Delistings are an often overlooked factor in investment performance, but their impact can be significant, particularly when it comes to index funds. Whether due to mergers, bankruptcies, or companies going private, delistings can affect both individual stockholders and those who invest through index funds. For investors focused on maximizing returns and minimizing risks, understanding how delisting works and its implication is critical.

What is a Delisting?

A delisting occurs when a company’s stock is removed from a stock exchange which can happen voluntarily or involuntarily. This creates liquidity issues, as delisted stocks are typically harder to trade and the resulting loss of liquidity often translates into a significant loss in value for shareholders.

Types of Delistings:

- Voluntary Delistings: When a company opts to leave the stock exchange, typically because it wants to go private or it is merging with another firm.

- Involuntary Delistings: These occur when a company is forced off an exchange due to poor financial performance, the stock’s share price falling below a minimum threshold, or failure to comply with regulatory requirements.

Impact on Index Funds

Index funds, by design, track a specific index like the S&P 500 or the NASDAQ Composite. When a stock within the index is delisted, the fund must adjust its holdings accordingly. The key question for index fund investors is whether delisting leads to a material impact on their overall investment performance.

Index Rebalancing: The Silent Impact

Index funds are passive by nature, designed to mirror the composition of an index. When a stock is delisted from an index, the fund automatically removes it and reallocates the capital into other constituents. This sounds simple enough, but it has a range of implications.

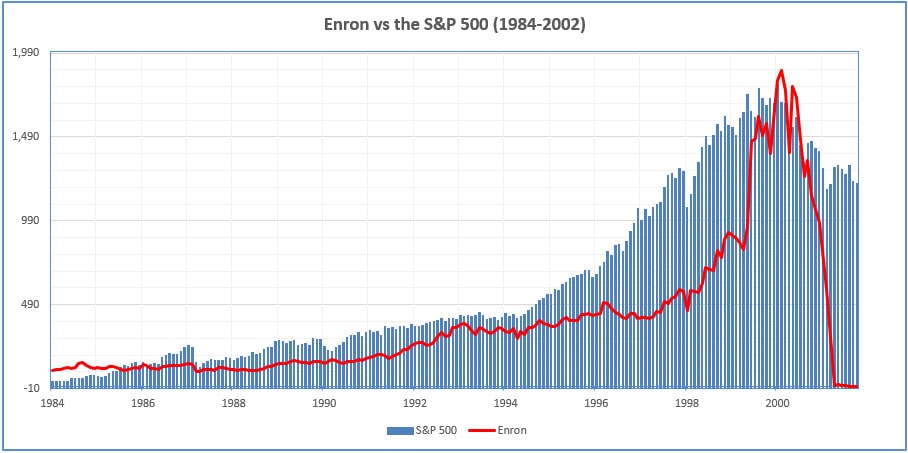

Example 1: The Fall of Enron Enron’s delisting in 2001 is a classic example. The company, once a darling of Wall Street, was a major constituent in the S&P 500. When its accounting fraud was uncovered and the stock price collapsed, index funds holding Enron suffered immediate losses.

Exhibit 1 (Source: Factset) Investors cannot invest directly in an index.

Timing and Liquidity Challenges

When a stock is delisted due to bankruptcy or failure to meet listing requirements, the process isn’t instantaneous. This creates a liquidity window, during which time the stock trades in the over-the-counter (OTC) markets, albeit at a lower price. Index funds generally avoid holding OTC stocks, so fund managers typically sell their position before the delisting takes effect. This is simple supply and demand – sellers outnumber buyers and the price falls which often means selling at a significant loss.

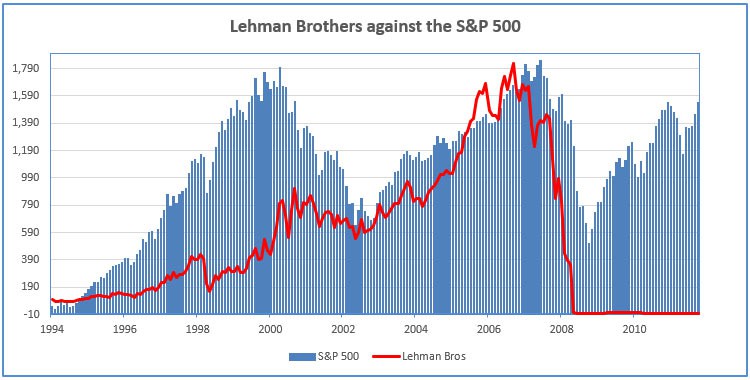

Example 2: Lehman Brothers During the 2008 financial crisis, Lehman Brothers’ collapse and subsequent delisting from the NYSE caused severe disruption. For index funds, the stock’s value plummeted, leading to massive sell-offs at the worst possible moment, effectively locking in those losses for investors in the S&P 500 index funds and other indices.

