By Indexopedia Research Team | October 15, 2024 | In

More often than not, investors seek to achieve the highest investment returns yet seldom consider the risks associated with those returns. The tricky nature of returns is that the more risk you take on, the more potential there is for upside. All too often, investors look through an investment guide or prospectus that shows great historical returns, yet seldom do the investment guides or advertising brochures spend time reviewing the risks or what happens when the fund or investment goes down, and how long the recovery may take.

Clearly, greater results often come by accepting greater risk, but the challenge for investors is when they seek high returns without considering the pain of a down market and how long it may take before recovery. If one seeks high returns and invests, but then finds themself in a down market with a long recovery, the challenge becomes staying invested long enough to regain the loss and remain invested to bear fruit. The problem with chasing returns is that higher returns are often directly correlated with recent results. If recent results are high, then average annual returns are increased, which is what investors seek. The challenge is that the returns that look so promising are often due to sector rallies. Investors may say, “I want more results,” without realizing the returns are based on what has already happened.

What we tell investors is “if you can’t swallow the pill, you shouldn’t put it in your mouth.” In other words, if you can’t handle the risk, you shouldn’t invest. This is why every investor should consider not just the returns, but also the down markets and recovery periods.

Understanding the Risk-Return Tradeoff

At the heart of any successful investment strategy lies the risk-return tradeoff, a simple but powerful concept that acknowledges that higher returns come at the cost of higher risk. This tradeoff is most evident when constructing a portfolio of stocks and bonds. A portfolio heavily weighted in stocks–historically the higher-returning asset class–offers greater potential upside but is also more exposed to volatility. Conversely, a portfolio dominated by bonds will generally provide lower returns but with much less risk. The key for investors is determining their own appetite for risk and crafting a portfolio that reflects their individual goals and timelines.

Let’s break this down with a practical example: a portfolio with 80% bonds and 20% stocks is considered lower-risk because bonds, particularly government or high-quality corporate bonds, tend to offer more stability. Such a portfolio will likely produce consistent, if modest, returns over time, with minimal exposure to large market swings. On the flip side, a higher-risk portfolio–say 80% stocks and 20% bonds–has the potential for much higher returns, but it also exposes the investor to significant market downturns, where stocks can lose substantial value in a short period.

Let’s break this down with a practical example: a portfolio with 80% bonds and 20% stocks is considered lower-risk because bonds, particularly government or high-quality corporate bonds, tend to offer more stability. Such a portfolio will likely produce consistent, if modest, returns over time, with minimal exposure to large market swings. On the flip side, a higher-risk portfolio–say 80% stocks and 20% bonds–has the potential for much higher returns, but it also exposes the investor to significant market downturns, where stocks can lose substantial value in a short period.

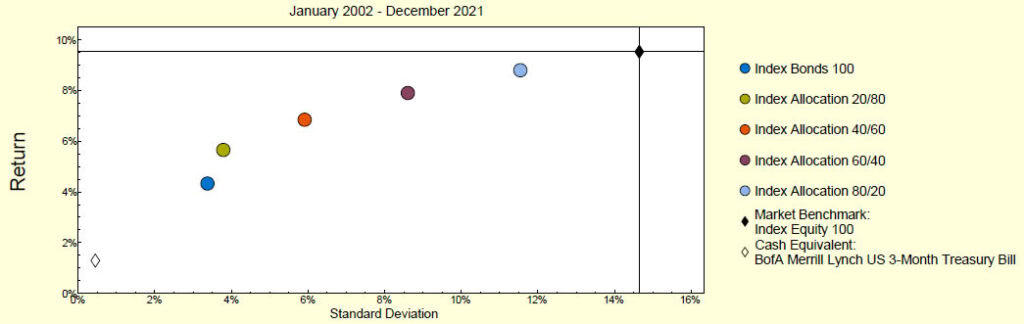

The graph below illustrates this concept. It examines the risk and return results of 5 theoretical portfolios, each constructed with varying allocations to stocks and bonds during the 20-year period from 2002 to 2021. The portfolio allocations range from 100% bonds to a portfolio with 20% bonds and 80% stocks. On the Y-axis is return, and on the X-axis is risk. Plotting the average risk and return of each portfolio along these axes reveals a “frontier” of results. You can clearly see that the all-bond portfolio has the lowest risk, but also comes with the lowest return. Conversely, the right-most point represents the 80/20 portfolio (80% stocks, 20% bonds). You can see that this portfolio delivered the strongest results but at a cost of significantly higher risk.

