A Market Entering the Year at Extremes

The year 2000 began with financial markets at a point of extraordinary optimism. The long bull market of the 1990s, fueled by falling interest rates, rapid productivity gains, and enthusiasm surrounding the internet and technology, had pushed equity valuations to historic extremes. Nowhere was this more evident than in technology and growth stocks, where expectations for future earnings far outpaced underlying fundamentals.

In March, the Nasdaq Composite reached its all-time high, capping a multi-year surge driven by speculative capital and retail participation. At the same time, traditional valuation measures such as price-to-earnings ratios were largely dismissed, as investors focused instead on growth narratives, market share, and perceived first-mover advantages.

The Bubble Begins to Deflate

The turning point came in the spring, as investors began to question whether technology companies could deliver on aggressive growth assumptions. A combination of earnings disappointments, tightening financial conditions, and simple exhaustion caused sentiment to shift. Selling pressure intensified quickly, particularly in unprofitable technology and internet stocks.

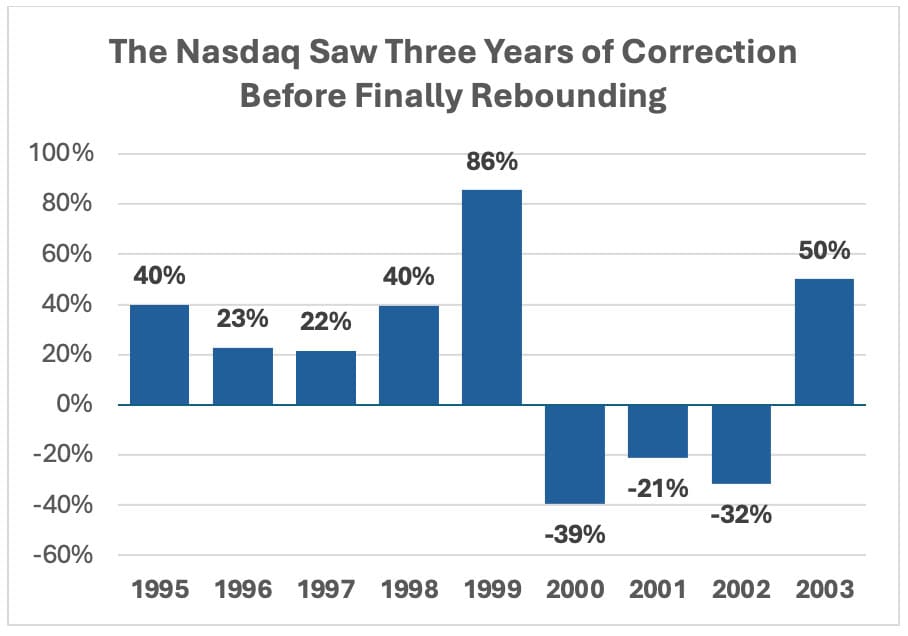

For the full year, the Nasdaq Composite fell approximately 39%, marking one of its worst annual declines on record. The S&P 500 declined roughly 10%, while the Dow Jones Industrial Average finished the year down about 6%. Importantly, the damage was not evenly distributed: technology and telecom stocks collapsed, while many value-oriented and defensive sectors held up comparatively well.

Federal Reserve Policy and the Cost of Capital

Monetary policy played an important role in the market’s reversal. Concerned about overheating conditions and inflationary pressures, the Federal Reserve raised interest rates several times during 1999 and early 2000, pushing the federal funds rate to 6.5% by May. Higher rates increased the cost of capital and reduced the appeal of speculative investments whose valuations depended heavily on distant future profits.

As rates rose, investors became less willing to overlook weak balance sheets and negative cash flows. Companies that had relied on frequent capital raises found access to funding tightening rapidly, accelerating the downturn in speculative areas of the market.

Earnings Reality Sets In

As the year progressed, it became clear that many technology companies would struggle to meet expectations. Revenue growth slowed, margins came under pressure, and competition intensified. Several high-profile companies issued earnings warnings, reinforcing concerns that prior projections had been overly optimistic.

This shift marked an important psychological change. Throughout much of the 1990s, disappointing earnings were often forgiven, with investors quick to buy dips. In 2000, that dynamic reversed, and earnings shortfalls were met with sharp and lasting price declines.

Sector Divergence and Investor Rotation

While technology stocks dominated headlines, other parts of the market told a more nuanced story. Energy stocks benefited from rising oil prices, with crude oil climbing above $30 per barrel amid strong global demand. Financials and consumer staples demonstrated relative resilience, supported by steady cash flows and more reasonable valuations.

This divergence highlighted the growing importance of fundamentals. Investors increasingly favored companies with tangible earnings, dividends, and strong balance sheets, foreshadowing leadership trends that would persist in the years ahead.

Bonds and the Search for Stability

Fixed income markets offered mixed results during the year. Rising interest rates early in 2000 weighed on bond prices, but as equity volatility increased and growth concerns emerged later in the year, Treasuries found support. By year-end, the 10-year Treasury yield had retreated from its highs, reflecting a shift toward safety and expectations of slowing economic momentum.

For diversified investors, bonds provided a measure of stability amid equity market stress, reinforcing their role during periods of market transition.

Psychology at the Turning Point

Perhaps the most significant development of 2000 was the shift in investor psychology. Confidence that equities would reliably deliver strong returns gave way to uncertainty and caution. The idea that markets could experience extended declines, particularly after years of excess, re-entered investor consciousness.

While many still believed the downturn would be short-lived, the year marked the beginning of a broader reassessment of risk, valuation, and diversification.

Laying the Groundwork for the Next Phase

By the end of 2000, markets had clearly transitioned from exuberance to retrenchment. Excesses built over the prior decade were beginning to unwind, and leadership was shifting away from speculation toward quality and durability. Though few investors recognized it at the time, the events of 2000 set the stage for the challenging years that followed—and underscored the importance of discipline, valuation awareness, and long-term perspective in navigating market cycles.