A Year Defined by Eroding Trust

If 2001 was dominated by shock and uncertainty, 2002 was defined by a profound loss of confidence. Investors entered the year hoping that the worst of the post-technology bubble downturn had passed, but those expectations were repeatedly disappointed. Equity markets suffered through another punishing decline as concerns shifted from economic growth to corporate integrity, accounting transparency, and the credibility of U.S. capital markets themselves.

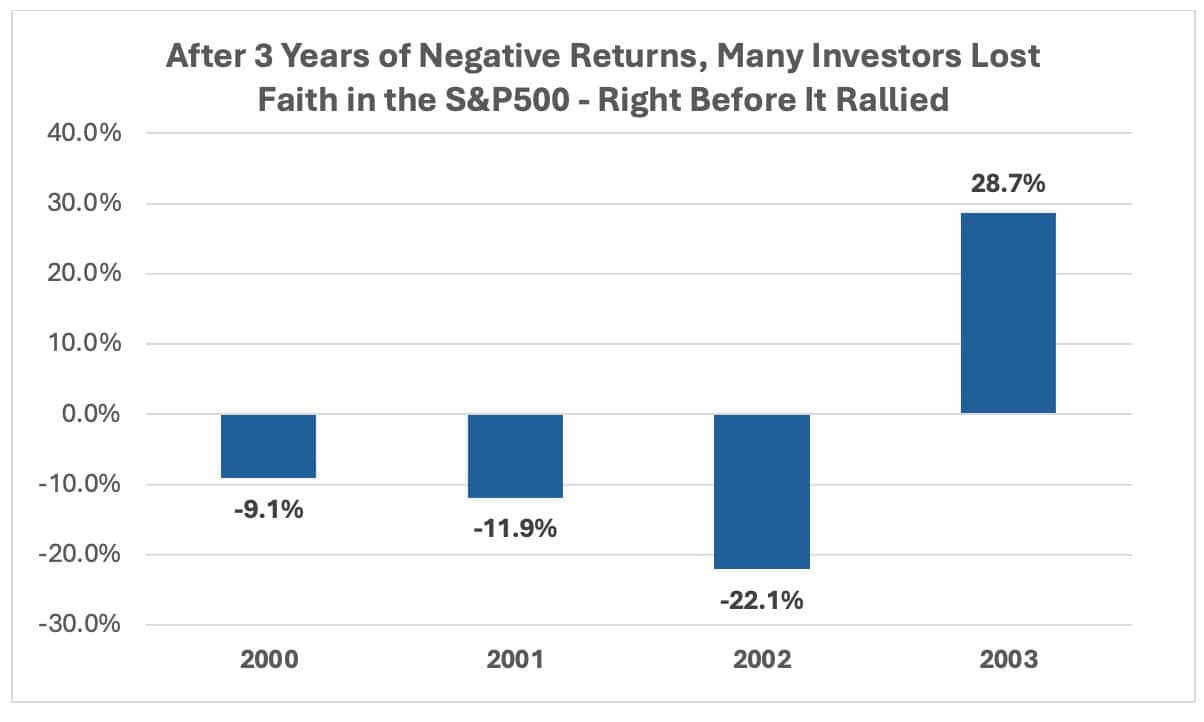

The S&P 500 fell approximately 22% in 2002, marking its third consecutive year of losses and the index’s worst annual performance since 1974. The Nasdaq Composite declined roughly 31%, continuing its collapse from the excesses of the late 1990s, while the Dow Jones Industrial Average fell about 16%. By October, equity markets reached levels not seen since the mid-1990s, completing a brutal unwinding of the prior decade’s optimism.

Corporate Scandals and the Collapse of Confidence

The defining feature of 2002 was a wave of high-profile corporate scandals that fundamentally altered investor psychology. The collapse of Enron, followed by revelations at WorldCom, Tyco, Adelphia, and others, exposed widespread accounting manipulation and weak governance practices. WorldCom’s mid-year bankruptcy, at the time the largest in U.S. history, was particularly damaging, as it revealed billions of dollars in improperly capitalized expenses.

These events created a crisis of trust. Investors no longer questioned just earnings growth; they questioned whether reported earnings could be believed at all. Equity risk premiums rose sharply, valuations compressed, and selling pressure intensified across sectors, particularly in technology, telecommunications, and financials tied to corporate lending.

Policy Response and Regulatory Reform

In response to the crisis, policymakers moved to restore credibility to the financial system. The passage of the Sarbanes-Oxley Act in July 2002 imposed stricter accounting standards, enhanced disclosure requirements, and increased executive accountability. While the legislation was initially viewed as a headwind for corporate profitability due to higher compliance costs, markets ultimately welcomed the effort to rebuild trust.

The Federal Reserve also remained accommodative, maintaining the federal funds rate at 1.75% throughout the year. While monetary policy provided some support, it could not offset the psychological damage caused by repeated governance failures. Investors were not yet willing to embrace risk simply because liquidity was available.

Bear Market Capitulation and the October Low

Market declines accelerated during the summer months, culminating in a sharp selloff in July and September. Volatility spiked, equity mutual fund outflows increased, and sentiment surveys reached extreme pessimism. By October, many investors had abandoned any expectation of a near-term recovery.

Ironically, this capitulation laid the groundwork for the next cycle. The S&P 500 reached its intraday low on October 9, 2002, down nearly 50% from its 2000 peak. Valuations at that point reflected deeply depressed expectations, with many high-quality companies trading at levels last seen years earlier.

Bonds, Credit Markets, and a Flight to Safety

As equities struggled, fixed income markets provided stability. Treasury bonds rallied as investors sought safety, pushing the 10-year Treasury yield below 4%. Investment-grade bonds delivered solid returns, while credit spreads widened amid concerns about corporate defaults.

High-yield bonds experienced periods of stress but avoided systemic collapse, as balance sheets outside the most troubled sectors remained manageable. For diversified investors, bonds played their traditional role as a ballast during equity market stress.

Economic Backdrop and the Consumer

Despite market turmoil, the broader U.S. economy avoided recession in 2002. GDP growth was modest, around 1.7%, supported by consumer spending and a still-strong housing market. Low interest rates encouraged refinancing activity, helping households manage through equity losses and employment uncertainty.

This disconnect between economic data and market performance frustrated investors but underscored how deeply confidence issues dominated asset pricing during the year.

Setting the Stage for Recovery

By the end of 2002, markets remained fragile, but important foundations were in place. Excess valuation had been largely purged, corporate behavior was under increased scrutiny, and policy remained supportive. While few investors felt optimistic at the time, the conditions that emerged in late 2002 would ultimately support the powerful recovery that began the following year.

For long-term investors, 2002 served as a reminder that bear markets often end not with optimism, but with exhaustion—when fear has largely displaced hope, and expectations have fallen far enough to allow recovery to begin.