Entering 2020, markets were supported by steady economic growth, low inflation, and accommodative central bank policy. Few could have predicted that a global pandemic would abruptly reshape the economic landscape, disrupt daily life, and test investor discipline on such an extreme scale.

What followed was a year defined by extremes—historic market declines, unprecedented policy intervention, and a powerful recovery that rewarded patience and long-term perspective.

An Abrupt Shock to the Global Economy

In February and March, the rapid spread of COVID-19 triggered a sudden halt in global economic activity. Governments implemented widespread lockdowns, travel ground to a near standstill, and entire industries faced abrupt revenue losses. Financial markets responded swiftly and forcefully.

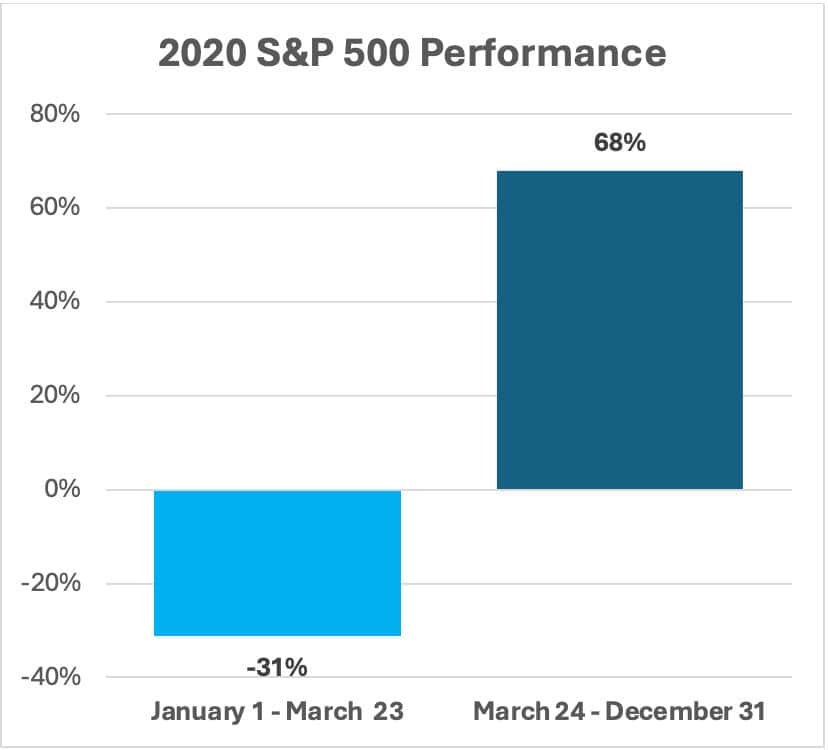

Between February 19 and March 23, the S&P 500 fell more than 30%, marking the fastest descent into a bear market on record. Volatility surged well above levels seen during the Global Financial Crisis. Credit markets also experienced significant stress, as investors rushed to raise cash and liquidity became scarce. Investment-grade credit spreads widened dramatically, and even high-quality bonds saw price declines.

For investors, the speed of the selloff was as unsettling as its magnitude. Traditional diversification provided limited protection in the short term as stocks and bonds tended to react in similar ways to the large shocks. The environment challenged even disciplined investors, as fear and uncertainty dominated investor reactions.

Unprecedented Policy Response and Market Stabilization

Faced with a rapidly deteriorating economic outlook, policymakers responded with extraordinary speed and scale. In March, the Federal Reserve cut interest rates to near zero and relaunched large-scale asset purchases. Over the course of the year, the Fed’s balance sheet expanded from roughly $4 trillion to more than $7 trillion.

Importantly, the Fed went beyond traditional measures, announcing facilities to support corporate bond markets, municipal debt, and short-term funding markets. While actual bond purchases were limited, the signaling effect alone helped restore confidence and stabilize credit conditions. Investment-grade issuance rebounded quickly, and borrowing costs fell to historic lows for many large companies.

Fiscal policy played a critical role as well. Congress approved multiple stimulus packages totaling more than $3 trillion, including direct payments to households, enhanced unemployment benefits, and support for small businesses. Together, these measures helped cushion the economic shock and laid the groundwork for recovery.

For investors, 2020 reinforced the growing importance of policy in shaping market outcomes. Monetary and fiscal tools became central forces, influencing not just economic conditions but also risk appetite and asset pricing.

A Powerful and Unexpected Market Recovery

Markets reached their lows in late March and then began a recovery that proved both swift and resilient. By year-end, the S&P 500 had gained approximately 68% from its trough, finishing 2020 up about 18% overall. This occurred despite a sharp economic contraction, with unemployment peaking near 15% in April and GDP experiencing its steepest quarterly decline on record.

The recovery highlighted the forward-looking nature of financial markets. Investors began anticipating economic recovery, continued policy support, and persistently low interest rates well before economic data improved meaningfully.

Market performance, however, was uneven. Large-cap U.S. stocks significantly outperformed small-cap and international equities for much of the year, and style leadership skewed strongly toward growth over value.

Technology Leadership and Structural Change

Technology and technology-enabled companies were clear beneficiaries of the pandemic-driven environment. The rapid adoption of remote work, e-commerce, digital payments, and cloud computing accelerated trends that had already been underway. As a result, companies such as Apple, Microsoft, Amazon, and other large-cap growth stocks accounted for a substantial portion of market returns.

By year-end, the five largest companies in the S&P 500 represented more than 20% of the index’s total market capitalization, reflecting both strong fundamentals and increased market concentration. While this raised reasonable questions about valuation and diversification, it also underscored how quickly economic leadership can shift during periods of disruption.

At the same time, many cyclical sectors struggled. Energy stocks declined sharply as oil prices briefly turned negative in April, while travel-related industries faced ongoing uncertainty. These divergences highlighted the uneven economic impact of the pandemic and reinforced the importance of diversified portfolio construction.

Perspective at Year-End

From an investment standpoint, 2020 reinforced several key investment principles. Markets can react violently to unexpected shocks, but they can also recover well before uncertainty fades. Policy support can play a decisive role during periods of crisis, and attempting to time markets during extreme volatility often yields poor results.

Investors who maintained a disciplined, long-term approach were ultimately rewarded, while those who reacted to short-term fear faced the difficult challenge of re-entering markets after prices had already moved higher.