risks to plan participants, depending on the type of retirement plan vehicles he or she uses. Not only do these features affect the safety, stability and returns your retirement can generate, but there are also material differences in costs that act as a drag on compounded returns as noted in the following table.

Understanding the constraints and limits of your retirement plan, and making wise choices in light of them, can have a profound impact on a participant’s long-term financial security, tax exposure, investment flexibility, and legal protections. Each plan type offers a unique blend of advantages and trade-offs. For example, employer-sponsored plans like 401(k)s and pensions provide high contribution ceilings and strong ERISA protections but may offer limited investment choices and come with administrative oversight. On the other hand, IRAs–particularly Roth and Traditional IRAs–offer more control and simplicity but have lower contribution limits and fewer creditor protections outside bankruptcy.

Specialized plans like Self-Directed IRAs or Cash Balance Plans cater to those with specific financial goals, higher incomes, or unique asset preferences, yet they demand a greater level of financial literacy and legal compliance. Government and nonprofit employees have access to tailored options such as 403(b), 457(b), and the Thrift Savings Plan, each with its own mix of accessibility, investment structure, and employer involvement.

Ultimately, no single retirement plan is inherently superior. The best choice depends on a participant’s income level, employment situation, investment preferences, and need for legal protection. A well-structured retirement strategy often combines multiple plan types to balance tax treatment, asset growth, and risk mitigation. For most individuals, informed planning is essential to optimizing the long-term benefits of these diverse retirement vehicles.

Related Articles

Comparing SEP IRAs and 401(k)s: Which Retirement Plan Makes the Most Sense for You?

Personal Finance,

April 22, 2025

Retirement Planning for High Earners: The Benefits of Cash Balance Plans

Personal Finance,

July 11, 2024

How Much Money Do You Need To Make Before Contributing to A 401(k)

Personal Finance,

Top Personal Finance FAQs,

September 19, 2024