A Year of Transition, Volatility, and Uneven Market Outcomes

After several years of strong and relatively steady gains, 2015 marked a meaningful shift in market behavior. Investors entered the year expecting continued progress, supported by economic expansion in the United States and the belief that the Federal Reserve’s first interest rate increase would signal confidence in growth. Instead, markets encountered rising volatility, slowing global momentum, and a series of interconnected events that repeatedly disrupted confidence.

Rather than a single defining shock, 2015 unfolded as a sequence of setbacks. Each episode—tied to global growth concerns, currency movements, or commodity weakness—interrupted market momentum. While the U.S. economy avoided recession, markets struggled to advance, reflecting the challenges that often emerge during periods of transition in the global economic cycle.

Global Growth Concerns and China Take Center Stage

One of the most important stories of 2015 was the growing concern over global economic growth, particularly in China. After years of rapid expansion fueled by exports, infrastructure investment, and credit growth, China began showing signs of strain. Manufacturing activity slowed, excess industrial capacity became evident, and policymakers sought to rebalance the economy toward consumer-driven growth.

These pressures came to a head in August, when Chinese equity markets fell sharply and authorities unexpectedly devalued the yuan. The move was intended to support exports by making Chinese goods more competitive globally and to stabilize slowing economic momentum. However, the decision surprised markets and raised fears that China’s slowdown was more severe than previously acknowledged.

The market reaction was swift. Global equities sold off sharply, volatility spiked, and investors reduced exposure to risk assets. The S&P 500 fell more than 10% in a matter of days, while emerging markets and commodity-producing economies experienced even steeper declines. Although markets stabilized in subsequent weeks, confidence was clearly shaken.

Equity Markets Struggle to Gain Traction

U.S. equity markets delivered disappointing results in 2015. The S&P 500 finished the year with a small positive return (+1.4%), while the Dow Jones Industrial Average declined modestly. The Nasdaq Composite posted a slight gain, supported largely by a narrow group of large-cap technology stocks.

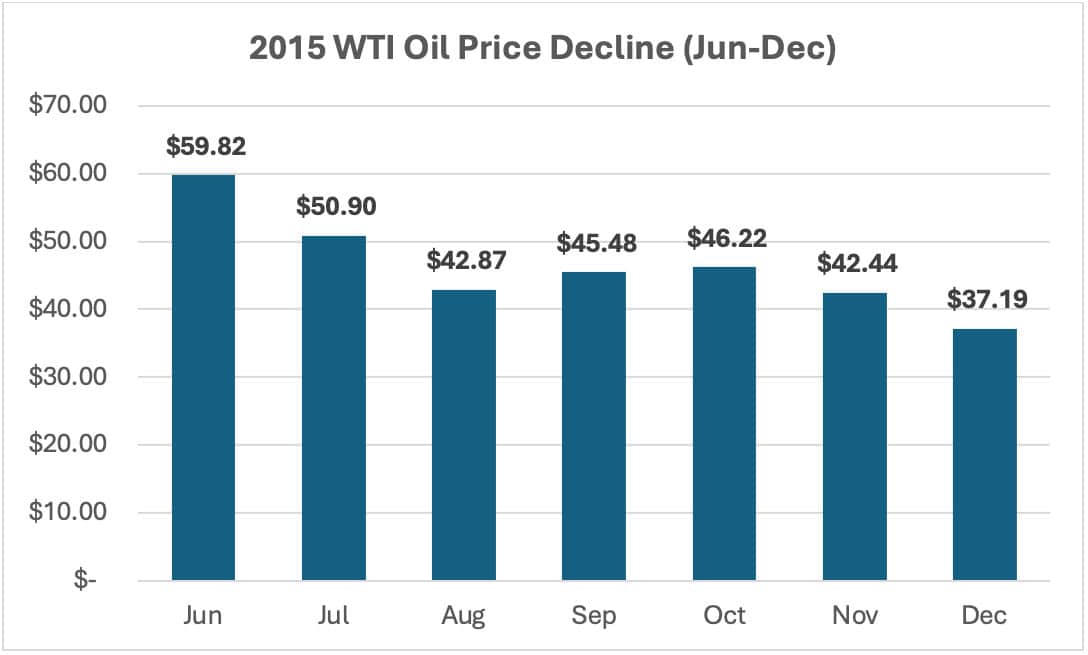

Market leadership narrowed significantly, in part due to the collapse in energy prices. Oil prices fell sharply throughout the year as global supply exceeded demand. Advances in U.S. shale production, combined with OPEC’s decision not to cut output, created a supply glut. At the same time, slowing growth in China and other emerging markets reduced demand expectations, pushing crude oil prices down from roughly $53 per barrel at the start of the year to near $37 by December.

This decline weighed heavily on energy companies, leading to reduced capital spending, layoffs, and rising credit concerns within the sector. Materials stocks also struggled as commodity prices broadly weakened.

Volatility became a defining feature of the year. In addition to the August selloff, markets experienced renewed weakness in September and again late in the year as investors struggled to regain confidence in global growth and earnings momentum.

Federal Reserve Prepares for Liftoff

Monetary policy remained a central focus throughout 2015 as investors anticipated the Federal Reserve’s first interest rate increase since 2006. As expectations for policy tightening grew, the U.S. dollar strengthened significantly. While a strong dollar helped keep inflation low, it also created headwinds for multinational companies by reducing the value of overseas earnings and making U.S. exports less competitive.

After months of debate, the Fed raised interest rates by 25 basis points in December. While widely expected, the move marked a symbolic turning point, ending nearly a decade of ultra-low rates. Importantly, policymakers emphasized that future increases would be gradual, helping prevent a sharper market reaction.

Bonds Provide Stability but Limited Returns

Fixed income markets provided stability during periods of equity stress, though returns were modest. The Bloomberg U.S. Aggregate Bond Index posted a small positive return for the year. Treasury bonds benefited during risk-off episodes, particularly during the August selloff, as investors sought safety.

The U.S. Dollar and Corporate Earnings Pressure

The strong U.S. dollar became a persistent headwind for corporate earnings in 2015. Many large companies reported that currency effects reduced reported revenue and profit growth, even when underlying demand remained stable. This contributed to slower earnings growth overall and reinforced investor preference for domestically focused businesses.

Looking Back at 2015

By the end of 2015, investors had navigated a year shaped by interconnected global forces. Slowing growth in China, collapsing commodity prices, currency shifts, and the beginning of U.S. monetary tightening combined to create a challenging environment. While returns were muted and volatility increased, the year helped reset expectations and highlighted the importance of understanding how global economic forces influence markets over time.