A Year of Steady Progress Amid Growing Global Imbalances

At first glance, 2014 appeared relatively calm compared with the dramatic market cycles that preceded and followed it. Equity markets advanced steadily, volatility remained contained for much of the year, and economic conditions in the United States continued to improve. Yet beneath the surface, 2014 was a year in which important global imbalances widened, quietly reshaping the investment landscape and laying groundwork for future volatility.

For long-term investors, 2014 reinforced the idea that markets do not need excitement to deliver returns—but periods of calm often coincide with meaningful structural change.

The U.S. Economy Pulls Away from the Rest of the World

A defining theme of 2014 was the increasing divergence between the U.S. economy and much of the global economy. In the United States, growth strengthened as employment gains accelerated, consumer spending improved, and corporate profits remained resilient. The unemployment rate declined steadily during the year, ending near 5.6%, reflecting continued healing in the labor market.

In contrast, economic conditions abroad were far less favorable. Europe struggled with sluggish growth and mounting deflationary pressures, while Japan’s economy faltered despite aggressive monetary stimulus. China’s growth rate continued to slow as policymakers attempted to rein in excess credit growth and shift the economy toward consumption rather than heavy industry.

These differences mattered for markets because capital increasingly flowed toward regions offering stronger growth and policy stability, particularly the United States.

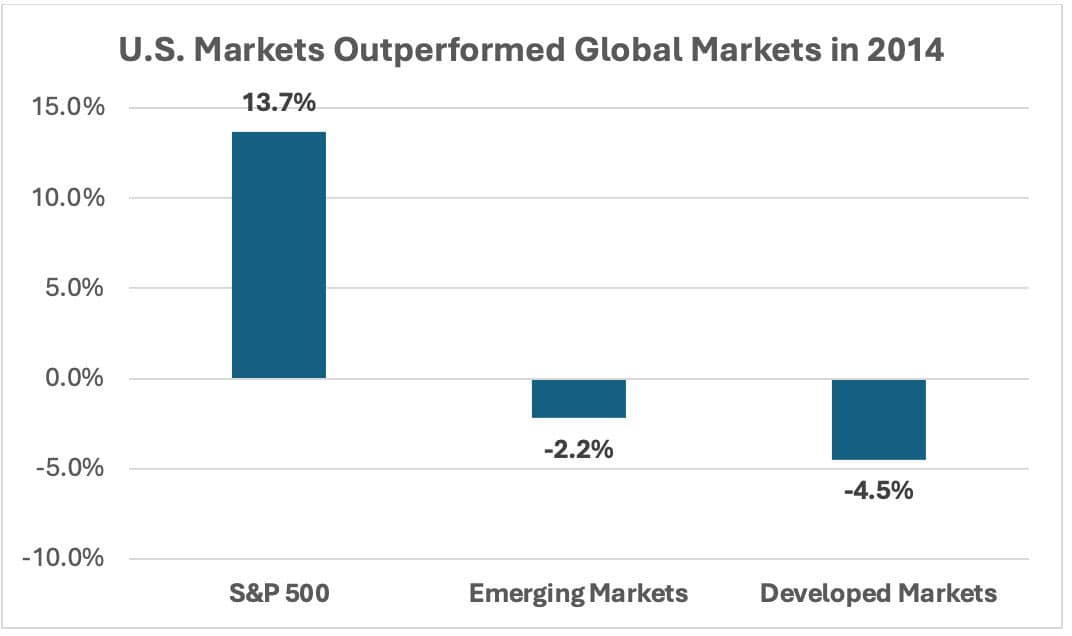

Equity Markets Advance at a Measured Pace

U.S. equity markets delivered solid, though more moderate, returns in 2014. The S&P 500 gained approximately 13.7% for the year, marking its third consecutive year of double-digit gains. The Dow Jones Industrial Average rose roughly 7.5%, while the Nasdaq Composite advanced about 13%.

Unlike prior years, market leadership took on a more defensive character. Healthcare and consumer staples performed well, reflecting investor preference for stable earnings and predictable cash flows. Technology stocks also contributed meaningfully, though returns were less speculative than in later years.

Markets experienced several notable pullbacks, including a sharp decline in October driven by concerns over global growth and geopolitical tensions. Each episode, however, proved temporary, as investors continued to view weakness as an opportunity rather than a warning sign.

Oil Prices Collapse and Redefine Market Expectations

One of the most significant developments of 2014 was the sharp decline in oil prices. Crude oil fell from over $100 per barrel in mid-year to below $60 by December. The decline was driven by a combination of rising U.S. shale production, weakening global demand, and OPEC’s decision not to cut output in order to protect market share.

For consumers, lower oil prices functioned as a tax cut, supporting household spending and confidence. For investors, however, the impact was more complex. Energy company earnings declined sharply, capital spending plans were reduced, and credit conditions for energy-related borrowers began to tighten.

Bonds Defy Expectations

Fixed income markets surprised many investors in 2014. Despite widespread expectations that interest rates would rise as the economic recovery progressed, bond yields moved lower. Slowing global growth and falling inflation expectations pushed investors toward high-quality bonds.

The 10-year U.S. Treasury yield declined from roughly 3.0% at the start of the year to approximately 2.2% by year-end. The Bloomberg U.S. Aggregate Bond Index returned about 6%, providing meaningful diversification benefits during periods of equity volatility.

Once again, bonds demonstrated their role as a stabilizing force in balanced portfolios, even in an environment of improving domestic growth.

A Stronger Dollar Emerges

Another important trend in 2014 was the strengthening of the U.S. dollar. As global growth diverged and investors anticipated tighter U.S. monetary policy relative to other regions, capital flowed into dollar-denominated assets.

While a stronger dollar helped keep inflation low in the United States, it created headwinds for multinational corporations and emerging markets. Currency pressures began to build overseas, foreshadowing challenges that would become more pronounced in subsequent years.

Looking Back at 2014

By the end of 2014, investors had experienced a year of steady progress rather than dramatic change. Yet beneath the surface, falling commodity prices, diverging global growth, shifting currency dynamics, and evolving investor preferences were reshaping the market environment.

For disciplined investors, 2014 reinforced the importance of diversification, patience, and a long-term perspective during periods when markets appear calm but structural forces are quietly at work.