Investors with over $1 million in investable assets have an interest in maintaining control, tax-efficiency, and transparency, often putting them at a disadvantage when investing in pooled bond funds. While bond funds may seem like a simple and convenient way to gain exposure to fixed income, they come with several drawbacks that make them less suitable for investors with substantial wealth. These drawbacks include reduced yield potential, higher costs, and less control over portfolio management. On top of those drawbacks are the lack of transparency into what the real yield and holdings are. Here’s 6 reasons investors with over $1 million should avoid bond funds:

1. Reduced Yield Potential

One of the primary issues with pooled bond funds is their exposure to older, lower-yielding bonds. Bond funds typically hold a mixture of bonds acquired over a wide range of time periods, many of which may have been purchased during times of lower interest rates. Some of these bonds bought prior to you investing in the fund may carry high prices and low yields-to-maturity. For example, bond funds that were built over the past decade may still hold a substantial amount of bonds that yield only 1-2%, reflecting the ultra-low interest rate environment of recent years.

Affluent investors, who can afford to directly invest in bonds through a separately managed account, have a significant advantage in this scenario. With direct ownership, investors can specifically choose newly issued bonds that reflect current market yields. In contrast, the bond fund investor is stuck with a blended yield that incorporates older bonds, leading to subpar returns in a rising interest rate environment. This yield drag can have a long-term negative impact on the investor’s overall return.

Example: Imagine a bond fund with an average yield of 2.5%, while new bonds in the current market offer 5%. A direct investor can target these higher-yielding bonds, while the bond fund investor’s returns are diluted by the fund’s outdated holdings.

2. Annual Advisor Fees

Some investment advisors will relay their fee information but leave out the fact that it is just the tip of the iceberg. Because investment advisors are charging a fee for advice, not for the management of the funds, as an investor you’re still subject to the other fund costs that impact your results.

3. Higher Costs and Expense Ratios

Another drawback of pooled bond funds is the layering of fees and expenses that erode returns. Affluent investors, who typically prioritize cost-efficiency, may be shocked to find that many bond funds charge expense ratios that can significantly eat into the income generated by the bonds themselves. In addition, bond funds may have embedded sales fees, 12b-1 fees, and other administrative costs that further reduce net returns.

With direct bond ownership, investors eliminate many of these fees. The primary costs for direct investing come from the initial purchase and any potential trading costs, but they are often far lower than the ongoing expense ratios of bond funds. Over time, the reduced fee burden of direct investing can translate into a higher total return.

Example: An affluent investor holding a $2 million bond portfolio in a pooled fund with a 0.75% expense ratio would pay $15,000 annually in fees, regardless of how well the bonds perform. In contrast, direct investors who buy bonds through an separately managed account may incur lower costs, improving their net income.

4. Lack of Control and Exposure to Herding Behavior

Pooled bond funds are subject to the behavior of other investors, particularly during times of market stress. When markets fall and redemptions increase, fund managers are often forced to sell bonds, regardless of whether the timing is optimal. This reactionary selling can occur at inopportune moments, locking in losses and reducing the overall value of the fund for remaining investors. This herding behavior, driven by panic selling, disproportionately affects funds with a high number of small retail investors.

Affluent investors who directly own bonds through an separately managed account are insulated from this forced selling. They maintain control over their portfolio, allowing them to ride out periods of market volatility without the fear of others’ decisions negatively impacting their investments. This control is crucial during downturns, when making strategic decisions is often the key to protecting wealth.

Example: In the 2008 financial crisis, many bond funds experienced significant losses as redemptions surged, forcing managers to sell bonds at fire-sale prices. Direct investors who held individual bonds were able to wait out the storm and avoid locking in losses.

5. Pricing disadvantages

When buying into a bond fund, you are buying shares of the fund not the underlying bonds themselves. Because most bond funds own bonds that were bought years ago, many will have high premiums that may mean the yield-to-maturity is quite low, relative to today’s bonds. In short, high bond prices with yields of 1% or 2% before fees are not very attractive.

6. Historical Results Mean Little

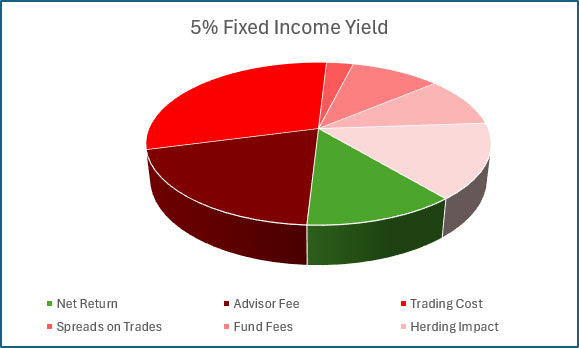

Because bond funds are pooled with no direct ownership, the historical results have little to do with your actual individual result. For example, if rates go down and bond prices increase, bond fund prices increase as well. A bond fund may hold bonds that have an average yield to maturity of 3% before accounting for the investment advisors fee of 1%. Because rates went down the previous year, the prices of bonds within the fund went up – pushing the overall annual return to 8%. 5% of this 8% was due to bond prices going up, and 3% was the net yield. The actual net take-home was 2% because the overall results from the following year were impacted by bond prices going up, not an increase in yield to the investor. As an investor, be aware that historical results may not help guide you to your future needs.

Conclusion

For affluent investors, pooled bond funds present several challenges that undermine the core reasons for investing in fixed income: stability, predictability, and reliable income. Between the reduced yield potential due to older bonds, the ongoing costs associated with expense ratios and fees, and the lack of control during market volatility, bond funds often fall short of delivering the benefits that high-net-worth individuals expect. Direct bond ownership, by contrast, offers these investors the opportunity to maximize yields, minimize costs, and maintain full control over their portfolio, ensuring that their fixed-income investments work efficiently to meet their long-term financial goals.

Related Articles

Why to Invest in Bonds and Where to Buy Them

Fixed Income,

Why to Buy & Where,

September 24, 2024

Should I worry about index funds pooled ownership?

Index Investing,

Investment Principles,

Top Index FAQs,

Top Investment Principles FAQs,

October 23, 2023

What is the Difference Between Market-Cap Index Funds and Equal Weighted Index Funds?

Investment Principles,

November 19, 2024