2020: A Year That Exposed Investor Behavior

Every market cycle tests investors, but 2020 put investor discipline to the test in a way few had experienced since the 1987 crash. It was fast and severe, but it also presented incredible opportunity.

The speed and severity of the COVID-19 market decline created one of the most emotionally challenging environments investors have faced in decades. In just over a month, markets fell more than 30%, volatility reached levels higher than the Global Financial Crisis, and headlines shifted daily from economic shutdowns to rising infection and death counts. The future felt bleak.

Yet by year-end, markets had not only recovered but finished solidly positive. The disconnect between fear and outcome made 2020 one of the clearest demonstrations in history that investor behavior matters more than market forecasts.

The portfolios did not change.

The behavior did.

What follows is a simple illustration of how five investors—facing the same market, the same information, and starting with the same resources—ended the year in dramatically different places.

Five Identical Portfolios. Five Very Different Outcomes.

Consider the results experienced by the following five investors, each of whom entered 2020 with:

- $1,000,000 invested

- $120,000 in cash on the sidelines

The only difference between them was how they behaved during the fear.

*Disclaimer: Source FactSet. Study uses S&P 500 daily returns. The low was calculated as of March 23, 2020. Recovery was calculated as of August 18, 2020.

Investor A: Sold and Never Returned

Investor A panicked at the height of the crisis and sold everything.

- At the time of sale:

