After two years defined by extraordinary policy support and strong market returns, 2022 marked a sharp turning point for investors. Entering the year, inflation pressures that had emerged in 2021 were proving far more stubborn than initially expected. This caused a rapid shift in monetary policy, a repricing of financial assets, and one of the most difficult environments for diversified portfolios in decades.

Inflation Becomes the Dominant Market Force

The defining theme of 2022 was inflation. Price pressures that initially appeared temporary became increasingly entrenched as supply chain disruptions, tight labor markets, and elevated energy prices persisted. U.S. inflation peaked above 9% during the summer, reaching its highest level in more than 40 years.

For investors, inflation fundamentally altered the investment landscape. Rising input costs compressed margins, consumer purchasing power came under pressure, and expectations for interest rates shifted dramatically. Markets that had been supported for years by low inflation and easy financial conditions were forced to adjust to a very different reality.

Inflation was no longer a background risk—it became the central issue influencing policy decisions, asset valuations, and investor sentiment throughout the year.

The Federal Reserve’s Most Aggressive Tightening Cycle in Decades

In response to persistent inflation, the Federal Reserve moved swiftly and decisively. Over the course of 2022, the Fed raised the federal funds rate from near zero to over 4%, implementing one of the fastest tightening cycles in modern history. Quantitative easing gave way to quantitative tightening as the Fed began reducing the size of its balance sheet.

This sudden shift had significant implications for markets. Higher interest rates increased placed downward pressure on equity valuations—particularly in growth-oriented sectors. At the same time, rising yields led to significant losses in bond valuations.

The 10-year Treasury yield rose from roughly 1.5% at the start of the year to around 3.9% by year-end. Core bond indexes experienced one of their worst annual returns on record, challenging the traditional role of fixed income as a stabilizing force during periods of equity market stress.

A Rare Year of Losses Across Stocks and Bonds

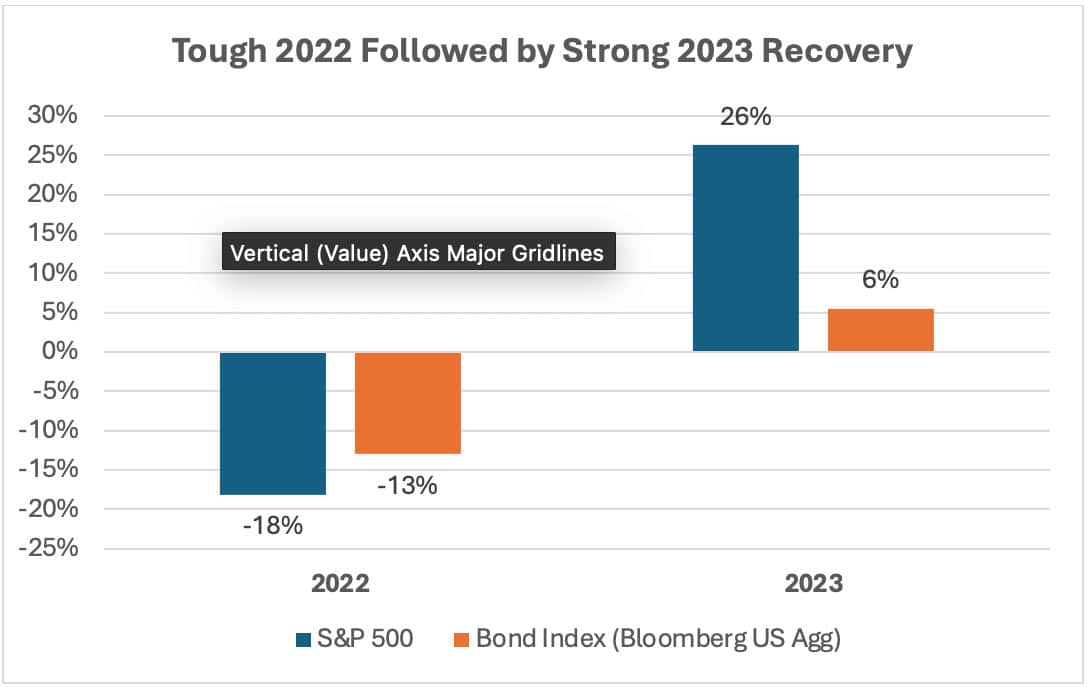

As policy tightened and valuations reset, both equity and fixed income markets struggled. The S&P 500 declined approximately 18% for the year, while technology-heavy indices fell even more sharply as higher rates weighed on growth assets. International equities also posted negative returns, pressured by a strong U.S. dollar and slower global growth.

What made 2022 so difficult for investors was the lack of traditional diversification benefits. Bonds, which historically provided balance during equity drawdowns, declined alongside stocks. As a result, balanced portfolios experienced losses that were unfamiliar to many investors.

Within equities, leadership shifted meaningfully. Energy stocks were a notable exception, posting strong gains as oil and gas prices surged following Russia’s invasion of Ukraine. In contrast, prior market leaders—particularly high-growth technology and speculative assets—experienced significant drawdowns as liquidity conditions tightened.

Geopolitical Tensions and Global Uncertainty

Geopolitical risk also played a prominent role in shaping market outcomes. Russia’s invasion of Ukraine in February added further pressure to global energy markets and exacerbated inflation concerns. Europe faced heightened economic uncertainty, while China’s continued COVID-related restrictions weighed on global growth.

Currency markets reflected these stresses. The U.S. dollar strengthened significantly, reaching multi-decade highs against several major currencies. While supportive for U.S. consumers, dollar strength created headwinds for international investments and multinational earnings.

Perspective at Year-End

From an investment perspective, 2022 was a difficult but important year. It marked the end of an era defined by ultra-low interest rates and abundant liquidity, and the beginning of a new environment in which inflation and policy restraint returned to the forefront.

While returns were disappointing, higher yields improved the long-term outlook for fixed income, and lower equity valuations laid the groundwork for future returns. As a lesson to investors, 2022 reinforced the value of diversification, risk management, and maintaining a long-term perspective during challenging periods.