Most investors assume that IRAs and nonprofits don’t pay federal taxes — and under normal circumstances, they’re right. These vehicles are generally intended to be tax-exempt, allowing assets to grow or serve their missions without interference from the IRS.

But not all income qualifies for that privileged treatment.

One such example is Unrelated Business Taxable Income (UBTI), a lesser-known exception that can trigger surprise tax bills for unsuspecting investors. Whether it’s income from a leveraged real estate deal or a private equity investment inside a self-directed IRA, UBTI can complicate an otherwise tax-advantaged strategy.

Here’s what investors need to know about how UBTI works, what can trigger it, and how to manage it effectively.

What Is UBTI?

UBTI refers to income earned by a tax-exempt entity (e.g., IRA, 401(k), or nonprofit) from a business activity that’s unrelated to its core mission or purpose.

Alas, tax-exempt doesn’t mean tax-immune. While most forms of passive income (like dividends, interest, and capital gains) retain their tax-advantaged treatment inside IRAs or nonprofits, certain types of income do not.

UBTI can arise when a tax-exempt account engages — directly or indirectly — in an active trade or business. For example, a nonprofit running a side business unrelated to its mission (like a museum operating a for-profit cafe). To the IRS, these types of earnings don’t align with the purpose of a tax-exempt entity, and therefore, they’re subject to tax.

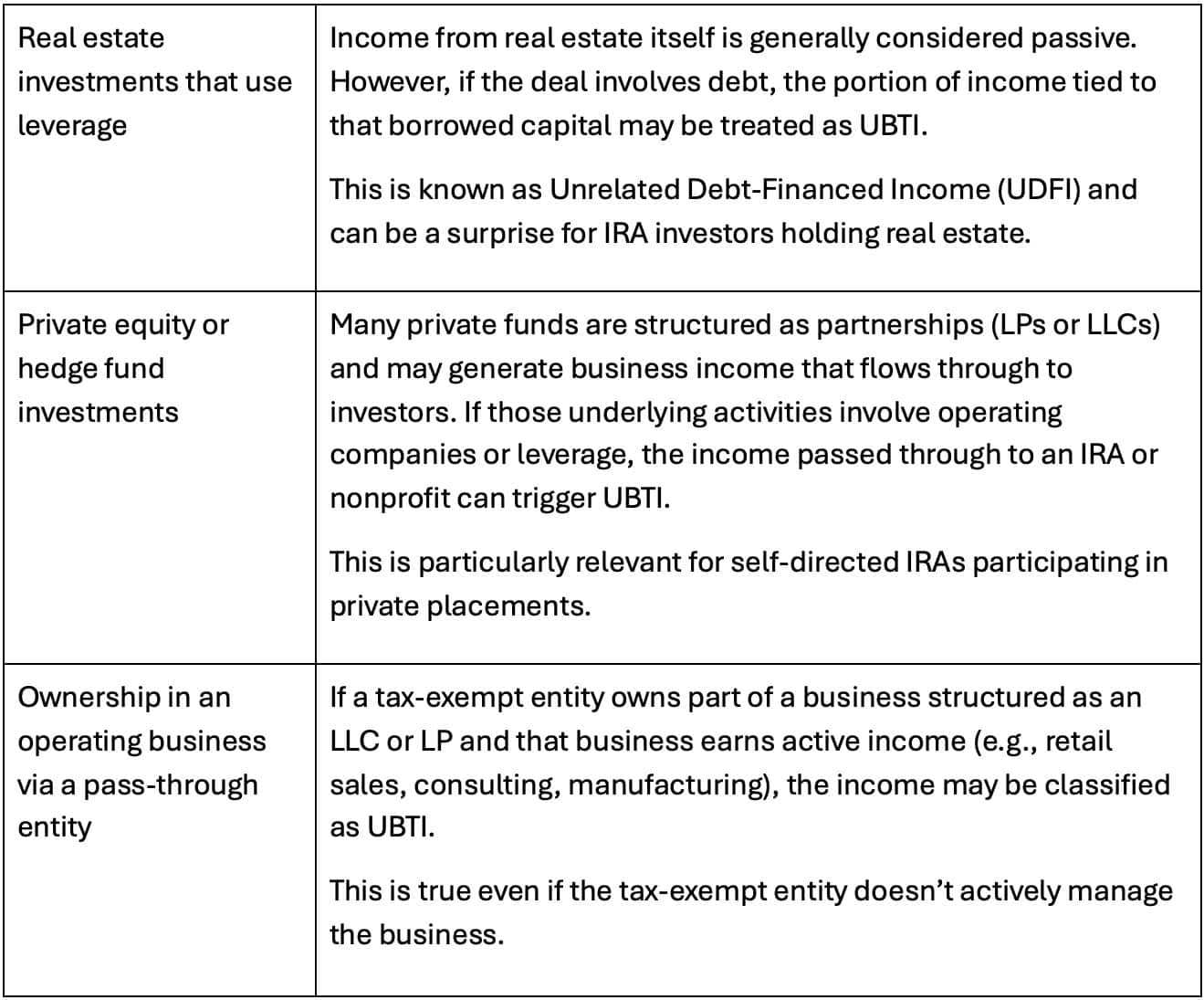

Common Examples of UBTI

Note, UBTI doesn’t prohibit alternative investments, but it does complicate them. If you’re investing through a self-directed IRA, it’s essential to review how the investment is structured, whether the entity uses leverage, and if the sponsor expects any UBTI exposure (usually disclosed on a Schedule K-1).

