A Year of Recovery, Reinforced by Policy Support

After the trauma of the global financial crisis, 2010 marked a year of cautious recovery for investors. While memories of 2008 and early 2009 remained fresh, markets spent much of the year rebuilding confidence as economic data slowly improved and policymakers maintained extraordinary levels of support. The investment environment was defined by a gradual healing process rather than rapid expansion, with optimism repeatedly tempered by lingering structural concerns.

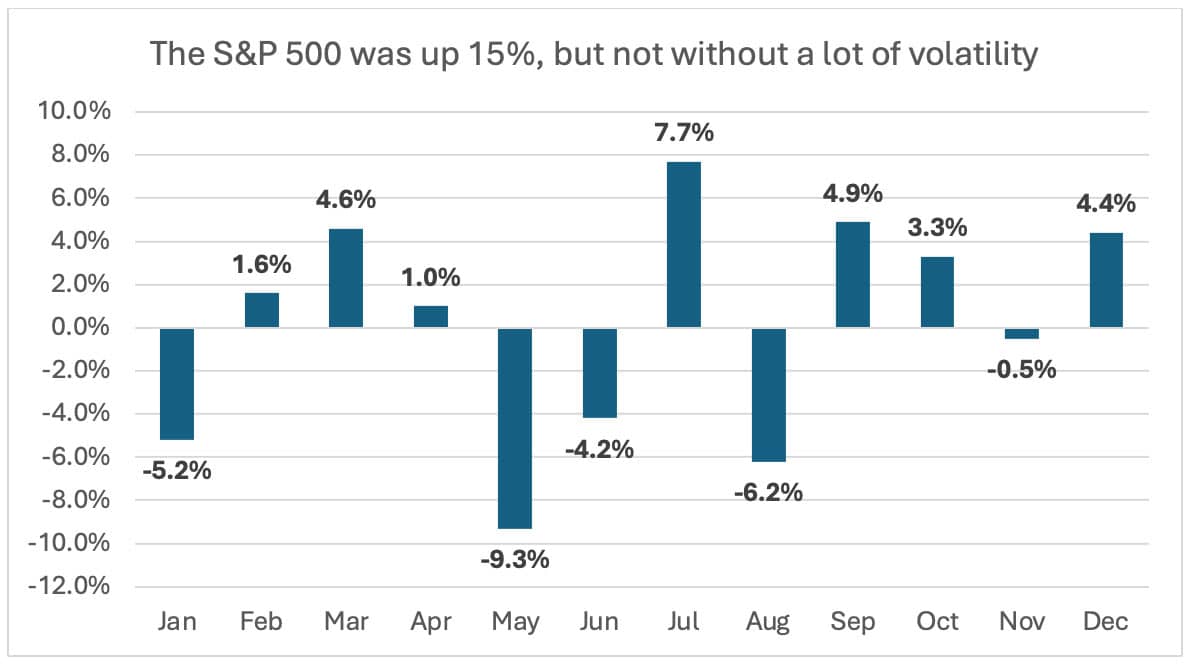

For investors, 2010 was a reminder that recoveries are rarely smooth, but that markets can still deliver meaningful returns amid uncertainty.

Economic Growth Returns, but at an Uneven Pace

The global economy continued to emerge from recession in 2010, led by the United States and supported by strong growth in emerging markets. U.S. GDP expanded at a moderate pace, corporate profits rebounded sharply, and business confidence improved as access to credit slowly normalized.

However, the recovery remained uneven. Housing activity stayed weak, unemployment remained elevated near 9-10% for much of the year, and consumer confidence fluctuated. Investors were forced to reconcile improving corporate fundamentals with a labor market that was slow to heal, reinforcing concerns about the durability of the expansion.

Internationally, emerging markets such as China, Brazil, and India posted robust growth, helping drive demand for commodities and manufactured goods. These trends supported global earnings growth but also introduced new concerns about overheating, inflation pressures, and the sustainability of rapid expansion.

The European Debt Crisis Reemerges

Just as markets were gaining confidence, concerns over sovereign debt in Europe resurfaced. Greece became the focal point in early 2010 as its fiscal problems escalated, raising fears of default and potential contagion across the eurozone. Bond yields for Greece and other peripheral countries rose sharply, reflecting growing investor anxiety.

In response, European authorities and the International Monetary Fund announced bailout packages and new stabilization mechanisms aimed at preventing broader financial disruption. While these measures helped calm markets temporarily, they underscored the fragility of the global recovery and introduced a recurring source of volatility that would persist for years.

For investors, the European debt crisis highlighted how fiscal imbalances and political constraints could threaten financial stability even after a major global recession had officially ended.

Equity Markets Deliver Strong Gains

Despite periodic volatility, equity markets produced solid returns in 2010. The S&P 500 gained approximately 15%, supported by strong earnings growth and historically low interest rates. Corporate profitability rebounded sharply as companies benefited from cost-cutting measures implemented during the recession and improving demand.

Leadership rotated throughout the year. Cyclical sectors such as industrials, technology, and consumer discretionary stocks performed well as investors positioned for economic recovery. Financial stocks stabilized after the turmoil of the prior two years, although regulatory uncertainty and balance sheet concerns continued to weigh on valuations.

International equities also performed well, particularly in emerging markets, though gains were accompanied by increased volatility as investors grappled with policy tightening abroad and currency fluctuations.

Monetary Policy Remains Accommodative

Central banks played a critical role in shaping market outcomes in 2010. The Federal Reserve maintained near-zero short-term interest rates throughout the year, reinforcing its commitment to supporting economic growth. Late in the year, concerns about slowing momentum and low inflation led the Fed to announce a second round of quantitative easing, commonly referred to as “QE2.”

Low interest rates supported higher equity valuations, encouraged borrowing and investment, and reduced the appeal of cash holdings. For investors, central bank policy became an increasingly important driver of asset prices, reinforcing the need to monitor policy developments alongside economic data.

Bonds Offer Stability but Lower Returns

The U.S. Bond market was positive in 2010 (Bloomberg U.S. Aggregate Bond Index +6.5%). Treasury yields fluctuated throughout the year, reflecting alternating periods of optimism and risk aversion. While yields remained historically low, high-quality bonds continued to provide diversification benefits during periods of market stress.

Credit markets improved significantly as default risks declined and investor confidence returned. Corporate bonds, particularly investment-grade and high-yield issues, benefited as balance sheets strengthened and access to capital improved.

For diversified portfolios, bonds played a stabilizing role, though investors increasingly recognized that future returns would likely be lower given starting yield levels.

A Year of Rebuilding Confidence

By year-end, markets had made substantial progress in recovering from the financial crisis, but uncertainty remained a defining feature of the investment landscape. Policymakers were still heavily involved, structural challenges persisted, and confidence was rebuilt gradually rather than decisively.

For long-term investors, 2010 reinforced the value of maintaining discipline during periods of recovery. Markets rewarded patience, diversification, and a willingness to look beyond short-term headlines as the global economy continued its slow, uneven return to stability.