A Shift from Recovery to Expansion

By 2004, financial markets were transitioning out of the post-recession recovery phase and into a more mature economic expansion. The U.S. economy entered the year with strong momentum following the fiscal stimulus, tax cuts, and accommodative monetary policy that characterized the early 2000s. Real GDP growth accelerated to approximately 3.9% for the year, supported by robust consumer spending, improving corporate profitability, and a notable rebound in business investment. Equity markets responded favorably, though gains were more measured than the powerful rally seen in 2003, reflecting a shift from valuation-driven upside to earnings-driven returns.

The S&P 500 finished the year up roughly 10.9%. In contrast, the technology-heavy Nasdaq Composite rose approximately 8.6%, lagging the broader market as leadership rotated away from speculative growth toward more cyclical and value-oriented sectors. Markets increasingly focused on sustainability rather than stimulus, and volatility rose modestly as investors adjusted expectations for interest rates and global growth.

The Federal Reserve Begins Normalizing Policy

One of the most important developments of 2004 was the Federal Reserve’s decision to begin raising interest rates after maintaining a historically low federal funds rate of 1.0%. With economic growth firming and concerns emerging about potential inflationary pressures, the Fed initiated its first rate hike in June, beginning a gradual tightening cycle that would continue in subsequent years. By year-end, the policy rate had been increased to 2.25%.

Importantly, the Fed communicated its intentions clearly, repeatedly emphasizing that tightening would proceed at a “measured pace.” This guidance helped prevent market disruption, particularly in fixed income. Treasury yields rose during the first half of the year but ultimately ended lower than many expected, with the 10-year Treasury yield declining from roughly 4.25% to near 4.20%. This counterintuitive move reflected strong global demand for U.S. bonds, subdued inflation expectations, and significant foreign capital inflows.

Energy Prices and Geopolitical Risk

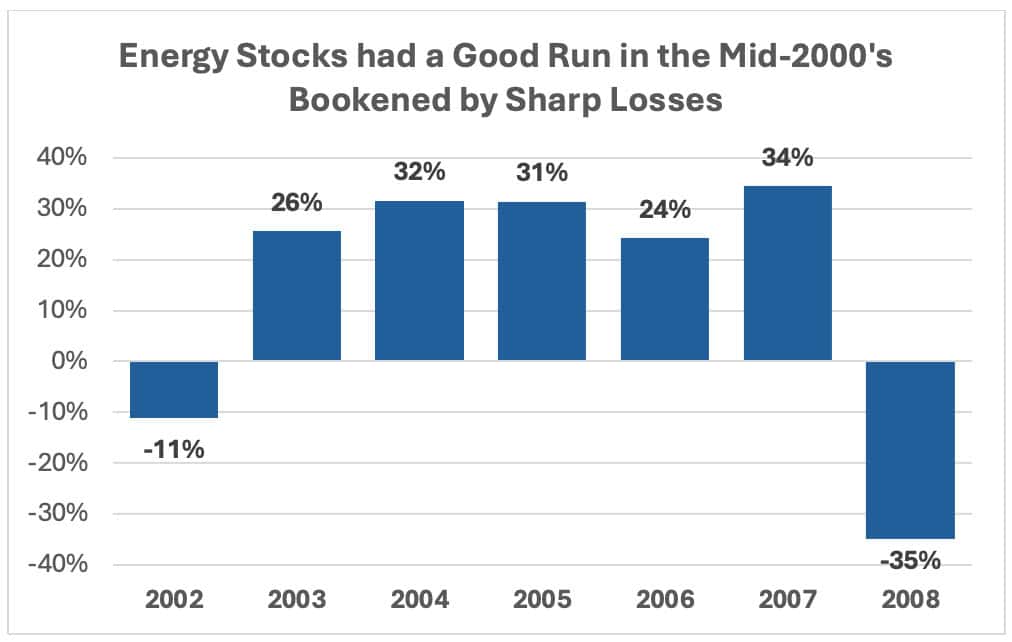

Energy markets emerged as a major theme in 2004, as oil prices climbed sharply amid rising global demand and heightened geopolitical uncertainty. Crude oil prices increased from approximately $32 per barrel at the start of the year to over $45 by year-end, driven by rapid growth in China, supply constraints, and instability in the Middle East, particularly Iraq. The surge in energy prices contributed to higher headline inflation, which averaged around 2.7% for the year, though core inflation remained more contained.

Equity markets absorbed the oil shock relatively well, but sector performance diverged meaningfully. Energy stocks significantly outperformed, benefiting from higher commodity prices and improved cash flows, while transportation and consumer discretionary sectors faced margin pressure. Investors became increasingly aware of energy as a structural, rather than cyclical, input to global growth.

A Weak Dollar and Global Capital Flows

Currency markets also shaped investment outcomes in 2004. The U.S. dollar weakened roughly 7% on a trade-weighted basis, reflecting concerns about persistent current account and fiscal deficits. Large federal borrowing needs and rising trade imbalances weighed on investor confidence in the currency.

A weaker dollar boosted multinational earnings by enhancing the value of overseas revenues, benefiting large-cap companies with significant international exposure. Foreign equity markets delivered strong returns for U.S. investors, as developed international stocks outperformed domestic markets, aided by currency appreciation.

Corporate Earnings and Equity Market Leadership

Corporate earnings growth remained strong, though it moderated from the rebound seen in 2003. S&P 500 earnings increased by approximately 19%, supported by productivity gains and disciplined cost control. However, rising input costs and interest rates began to pressure margins later in the year, contributing to more selective equity performance.

Value stocks outperformed growth stocks as investors favored companies with stable cash flows, reasonable valuations, and pricing power. Financials benefited from rising short-term rates and increased lending activity, while industrials gained from improving capital spending trends. In contrast, segments of the technology sector struggled to regain leadership, as capital expenditure cycles normalized and competitive pressures intensified.

Bonds, Credit Markets, and Portfolio Stability

Despite the Fed’s tightening campaign, bond markets proved resilient. Investment-grade and high-yield credit performed well, supported by low default rates and improving corporate balance sheets. The flattening of the yield curve late in the year signaled market confidence in the Fed’s ability to manage inflation without derailing growth.

For investors, 2004 reinforced the value of diversification during periods of policy transition. Equity returns were positive but uneven, bonds provided stability, and international exposure helped offset domestic volatility. The year marked a clear inflection point – not the end of the expansion, but the beginning of a more globally interconnected and policy-sensitive market environment.