A Fragile Start to the Year

Entering 2001, markets were already under pressure following the collapse of the technology bubble in 2000. Valuations remained elevated in many growth-oriented sectors, corporate earnings expectations were still being revised lower, and business investment was slowing. Equity markets weakened through the first quarter as investors gradually recognized that the economic slowdown was more pronounced than initially believed. Analysts continued to cut earnings forecasts well into the spring, contributing to persistent volatility.

The S&P 500 declined approximately -12% for the year, while the Nasdaq Composite fell roughly -21%, extending its sharp reversal from the late 1990s. The Dow Jones Industrial Average was down about -7%, reflecting relative resilience in more defensive and dividend-oriented stocks. Market leadership narrowed as investors gravitated toward perceived safety rather than growth, with capital flowing into larger, established companies.

The Economy Slips into Recession

The U.S. economy officially entered recession in March 2001, driven by falling capital expenditures, declining corporate profits, and excess capacity built during the prior expansion. Technology spending retrenched sharply as companies pulled back on hardware, software, and telecommunications investment. Layoffs increased, particularly in technology and manufacturing, weakening business and consumer confidence throughout the summer.

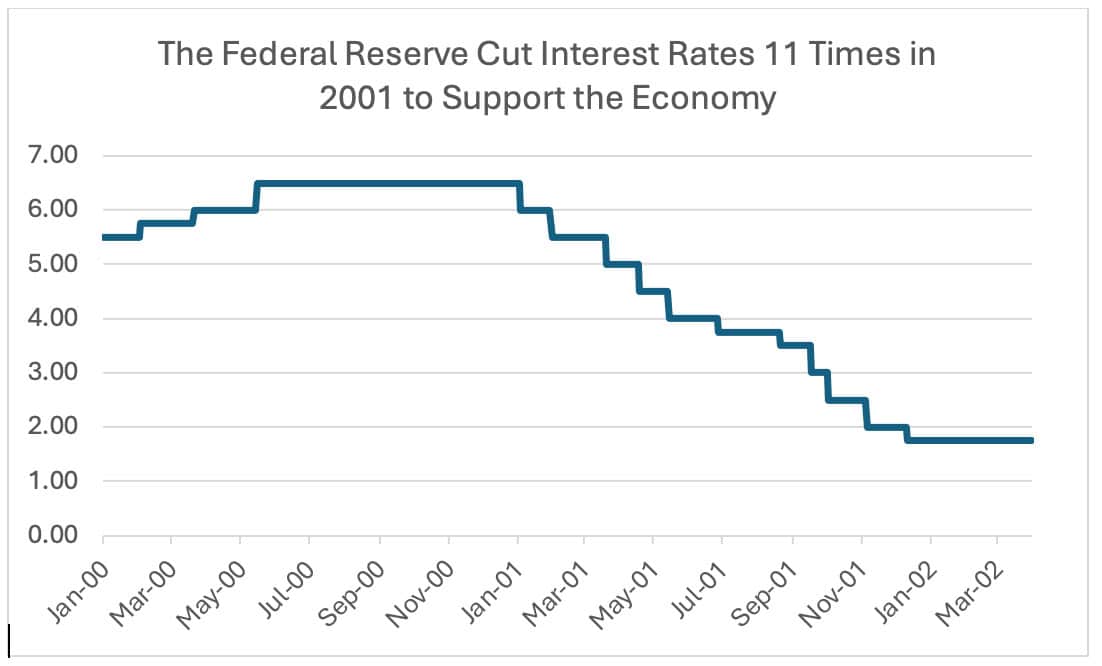

Despite the downturn, inflation remained contained, giving policymakers room to respond. The Federal Reserve began an aggressive easing campaign, cutting the federal funds rate 11 times during the year, from 6.5% to 1.75% by December. These moves were intended to stabilize financial conditions and prevent a deeper contraction, even as economic data continued to deteriorate.

September 11 and the Shock to the System

The defining moment of 2001 came on September 11, when terrorist attacks on New York and Washington fundamentally altered the economic and psychological landscape. U.S. equity markets were closed for nearly a week, the longest shutdown since the 1930s. When trading resumed, stocks fell sharply as investors struggled to assess the economic impact and broader implications for global security and trade.

Airlines, travel-related companies, and insurers experienced immediate and severe losses. Consumer confidence declined abruptly, and business activity slowed further as uncertainty surged. However, the market reaction, while intense, was relatively short-lived compared to the shock itself, reflecting the already depressed state of valuations and sentiment.

Policy Response and Market Stabilization

In the aftermath of the attacks, policymakers acted swiftly. The Federal Reserve provided liquidity to the financial system, reassured markets of its support, and continued its easing cycle. Fiscal policy also became more accommodative, with increased government spending and the groundwork laid for future tax relief measures aimed at supporting demand.

These actions helped stabilize markets in the fourth quarter. While equity indices did not recover meaningfully by year-end, selling pressure eased, volatility declined, and credit conditions gradually improved as confidence slowly returned.

Corporate Earnings and Sector Divergence

Corporate earnings fell sharply in 2001, particularly in technology, telecommunications, and industrial sectors. Excess capacity, pricing pressure, and falling demand weighed heavily on margins. In contrast, more defensive sectors such as consumer staples, utilities, and healthcare held up relatively well, reflecting investors’ preference for stability and predictable cash flows during uncertain times.

The technology sector, once the engine of market growth, continued to unwind excesses built during the bubble years. Many high-profile companies saw revenues stall and profitability evaporate, reinforcing the need for a fundamental reset across the sector.

Bonds, Housing, and the Search for Safety

As equities struggled, bond markets delivered strong returns. Treasury yields fell significantly as investors sought safety and as the Fed cut rates aggressively. The 10-year Treasury yield declined to approximately 5% by year-end, supporting positive returns for intermediate- and long-duration bonds.

Lower interest rates also supported the housing market. Mortgage refinancing activity increased, providing households with cash flow relief and helping to cushion the broader economic slowdown, even as equity wealth declined.

A Year That Reshaped Investor Behavior

By the end of 2001, markets had endured a rare combination of economic recession, financial market adjustment, and geopolitical shock. Investor psychology shifted decisively away from speculation toward capital preservation. While conditions remained fragile, the groundwork was being laid for eventual recovery through accommodative policy, lower valuations, and gradual economic healing.

For investors, 2001 reinforced the importance of diversification, patience, and long-term perspective during periods of profound uncertainty—lessons that would resonate well beyond the year itself.