A Year Defined by Policy Reversal, Trade Tensions, and a Powerful Market Recovery

Following one of the most volatile and unsettling market environments in years, 2019 marked a dramatic reversal for investors. After the sharp equity market selloff in late 2018, concerns entering the year centered on slowing global growth, tightening financial conditions, and escalating trade tensions between the United States and China. Instead of deterioration, markets were met with a decisive shift in monetary policy, easing financial conditions, and a resurgence in risk appetite that fueled one of the strongest equity market years of the decade.

By year-end, investors were reminded once again of the market’s sensitivity to policy moves—and the speed with which sentiment can change.

Federal Reserve Pivot Ignites Risk Assets

The single most important market development of 2019 was the Federal Reserve’s abrupt shift away from monetary tightening. After raising interest rates four times in 2018, the Fed entered 2019 signaling patience and, eventually, accommodation as global growth softened and financial markets showed signs of strain.

By July, the Fed delivered its first rate cut since the financial crisis, ultimately lowering the federal funds rate three times during the year by a total of 75 basis points. This pivot had a profound impact on markets. Equity valuations expanded, borrowing costs declined, and financial conditions loosened meaningfully. The 10-year Treasury yield fell from approximately 2.7% at the start of the year to near 1.9% by August, reflecting both rate cuts and heightened demand for safety earlier in the year.

This policy reversal restored investor confidence and became the foundation for the year’s strong asset price performance.

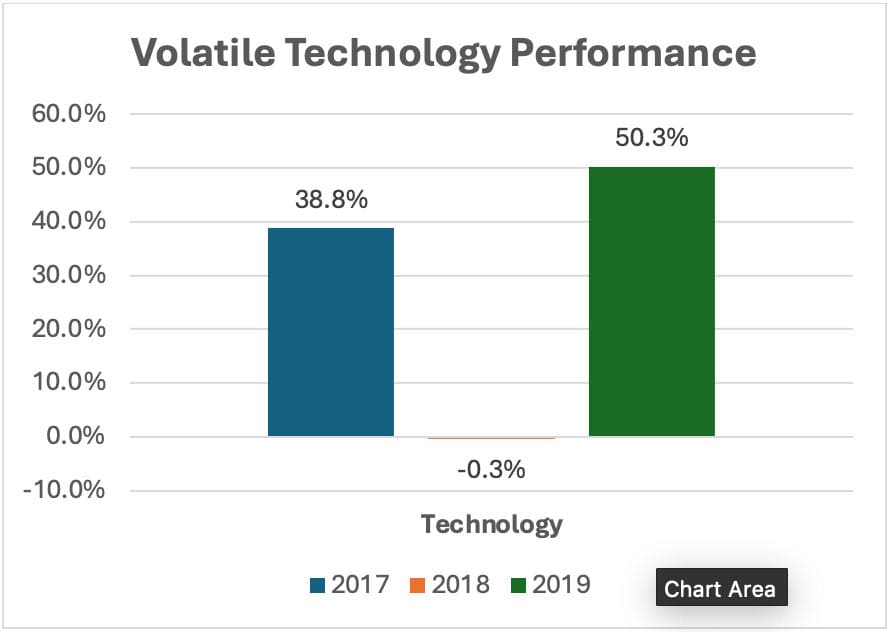

Equity Markets Stage a Historic Rebound

U.S. equity markets delivered exceptional returns in 2019, rebounding sharply from the prior year’s losses. The S&P 500 finished the year up approximately 31%, its best annual return since 2013 and one of the strongest performances of the post-crisis era. The Nasdaq Composite rose roughly 36%, driven by strength in technology and growth-oriented companies, while the Dow Jones Industrial Average gained about 25%.

Importantly, the rally was driven largely by valuation expansion rather than earnings growth. Corporate profits were relatively flat, reflecting margin pressures, slower global demand, and uncertainty tied to trade policy. However, lower interest rates benefit growth stocks and long-duration assets.

Large-cap growth significantly outperformed value stocks, extending a trend that had already been in place for much of the decade. At the same time, smaller companies lagged their large-cap counterparts, as investors favored balance sheet strength and global scale amid ongoing uncertainty.

Trade War Volatility Dominates Headlines

Throughout 2019, trade tensions between the U.S. and China remained a persistent source of market volatility. The year was afflicted by alternating periods of optimism and escalation, as tariff announcements and negotiation headlines repeatedly moved markets.

Tariffs were raised on hundreds of billions of dollars of goods, directly affecting global supply chains and corporate planning. Manufacturing activity weakened globally, with several regions flirting with recessionary conditions. U.S. business investment slowed notably, reflecting hesitation around capital spending amid policy uncertainty.

Despite these challenges, markets increasingly treated trade-related volatility as periodic rather than systemic. By year-end, progress toward a “Phase One” trade agreement helped stabilize sentiment, reinforcing the market’s belief that the worst economic outcomes could be avoided.

Bonds Deliver Strong Returns Amid Falling Yields

Fixed income markets played a critical role in 2019, delivering returns that surprised many investors. As interest rates declined, bond prices rose meaningfully. The Bloomberg U.S. Aggregate Bond Index gained approximately 8.7% for the year, one of its strongest annual performances in decades.

Treasury securities provided balance during periods of equity volatility, while investment-grade credit benefited from declining yields and stable corporate balance sheets. Even with low absolute yields, bonds reaffirmed their role as a stabilizing force within diversified portfolios.

The yield curve, which briefly inverted during the year, raised recession concerns but ultimately normalized as growth stabilized and policy eased.

Looking Back at 2019

By the end of 2019, investors were reminded that markets often recover well before economic clarity fully emerges. The year demonstrated the powerful influence of central bank policy, the resilience of risk assets, and the importance of maintaining discipline during periods of volatility. What began with lingering fear and skepticism concluded with renewed confidence, setting the stage for the unexpected challenges that lay ahead.