Following the extraordinary volatility of 2020, investors entered 2021 with cautious optimism. Vaccines were being distributed, economies were reopening, and unprecedented monetary and fiscal support remained firmly in place. While uncertainty persisted, the dominant question shifted from crisis management to recovery: how quickly would growth return, and what would it mean for markets?

By year-end, 2021 proved to be a year of strong returns, declining volatility, and growing confidence.

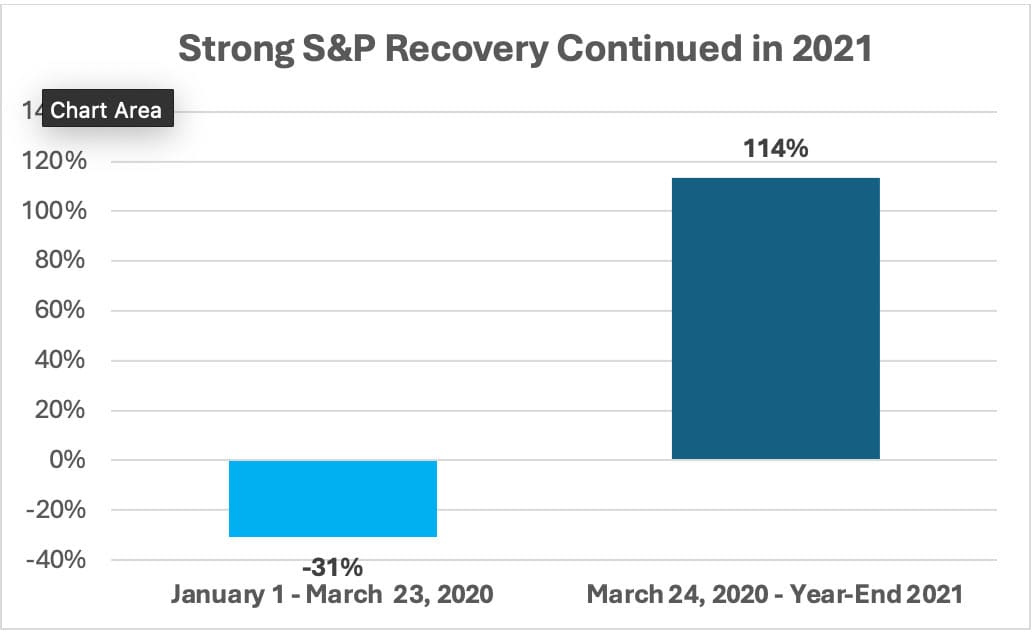

A Powerful Economic Reopening

The defining theme of 2021 was the global economic reopening. As vaccination rates increased and restrictions eased, consumer activity rebounded sharply. Pent-up demand, elevated household savings, and ongoing fiscal support combined to fuel strong economic growth, particularly in the United States.

Corporate earnings surged. S&P 500 earnings grew by more than 45% year over year, far exceeding expectations at the start of the year. This earnings recovery provided support for equity markets, helping justify higher valuations following the sharp rally off the 2020 lows.

Equity markets responded positively. The S&P 500 gained approximately 29% in 2021, marking one of the strongest annual returns of the past decade. Importantly, the advance was far less volatile than the prior year, reinforcing investor confidence and encouraging greater risk-taking across asset classes.

Continued Policy Support and Ultra-Low Interest Rates

Despite the improving economic backdrop, monetary policy remained highly accommodative throughout most of 2021. The Federal Reserve kept the federal funds rate near zero and maintained ample liquidity across financial markets.

As the economy grew, interest rates, while still historically low, began to climb slightly (the 10-year Treasury yield rose from 0.9% to 1.5%). This upward movement in yields pushed bond prices down, resulting in negative bond returns for the year.

Fiscal policy also remained supportive. Additional stimulus measures, including infrastructure spending initiatives, reinforced expectations for sustained economic expansion. For investors, the policy backdrop in 2021 was notably different from prior recoveries—growth was strong, yet financial conditions remained exceptionally easy.

Equity Leadership Broadens, Then Narrows Again

Early in the year, market leadership broadened meaningfully. Cyclical and value-oriented sectors such as financials, industrials, and energy outperformed as investors positioned for reopening and reflation. Small-cap stocks also performed well early on, benefiting from domestic economic strength.

As the year progressed, however, leadership shifted back toward large-cap growth and technology-oriented companies. Slowing global growth, concerns around new COVID variants, and falling long-term interest rates in the second half of the year renewed investor preference for high-quality, cash-generating businesses.

Technology and communication services once again played an outsized role in market returns. Companies such as Apple, Microsoft, Alphabet, and NVIDIA benefited from durable earnings growth and strong balance sheets, reinforcing their status as core holdings in many portfolios. By year-end, market concentration remained elevated, though less extreme than during the depths of the pandemic.

Inflation Emerges as a Market Concern

While markets were largely constructive throughout the year, inflation quietly emerged as a growing concern. Supply chain disruptions, labor shortages, and strong consumer demand led to rising prices across goods and services. By the end of 2021, U.S. inflation had climbed above 7% year over year—the highest level in decades.

Initially, both policymakers and investors viewed inflationary pressures as transitory. Markets remained relatively calm, and long-term interest rates stayed contained. However, as inflation persisted into the second half of the year, expectations around future monetary policy began to shift.

Bond markets reflected this growing uncertainty. While returns were modestly negative for core fixed income, volatility remained relatively subdued. Still, the groundwork was being laid for a more challenging environment for bonds should inflation remain elevated.

Perspective at Year-End

From an investment standpoint, 2021 rewarded patience and long-term discipline. Strong equity returns, robust earnings growth, and supportive policy combined to deliver favorable outcomes for diversified portfolios. At the same time, the year highlighted how quickly market leadership can rotate and how new risks can emerge even during periods of economic strength.

The extraordinary policy support that defined the post-pandemic recovery remained in place, but signs of strain—particularly around inflation—were becoming harder to ignore. While markets ended the year on solid footing, the investment landscape was beginning to change in ways that would become far more apparent in the years ahead.