Portfolio value: $686,771.90

Cash: $120,000

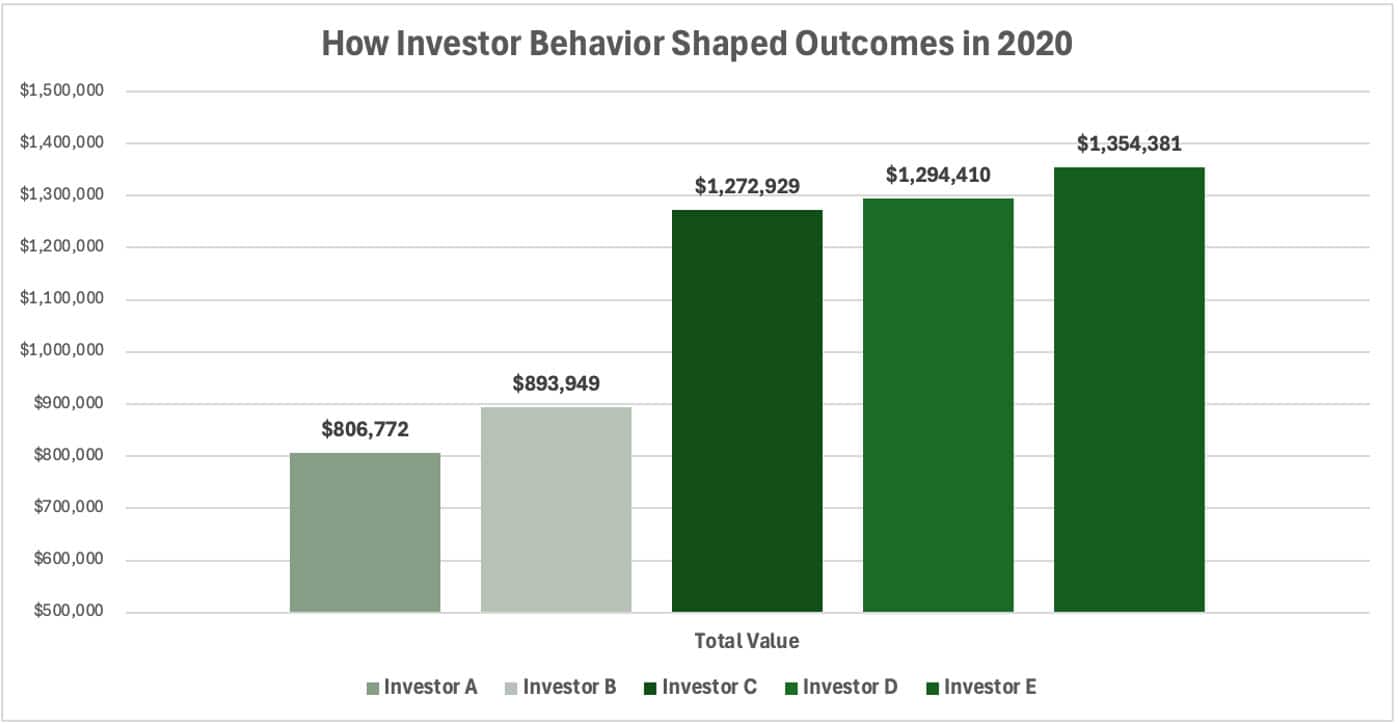

Total: $806,771.90

Concerned that markets would collapse again as COVID cases rose, Investor A never re-entered.

- End of 2020:

Total value: $806,771.90

This was the worst possible outcome—turning a temporary decline into a permanent loss.

Investor B: Sold, Then Re-Entered Late

Investor B also panicked and sold at the lows but eventually re-entered once markets had already recovered and their fears subsided.

- At the March low:

Portfolio value: $686,772

Cash: $120,000 - End of 2020:

Total value: $893,949.39

Selling, even if followed by re-entry, came at a steep cost.

Investor C: Stayed Invested, Did Nothing

Investor C never sold and avoided panic—but also never invested excess cash.

- At the March low:

Portfolio value: $686,772

Cash remaining: $120,000 - End of 2020:

Portfolio value: $1,152,929.07

Cash remaining: $120,000

Total value: $1,272,929.07

Doing nothing worked reasonably well—but it left opportunity on the table.

Investor D: Disciplined and Consistent

Investor D continued adding $10,000 per month throughout the year, including during the depths of the COVID panic.

- At the March low:

Portfolio value: $701,282

Cash remaining: $100,000 - End of 2020:

Portfolio value: $1,294,410.45

Cash remaining: $0

Investor D ignored headlines and focused on accumulating shares when prices were lower. This discipline translated directly into long-term value.

Investor E: Leaned Into the Fear

Investor E stayed invested and deployed all excess cash at the height of market panic.

- At the March low:

Portfolio value: $806,772

Cash remaining: $0 - End of 2020:

Portfolio value: $1,354,380.94

Investor E achieved the best outcome, not by predicting the recovery, but by acting decisively when fear was highest.

Ranking the Outcomes (Worst to Best)

- Stayed out of the market entirely (Investor A)

- Sold and re-entered late (Investor B)

- Did nothing (Investor C)

- Stayed invested and added gradually (Investor D)

- Stayed invested and added aggressively during fear (Investor E)

The pattern is unmistakable. The more fear dictated behavior, the worse the outcome. Of course, events surrounding the pandemic of 2020 could have unfolded somewhat differently such that adding aggressively might have harmed the results for Investors D & E in 2020. But the fullness of history demonstrates unequivocally that discipline is eventually rewarded, so the lessons would have been the same.

Why Behavior Overwhelms Forecasts

What made 2020 so difficult wasn’t just the drawdown—it was the narrative. Markets were falling while uncertainty was rising. The instinct to “wait until things feel better” was completely understandable.

But markets do not recover when certainty returns. They recover when fear peaks.

The investors who fared best were not those with better information. They were the ones who understood that down markets are not interruptions to compounding—they are opportunities to magnify it.

Selling removes capital from recovery. Waiting delays it. Adding accelerates it.

This is why the greatest damage investors do to themselves rarely comes from owning the wrong portfolio. It comes from reacting emotionally at exactly the wrong time.

The Quiet Lesson of 2020

2020 did not reward courage.

It rewarded discipline.

It rewarded investors who recognized that volatility is not risk—it is the price of long-term returns. And that fear, while human, is not a signal.

The market offered the same opportunity to everyone. Nevertheless, different investors earned dramatically different results. And the only factor that determined the differences was investor behavior.

You don’t need to predict the next crisis.

You need to decide—in advance—how you will behave when it arrives.