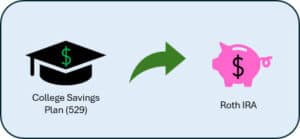

When it comes to planning for a child’s education, many parents turn to 529 Plans as a way to save and invest for future education expenses. However, as children grow older and get closer to college age, some parents may start to wonder what to do with excess money in these plans. One option that has gained popularity in 2024 is rolling a 529 Plan into a Roth IRA.

While withdrawing funds from a 529 and funding a Roth IRA came with penalties before 2024, the implementation of the SECURE 2.0 Act made this strategy more appealing.

This move can have both costs and benefits, depending on the individual circumstances of the account holder. In this article, we will explore the costs and benefits of rolling a 529 Plan to a Roth IRA, and provide specific examples and details to help you determine if this strategy may be right for you.

This move can have both costs and benefits, depending on the individual circumstances of the account holder. In this article, we will explore the costs and benefits of rolling a 529 Plan to a Roth IRA, and provide specific examples and details to help you determine if this strategy may be right for you.

Costs:

- Tax implications: One of the biggest costs of rolling a 529 Plan into a Roth IRA is the potential tax implications. When you roll over funds from a 529 Plan to a Roth IRA, you are essentially converting the funds from a tax-deferred account to a tax-free account. This means that you will pay taxes on any gains in the 529 Plan that are rolled over.

- For example, let’s say you put $4,000 in a 529 Plan that has grown to $7,000 over the years. If you decide to roll over the funds to a Roth IRA, you will need to pay taxes on earnings. Depending on your tax bracket, this could result in a significant tax bill.

- Penalties: Before the Secure 2.0 Act went into effect in 2024, withdrawals from a 529 for any reason other than qualified educational expenses were subject to a 10% penalty. The new rules allow a rollover from a 529 to the 529 beneficiaries Roth IRA.

- Secure 2.0 Act: There are some requirements for executing this rollover without penalty:

- The account must have been open for at least 15 years.

- The money must be transferred according to annual Roth IRA contribution limits.

- The lifetime maximum for this rollover is $35,000 per beneficiary. Since the 2024 Roth IRA contribution limits for most people are $7,000/yr, rolling over $35,000 to a Roth IRA would need to be done over the course of 5 years.

- Just like a regular Roth IRA contribution, the beneficiary’s contribution limit (for someone under 50) is $7,000 or their earned income for the year, whichever is lower.

- The amount of each rollover cannot exceed the aggregate amount of contributions (and earnings attributable thereto) made earlier than the 5-year period before the date of the rollover.

- There are no income-based phaseouts for a 529-to-Roth rollover.

- Many (but not all) states conform to the Federal law treating 529-to-Roth rollovers. In some states, particularly where a tax deduction or credit is received for contributing to a 529, the beneficiary will need to factor in the state tax implications.

Note: A sharp-eyed financial planner might ask if a parent could roll their child’s 529 account into their own Roth IRA. In theory, this could be done by changing the beneficiary of the 529 to the parent, then executing the Roth conversion to the parent’s Roth IRA. However, the IRS has not yet clarified (as of 11/8/24) whether changing the beneficiary on a 529 resets the 15-year waiting period mentioned above. For this reason, it is better to await IRS guidance and use caution when updating beneficiaries.

Benefits:

- Flexibility: One of the key benefits of rolling a 529 Plan to a Roth IRA is increased flexibility. While 529 Plans are specifically designed for education expenses, Roth IRAs can be used for a variety of purposes, including retirement, certain emergencies, or even a down payment on a house.

- This flexibility can be particularly valuable if your child decides not to pursue higher education or receives grants and/or scholarships that cover their expenses. By rolling over the funds to a Roth IRA, you can ensure that the money will not go to waste and be used for other purposes.

Tax-free growth potential: Another significant benefit of rolling a 529 Plan to a Roth IRA is the ability to take advantage of potential tax-free growth. Unlike 529 Plans, which offer tax-deferred growth potential on earnings, Roth IRAs provide tax-free growth potential on both contributions and earnings.

Tax-free growth potential: Another significant benefit of rolling a 529 Plan to a Roth IRA is the ability to take advantage of potential tax-free growth. Unlike 529 Plans, which offer tax-deferred growth potential on earnings, Roth IRAs provide tax-free growth potential on both contributions and earnings.- This means that any funds you contribute to a Roth IRA, as well as any earnings generated by those funds, can grow tax-free for as long as they remain in the account. This can result in significant savings over time, especially if you have many years until retirement.

- Estate planning: Rolling a 529 Plan to a Roth IRA can also offer benefits in terms of estate planning. Unlike 529 Plans, which are considered assets of the account owner, Roth IRAs can be passed on to beneficiaries tax-free.

- This means that if you pass away before using all of the funds in the Roth IRA, your beneficiaries can inherit the account and continue to benefit from the amount you accumulated. This can be a valuable way to pass on wealth to future generations while minimizing tax implications.

In conclusion, rolling a 529 Plan to a Roth IRA can have both costs and benefits. While there may be tax implications associated with the rollover, the increased flexibility, tax-free growth potential, and estate planning benefits can make this strategy worth considering for some investors. As with any financial decision, it is important to carefully weigh the costs and benefits before making a final decision. Consulting with a financial professional can also help you determine if rolling a 529 Plan to a Roth IRA is the right move for your individual situation.