Exhibit 2 (Source: Factset) Investors cannot invest directly in an index.

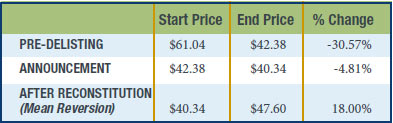

Example 3: AutoNation was removed from the S&P 500 index in 2017 due to the company’s declining market capitalization and performance relative to other firms in the index. The S&P 500 is composed of the 500 largest U.S. publicly traded companies and membership is primarily based on market value. Companies that see their market cap shrink below a certain threshold relative to others may be removed to maintain the index’s representation of the largest U.S. firms. Despite being a well-known auto retailing brand, these challenges and a declining market cap relative to peers resulted in AutoNation’s deletion from the S&P 500 in 2017. This removal signaled a rough patch for the company, which faced pressure to evolve in a rapidly changing market environment.

Exhibit 3 (Source: Factset)

As you can see prior to the reconstitution announcement to be delisted, AutoNation went from $61.04 to $42.38, suffering a loss of 30.57%. At announcement to end of grace period the stock further declined from $42.38 to $40.34. After reconstitution and deletion, the stock went up from $40.34 to $47.60

A. Pre-Deletion:

Exhibit 4 (Source: Factset)

B. Announcement of Effective Date:

Exhibit 5 (Source: Factset)

C. Reversion to the Mean:

Exhibit 6 (Source: Factset) All investments involve risk, including the possible loss of principal. Past performance is no indication of future performance.

Small-Cap and Micro-Cap Delistings

Delistings can be particularly problematic in small-cap and micro-cap indices, where companies are more prone to volatility, financial distress, and regulatory delistings. For investors in funds tracking indices like the Russell 2000, the risk of delisting is higher because smaller companies are more vulnerable to market fluctuations and financial instability.

Example 3: RadioShack RadioShack’s delisting in 2015 is an example from the small-cap world. At the time of its bankruptcy and subsequent delisting, RadioShack was a component of the Russell 2000 Index. Index funds tracking the Russell 2000 had to sell their shares, resulting in realized losses for investors.

Effects on Index Performance

The most direct impact of delisting is a reduction in overall index performance. While major indices like the S&P 500 are designed to remove underperforming stocks and replace them with higher-performing ones, the timing of these adjustments can be problematic. Delisted companies are often removed only after their stock has significantly depreciated, which means index funds are forced to sell low.

The Role of Market Cap Weighting

Most index funds are market-cap weighted, meaning that larger companies represent a bigger proportion of the index. Therefore, delisting a large-cap stock has a greater effect on performance than delisting a small-cap stock.

How to Mitigate the Impact of Delistings

Investors can take several steps to mitigate the negative effects of delistings:

- Diversify Across Asset Classes: Avoid over-concentration in any one index by investing across asset classes, such as bonds, real estate, or international markets. Diversification can reduce the impact of a single company’s failure. Note that diversification does not ensure a profit or protect against a decline in a down market.

- direct ownership (vs pooled ownership): One of the main advantages of direct ownership is the ability of the fund manager to choose stocks of stable companies with quality earnings. This level of control allows investors to build a portfolio of stocks that are less likely to be delisted. In contrast, pooled investments like mutual funds and ETFs offer limited control over individual securities.

- Focus on Quality Stocks: Indexes that focus on high-quality companies with strong balance sheets (such as those that track the S&P 500 Quality Index) may offer some protection from delistings. Companies with robust fundamentals are less likely to be delisted.

Conclusion

For index fund investors, delistings represent a hidden risk that can negatively impact long-term returns. While index investing remains a powerful strategy for building wealth over time, understanding the nuances of events like delistings helps investors make more informed decisions. By diversifying holdings and considering alternative approaches, such as actively managed funds or quality-focused indices, investors can help safeguard against the sometimes unexpected effects of delistings.

In the end, delisting is just another part of the broader market landscape but serves as an important reminder that even passive investing requires vigilance.

Related Articles

What are Reconstitutions and Delistings?

Index Investing,

October 24, 2023

How do Delistings Affect the Performance of Pooled Index Funds?

Index Investing,

Top Index FAQs,

October 21, 2024

Why do Transparency and Control Matter?

Index Investing,

Investment Principles,

Top Index FAQs,

Top Investment Principles FAQs,

November 3, 2023