A Year That Began Calmly and Ended in Crisis

For much of 2007, markets appeared stable and resilient. Economic growth was slowing modestly, but corporate earnings remained strong, credit was widely available, and volatility stayed unusually low. Beneath the surface, however, structural weaknesses were building within the financial system. What began as isolated stress in housing and credit markets gradually evolved into a broader loss of confidence by year-end.

In hindsight, 2007 stands as the opening chapter of the global financial crisis (GFC)—a year when risks long ignored began to surface, reshaping market behavior and investor expectations.

Housing Weakness Exposes Credit Vulnerabilities

The first signs of trouble emerged from the U.S. housing market. After years of rising home prices, affordability deteriorated, demand softened, and price declines began in several regions. Defaults increased, particularly among subprime borrowers who had relied on adjustable-rate mortgages and loose lending standards.

As housing conditions worsened, losses spread into mortgage-backed securities. Many of these securities were held by banks, hedge funds, and institutional investors, often with significant leverage. Because these instruments were complex and opaque, uncertainty about their true value quickly became a source of concern, increasing skepticism across credit markets and risk-sensitive asset classes.

At first, markets treated housing problems as contained. However, as losses mounted and funding conditions tightened, investors began to reassess credit risk more broadly.

Credit Markets Tighten and Volatility Returns

By mid-2007, stress in credit markets became increasingly visible. Several hedge funds tied to subprime mortgages failed, and banks grew more cautious in lending to one another. Liquidity in short-term funding markets declined, and credit spreads widened, signaling rising risk aversion and reduced willingness to extend capital.

In August, global equity markets experienced a sharp sell-off as investors reacted to growing uncertainty. Although markets recovered partially in subsequent months, volatility remained elevated compared to the unusually calm conditions of prior years.

Central banks responded by injecting liquidity into the financial system. The Federal Reserve began cutting interest rates late in the year, signaling concern about tightening financial conditions and slowing economic growth. These actions helped stabilize markets temporarily, but underlying issues remained unresolved.

Equity Markets Mask Growing Risks

Despite mounting concerns, equity market performance in 2007 was relatively mixed rather than disastrous. The S&P 500 finished the year with a modest gain of approximately 5%, though returns were uneven and concentrated earlier in the year. Markets peaked in October before declining sharply into year-end as financial stress intensified.

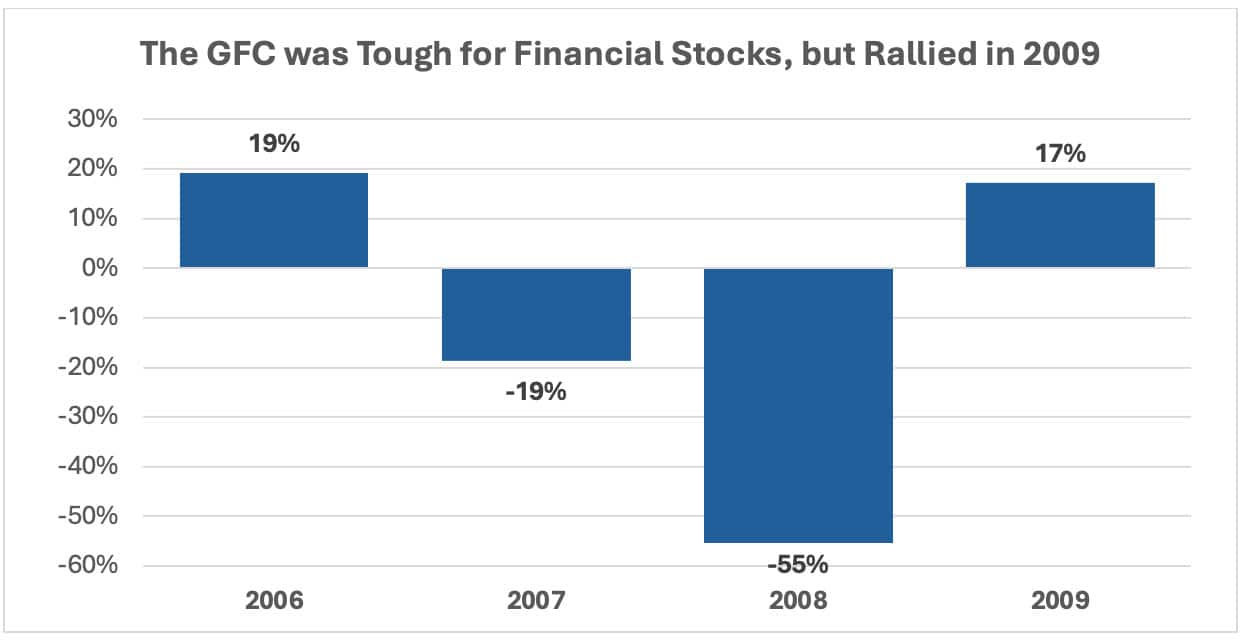

Leadership narrowed as defensive sectors began to outperform. Financial stocks weakened significantly as investors questioned balance sheet strength and exposure to mortgage-related assets. In contrast, energy and commodity-related stocks benefited from rising oil prices and strong global demand earlier in the year.

International markets showed similar patterns. While global equities posted gains earlier in the year, concerns about U.S. housing and global credit conditions weighed increasingly on investor sentiment.

Bond Markets Signal Rising Concern

Bond markets provided clearer warnings than equities. Credit spreads widened steadily as investors demanded higher compensation for risk. While high-quality government bonds performed relatively well during periods of market stress, lower-quality credit faced mounting pressure.

The yield curve began to reflect expectations of slower growth and further monetary easing. These signals suggested that bond investors were increasingly focused on downside risks, even as equity markets remained comparatively resilient for much of the year.

Economic Growth Slows but Remains Positive

Economically, 2007 was a year of deceleration rather than collapse. U.S. growth slowed as housing activity declined, but consumer spending and business investment remained supported for much of the year. Employment conditions weakened gradually, though unemployment remained relatively low by historical standards.

This divergence between weakening financial conditions and still-positive economic data contributed to investor confusion. Markets struggled to assess whether housing-related stress would remain isolated or evolve into a broader economic downturn.

Lessons from a Transitional Year

By the end of 2007, confidence had clearly eroded. Investors entered 2008 facing heightened uncertainty, tighter credit conditions, and growing concerns about systemic risk. While the full magnitude of the crisis was not yet apparent, the warning signs were firmly in place and increasingly difficult to ignore.

For long-term investors, 2007 reinforced the importance of understanding risk beneath the surface, maintaining diversification, and recognizing that periods of apparent stability can mask developing vulnerabilities. The year served as a reminder that market cycles often turn gradually at first—before accelerating rapidly once confidence breaks and conditions deteriorate.