A Year Marked by Policy Tightening, Volatility, and a Sharp Shift in Investor Confidence

After several years of steady gains and subdued volatility, 2018 delivered a stark change in market conditions. Investors entered the year optimistic about synchronized global growth, strong corporate earnings, and the benefits of U.S. tax reform. However, as the year progressed, tightening monetary policy, rising interest rates, and escalating trade tensions undermined confidence and exposed weaknesses across global markets.

By year-end, markets were dealing with heightened uncertainty, increased volatility, and growing concerns that policy tightening had gone too far.

Federal Reserve Tightening Reshapes the Investment Landscape

The dominant force shaping markets in 2018 was the Federal Reserve’s commitment to continued monetary tightening. Building on prior increases, the Fed raised interest rates four times during the year, bringing the federal funds target range to 2.25%-2.50% by December. Policymakers emphasized confidence in economic strength and downplayed market volatility, reinforcing expectations that policy normalization would continue.

Rising rates pushed the 10-year Treasury yield above 3% in October, its highest level in seven years. This move placed pressure on equity valuations, particularly for growth-oriented stocks, and tightened financial conditions across the economy. Borrowing costs increased for corporations and consumers alike, while the U.S. dollar strengthened, weighing on multinational earnings and emerging markets.

Markets grew increasingly sensitive to Fed communications, with investor sentiment deteriorating as concerns mounted that policy tightening could slow economic growth more than intended.

Equity Markets Struggle Under Volatility and Valuation Pressure

Equity markets delivered negative returns in 2018, marking the first down year for U.S. stocks since 2008. The S&P 500 declined approximately -4.4% for the year, while the Dow Jones Industrial Average fell roughly -5.6%. The Nasdaq Composite fared modestly better but still finished down about -3.9%, as technology stocks experienced sharp swings.

Volatility surged, particularly during February and again in the fourth quarter. The final three months of the year proved especially challenging, with equities selling off sharply amid fears of slowing global growth, tightening liquidity, and ongoing trade disputes. December alone saw the S&P 500 decline nearly -9%, its worst December performance since the Great Depression era.

Leadership within the market narrowed significantly. Defensive sectors such as utilities and consumer staples held up relatively well, while interest-rate-sensitive and cyclical areas faced meaningful pressure. Small-cap stocks initially benefited from domestic exposure but ultimately declined as financial conditions tightened further.

Trade Tensions Add to Global Growth Concerns

Trade policy uncertainty intensified throughout 2018, contributing to market volatility and weakening business confidence. The United States imposed tariffs on a wide range of imports, particularly from China, prompting retaliatory measures and increasing concerns about global supply chains.

Manufacturing indicators softened globally, with signs of slowing growth emerging in Europe and Asia. Emerging markets were hit especially hard, as a stronger U.S. dollar and rising U.S. interest rates led to capital outflows and currency pressure. Equity markets in several developing economies experienced double-digit declines, reinforcing risk aversion among global investors.

While trade tensions were not the sole driver of market weakness, they compounded concerns already present from tightening monetary policy and late-cycle economic dynamics.

Bonds Offer Limited Protection as Rates Rise

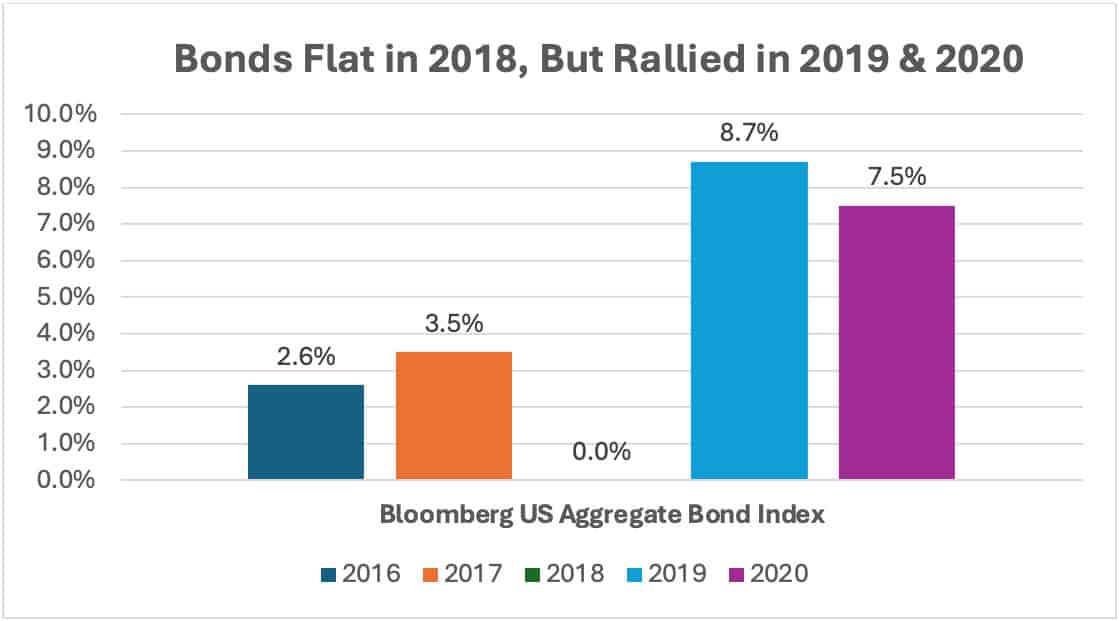

Unlike many prior periods of equity weakness, fixed income offered limited downside protection in 2018. Rising interest rates weighed on bond prices, resulting in modest losses across much of the bond market. The Bloomberg U.S. Aggregate Bond Index was basically flat for the year.

Shorter-duration bonds held up better, while longer-duration Treasuries experienced price pressure as yields rose. Credit markets remained relatively stable for much of the year, supported by solid corporate fundamentals, though spreads widened modestly during the fourth-quarter selloff.

The combination of equity and bond declines challenged traditional diversification assumptions, but both asset classes rallied strongly the following year, proving that patience and discipline are needed during challenging times.

Looking Back at 2018

By the end of 2018, investors were left navigating a very different environment than the one that had prevailed for much of the decade. Markets had transitioned from policy support to policy restraint, from complacency to volatility, and from valuation expansion to contraction. The year served as a reminder that late-cycle dynamics can unfold quickly, and that shifts in monetary policy often carry significant consequences for asset prices, setting the stage for the dramatic reversal that followed in 2019.