From Bear Market to Turning Point

After three difficult years marked by the bursting of the technology bubble, corporate scandals, and recession, 2003 became the year markets finally turned the corner. Investor sentiment entering the year was deeply pessimistic, shaped by lingering fears over earnings quality, geopolitical uncertainty, and the aftermath of the 2001 downturn. Equity markets initially wobbled in the first quarter, but by March a durable rally began that would define the rest of the year. Trading volumes increased steadily as institutional investors cautiously re-entered equity markets.

The S&P 500 finished 2003 up approximately 26%, its strongest annual return since 1997. The Nasdaq Composite surged roughly 50%, reflecting a powerful rebound in beaten-down technology and growth stocks, while the Dow Jones Industrial Average gained about 25%. Importantly, the rally was broad-based and persistent, signaling a genuine shift from bear-market recovery to early-cycle expansion rather than a short-lived technical bounce.

The Iraq War and the Removal of Uncertainty

One of the most important catalysts for the market turnaround was the resolution of geopolitical uncertainty surrounding the Iraq War. In the months leading up to the March invasion, markets struggled to price the economic and political consequences of military conflict. Once the invasion began and progressed more quickly than many feared, uncertainty declined sharply.

Historically, markets tend to respond positively when major unknowns are resolved, even if the events themselves are disruptive. In this case, equities began their rally almost precisely as the conflict unfolded, reflecting relief rather than optimism. Energy prices, which had risen in anticipation of supply disruptions, stabilized, easing inflation concerns and supporting consumer confidence later in the year.

Monetary Policy and the Search for Growth

The Federal Reserve played a critical role in shaping market outcomes in 2003. Concerned about sluggish growth and the possibility of deflation, the Fed maintained an exceptionally accommodative stance. In June, the federal funds rate was cut to 1.0%, the lowest level in decades.

Low interest rates encouraged borrowing, supported housing activity, and pushed investors out along the risk spectrum in search of higher returns. Bond yields fell early in the year but rose later as economic growth improved, leading to modest losses for long-duration Treasuries. However, credit markets performed well, as improving economic conditions reduced default risk and tightened credit spreads meaningfully by year-end.

Corporate Earnings and the Rebuilding of Trust

Another key driver of the 2003 rally was a meaningful recovery in corporate earnings. After several years of earnings declines and restatements, profits rebounded sharply. S&P 500 earnings grew by more than 20% during the year, aided by cost cutting, productivity gains, and stabilizing revenues.

Just as important as the numbers themselves was the gradual restoration of trust in corporate reporting. The fallout from scandals such as Enron and WorldCom had severely damaged investor confidence. By 2003, stronger governance standards and improving transparency helped investors feel more comfortable re-engaging with equities, particularly in previously shunned sectors.

Leadership from Small-Cap and Growth Stocks

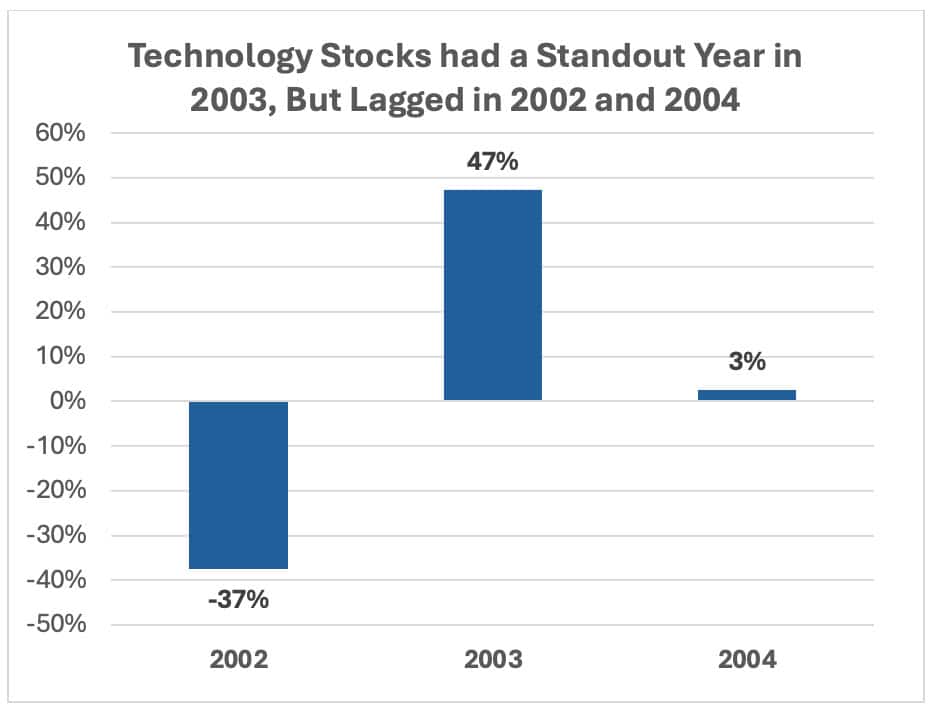

Market leadership in 2003 reflected the early stages of an economic cycle. Small-cap stocks significantly outperformed large caps, with the Russell 2000 gaining roughly 47%, as investors sought companies most leveraged to domestic economic improvement. Growth stocks also outpaced value stocks, reversing the leadership trends of the prior bear market years.

Technology stocks led the rally, benefiting from lean cost structures and operating leverage as demand stabilized. Semiconductor stocks, in particular, rebounded sharply as inventories normalized and capital spending slowly returned across the technology supply chain.

Housing, the Consumer, and Economic Momentum

Low interest rates fueled a strong housing market, which became a key pillar of economic growth. Rising home prices supported household balance sheets and encouraged consumer spending through refinancing and home equity extraction. The U.S. economy grew approximately 2.8% in 2003, with momentum accelerating as the year progressed into the fourth quarter.

This combination of improving growth, accommodative policy, and recovering confidence created a favorable backdrop for risk assets. While valuations expanded meaningfully during the rally, they did so from deeply depressed levels following years of market declines.

A Foundation for the Expansion Ahead

By year-end, markets had largely shaken off the trauma of the early 2000s. Although challenges remained, 2003 marked the beginning of a multi-year expansion characterized by improving earnings, expanding participation, and renewed investor engagement. For long-term investors, the year reinforced the importance of staying invested through periods of pessimism and uncertainty, as major turning points often occur when confidence is at its lowest.