A Year of Calm That Masked Growing Imbalances

For investors, 2006 was a year marked by steady returns, low volatility, and broad confidence in the global economic outlook. Markets benefited from solid growth, rising corporate profits, and supportive financial conditions. Risk appetite remained strong, and concerns about systemic stress were largely absent from investor thinking.

In hindsight, however, 2006 represented a late-stage expansion year in which excesses quietly accumulated beneath the surface. While markets performed well, several structural imbalances were becoming increasingly pronounced, setting the stage for volatility in the years ahead.

Economic Growth Remains Resilient

Global economic conditions in 2006 were generally favorable. The U.S. economy continued to expand at a moderate pace, supported by consumer spending, business investment, and accommodative financial conditions. Corporate earnings growth remained strong, reinforcing confidence in equity markets.

Internationally, growth was even more robust. Emerging markets, led by China and other parts of Asia, expanded rapidly, driving demand for commodities and manufactured goods. Europe also showed signs of renewed momentum after several years of sluggish performance.

Inflation pressures were present but manageable. Energy prices had risen in prior years, but core inflation remained contained, allowing central banks to tighten policy gradually rather than aggressively.

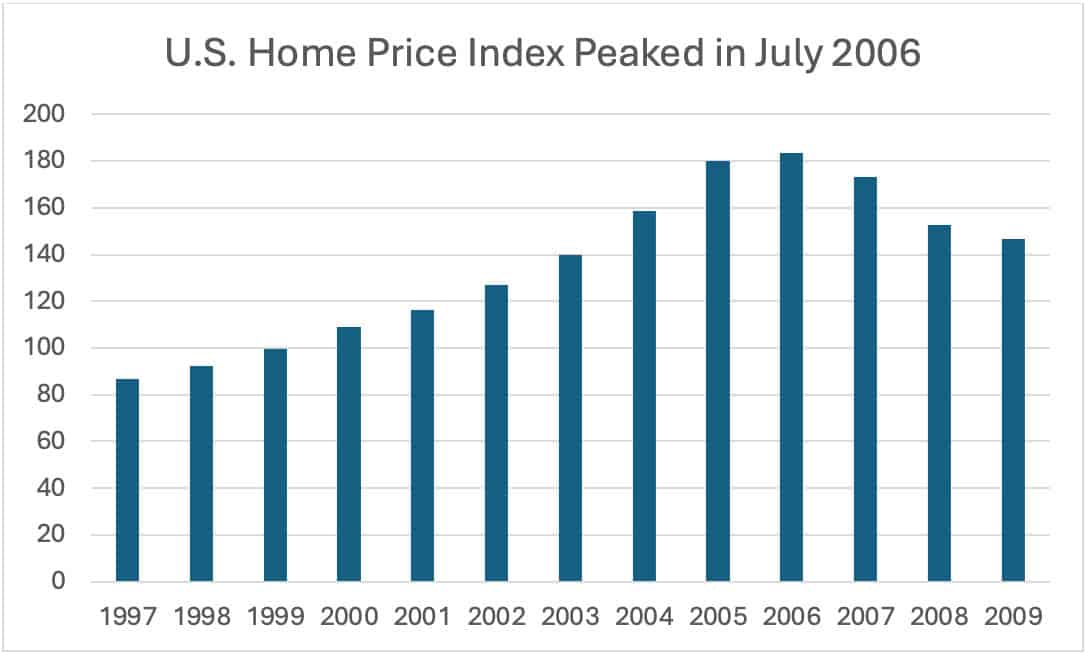

Housing Market Begins to Cool

One of the most important developments of 2006 was the shift in the U.S. housing market. After several years of rapid price appreciation, signs of cooling became increasingly evident. Home sales slowed, inventories rose, and price gains moderated in many regions.

While housing weakness initially appeared orderly, it carried broader implications. Residential investment declined, and concerns began to emerge around mortgage lending practices, particularly in the subprime segment. Adjustable-rate mortgages and relaxed underwriting standards left some borrowers vulnerable to higher payments as interest rates rose.

Despite these early warning signs, markets largely viewed housing softness as a localized issue rather than a systemic threat.

Monetary Policy Tightening Continues

Central bank policy played an important role in shaping market conditions during 2006. The Federal Reserve raised short-term interest rates four times, bringing the federal funds rate to 5.25% by midyear. These moves reflected confidence in economic growth and a desire to prevent inflation from accelerating.

While higher rates began to slow interest-sensitive sectors such as housing, financial conditions remained generally supportive. Credit was readily available, borrowing costs remained reasonable, and investors continued to show a strong appetite for risk.

Bond markets sent mixed signals. The yield curve flattened and briefly inverted, historically a warning sign of slower growth ahead. However, equity markets largely dismissed these signals, focusing instead on strong earnings and global expansion.

Equity Markets Deliver Solid Returns

Equity markets performed well in 2006. The S&P 500 rose approximately 15.8%, supported by healthy corporate profits and continued investor confidence. Gains were relatively broad-based, though leadership rotated throughout the year.

Energy and materials stocks benefited from strong global demand and elevated commodity prices. Financial stocks also performed well, supported by robust lending activity and stable credit conditions. Meanwhile, defensive sectors lagged as investors favored growth-oriented and cyclical areas of the market.

International equities posted solid gains as well, particularly in emerging markets, reinforcing enthusiasm for global diversification.

Credit Markets Reflect Optimism

Credit markets remained calm and supportive throughout 2006. Corporate bond spreads stayed narrow, reflecting low perceived default risk and strong investor demand for yield. Structured credit products grew rapidly in popularity, offering higher returns in exchange for increased complexity.

This environment encouraged leverage and risk-taking across the financial system. While returns were attractive, the widespread assumption that volatility would remain low contributed to complacency among investors, portfolio managers, and lenders across multiple asset classes.

A Year of Confidence and Complacency

By year-end, investor sentiment remained optimistic. Markets had delivered steady gains, volatility was subdued, and economic growth appeared durable. Few anticipated the magnitude of challenges that would emerge in the years ahead.

For long-term investors, 2006 serves as a reminder that periods of stability can coincide with the buildup of hidden risks. Strong returns and calm markets, while welcome, do not eliminate the need for diversification, discipline, and attention to underlying fundamentals. These lessons, while subtle at the time, would become far clearer as market conditions shifted dramatically in subsequent years.