Exhibit 1: Source Zephyr

Historical Examples of the Risk-Return Tradeoff

To appreciate this tradeoff, we can look at historical performance during critical market events. Take the financial crisis of 2008. Investors with a heavy stock allocation, particularly those who were 100% invested in equities, saw their portfolios suffer as the S&P 500 lost 37% of its value that year. A portfolio balanced at 80% stocks and 20% bonds would have still suffered a significant loss but would have been cushioned somewhat by the relative stability of bonds.

In contrast, those with a more conservative portfolio, such as one with 80% bonds and 20% stocks, experienced far smaller losses. For example, the U.S. Treasury bond market had a positive return in 2008, serving as a buffer during the stock market collapse. Investors in these low-risk portfolios were able to avoid the worst of the downturn while still maintaining a small exposure to equities, which allowed them to capture some of the recovery when the market began to rebound in 2009.

Stocks for Growth, Bonds for Stability

The logic behind a balanced portfolio is straightforward: stocks are generally used to fuel growth, while bonds are employed to provide stability. Over time, stocks have consistently outperformed bonds, but their higher returns come with greater short-term volatility. For example, between 1980 and 2020, the S&P 500 delivered an average annual return of around 10%, while U.S. Treasury bonds returned roughly 5% per year. While stocks more than doubled the return of bonds, that performance came with significant fluctuations, including bear markets like the Dot-Com bust in the early 2000’s and the 2008 financial crisis.

A low-risk portfolio with 80% bonds and 20% stocks aims to capture some of that long-term growth potential of equities while prioritizing capital preservation. Bonds, especially high quality corporate bonds, provide steady income through interest payments and are much less likely to experience the wild swings common in the stock market.

In contrast, a high-risk portfolio with 80% stocks and 20% bonds maximizes the potential for long-term capital appreciation but requires the investor to be comfortable with the possibility of substantial short-term losses. This portfolio is best suited for younger investors or those with a longer investment horizon, as they have time to recover from any downturns.

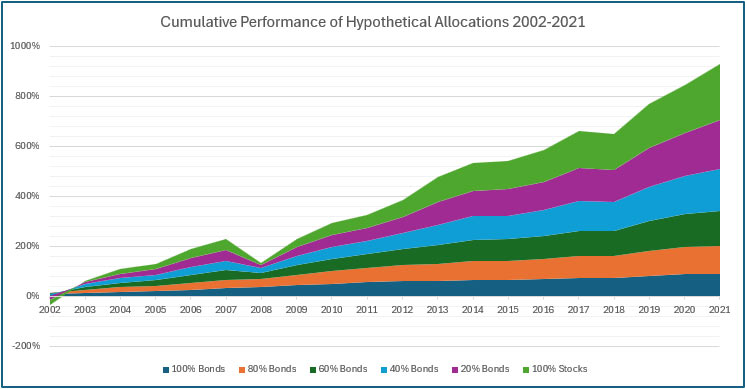

The graph below (Exhibit 2) illustrates how, over time, the higher-risk portfolios outperformed the lower-risk portfolios:

Exhibit 2 (Source: Zephyr)

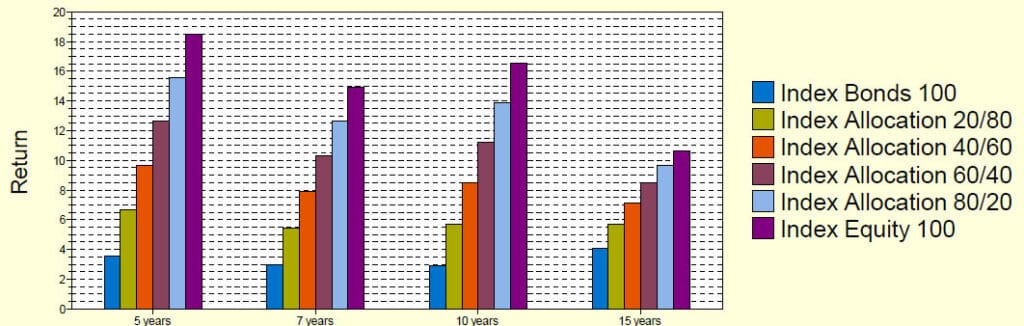

And in Exhibit 3, the average return comparison clearly demonstrates the superior results obtained from the riskier portfolio allocations:

Exhibit 3 (Source: Zephyr)

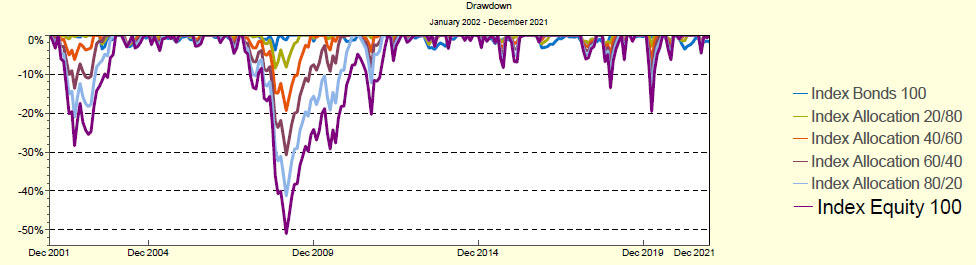

Superior returns generally come at a price, however. During down markets, the time to recovery is typically longer for the riskier portfolios. The graph below (Exhibit 4) demonstrates the drawdown experienced by each portfolio allocation. The all-equity portfolio, for example, suffered the worst drawdown – relative to the other portfolios. It also took the longest time to recover. Remember-there’s no such thing as a free lunch!

Exhibit 4 (Source: Zephyr)

The Power of Rebalancing

One of the key strategies to managing the risk-return tradeoff in a portfolio is regular rebalancing. Over time, as the stock and bond portions of the portfolio grow or shrink due to market fluctuations, the actual percentages of each asset class can drift from their original target allocation. For instance, if stocks outperform bonds over a given period, an 80% stock/20% bond portfolio might grow to 85% stocks and 15% bonds.

This drift increases exposure to risk, so it’s important to periodically rebalance the portfolio–selling off some of the overperforming stocks and buying bonds to bring the allocation back in line with the original target. Rebalancing ensures that you’re not unintentionally taking on more risk than you’re comfortable with, and it also helps to lock in gains from stocks during bull markets while buying bonds when their prices are lower.

Diversification: A Crucial Component

Diversification, which does not ensure a profit or protect against a decline in a down market, is another essential strategy for managing the risk-return tradeoff within a portfolio. Simply holding a mix of stocks and bonds is helpful, but diversifying within each asset class can further reduce risk. For instance, within the stock portion of the portfolio, you might diversify across different sectors, geographies, and company sizes. A portfolio with 80% stocks doesn’t have to mean 80% in U.S. tech companies–it could also include international stocks, emerging markets, or small-cap companies, each of which carries its own risk profile.

Similarly, within the bond portion of the portfolio, you could diversify between government bonds, corporate bonds, and even municipal bonds, depending on your income needs and tax considerations. While all bonds offer more stability than stocks, some categories, like high-yield or “junk” bonds, offer higher returns but come with greater credit risk.

Conclusion: No Free Lunch, But Smart Choices Can Help

Ultimately, the risk-return tradeoff is a fundamental principle that every investor must navigate. There’s no free lunch when it comes to investing–if you want to attempt to achieve superior returns, you must be willing to take more risk. However, the key is finding a balance that aligns with your financial goals and risk tolerance. For conservative investors, a portfolio weighted heavily toward bonds might be appropriate, while more aggressive investors might lean more toward stocks to capture greater long-term growth potentially.

By diversifying, rebalancing regularly, and understanding how risk and return work together, you can build a portfolio that not only meets your investment objectives but also gives you the confidence to weather whatever the markets may bring. Whether you choose an 80% bond, 20% stock portfolio or the reverse, it’s about understanding the tradeoffs and making informed decisions, knowing that no strategy is without risk, but that a well-managed portfolio can potentially mitigate those risks while providing the opportunity for meaningful returns over time.

Related Articles

The Power of Diversification: How Different Asset Classes Complement Each Other in a Balanced Portfolio

Behavior,

Index Sectors,

Investment Principles,

Markets,

Portfolio Considerations,

September 17, 2024

What is the “Perfect” Asset Allocation?

Investment Principles,

Portfolio Considerations,

January 8, 2025

The Importance of Rebalancing a Portfolio

Investment Principles,

Portfolio Considerations,

Top Investment Principles FAQs,

August 12, 2024