For example, energy and natural resource companies are often structured as master limited partnerships (MLPs), a type of publicly traded partnership that passes through income to investors. Let’s say an IRA holds an interest in XYZ Midstream Partners, an MLP that distributes propane and refined fuels. Because XYZ operates an active energy business, the income passed through to the IRA — as reported on Schedule K-1 — may be considered UBTI.

How UBTI Works in Practice

Tax-exempt entities aren’t taxed on all UBTI, only when it exceeds a certain threshold. For IRAs, 401(k)s, and nonprofits, the IRS allows up to $1,000 of UBTI per year without triggering a tax liability.

Once UBTI crosses that line, however, it’s subject to a separate tax (with a confusingly similar name): the Unrelated Business Income Tax (UBIT).

For IRAs and other tax-deferred accounts:

The IRA custodian is usually responsible for preparing and submitting IRS Form 990-T, which calculates the tax owed based on the account’s share of UBTI. Not all custodians offer support for UBIT filings though, which is a key consideration when investing through a self-directed IRA.

For nonprofits and other tax-exempt organizations:

UBIT is also reported on Form 990-T, and the organization pays the tax directly. Depending on the size of the UBTI and the frequency of exposure, nonprofits may also be required to make estimated quarterly payments.

While the tax rate varies depending on the entity type and income level, the presence of UBTI can chip away at the advantages of these accounts, so it’s important to evaluate exposure before investing.

Can UBTI Be Avoided or Mitigated?

Fortunately, there are several ways investors can reduce or avoid UBTI exposure while still accessing certain types of alternative assets.

1. Use of Blocker Corporations

To help shield tax-exempt investors from UBTI, many investment funds structure their offerings using what’s known as a blocker corporation: normally a C Corporation that sits between the fund and its investors.

Why does this matter? Because a C Corporation is taxed at the entity level — currently at a flat 21% corporate tax rate — while pass-through entities (like LLCs or LPs) push income directly to investors, which for tax-exempt accounts can result in a potential UBTI tax rate of up to 37%.

By interposing a C Corporation, the income is taxed once at the corporate level but doesn’t flow through as UBTI. That makes it a useful workaround for IRAs and nonprofits trying to access private investments without triggering unexpected tax liabilities.

Blockers are primarily why many investors have never heard of UBTI before. Publicly traded stocks are mostly structured as C Corporations, so UBTI wouldn’t be a concern.

2. Choose UBTI-Friendly Investments

Certain structures and asset classes are less likely to generate UBTI, namely funds that avoid operating businesses and leverage or funds that only distribute passive income (interest, dividends, capital gains, royalties, rent).

Always review offering documents, fund FAQs, and prior-year K-1s to gain insight into expected UBTI exposure.

3. Partner with the Right IRA Custodian

If you’re investing through a self-directed IRA, make sure your custodian:

- Supports Form 990-T filings and UBIT-related administration

- Communicates clearly about reporting deadlines and tax obligations

- Can help you track cumulative UBTI exposure across multiple investments

FAQs About UBTI

If an investment has the potential to incur taxes, why include it in an IRA?

In many cases, the after-tax benefits still outweigh the drawbacks, especially when exposure to UBTI is minimal or intermittent. A private real estate deal or MLP might generate some UBTI, but also deliver strong long-term appreciation or consistent cash flow.

How can I estimate my IRA’s UBTI tax liability?

UBTI is typically in box 20 with code “V” of a Schedule K-1, which are issued annually by the partnership or fund.

If UBTI exceeds $1,000, your custodian (assuming they support UBIT filings) will typically file IRS Form 990-T on behalf of the IRA and remit payment. The tax is applied at trust tax rates, which are more compressed than individual brackets — meaning they hit the highest tax rates at lower income levels, so the liability can add up quickly.

What happens if an IRA holds two or more investments that generate UBTI?

UBTI is aggregated at the account level, not on an investment-by-investment basis. So, if your IRA earns $700 of UBTI from one partnership and $600 from another, your total UBTI is $1,300, exceeding the exemption and triggering UBIT.

Related Articles

Who Invented the first index fund?

Index Investing,

Top Index FAQs,

Types of Indexes,

October 21, 2024

Donate From Your IRA to Reduce Taxes

Index Investing,

Personal Finance,

Tax,

September 19, 2024

Tax Efficiency: Incorporating Qualified Opportunity Zones and 1031 Exchanges into an Affluent Investor’s Portfolio

Personal Finance,

March 18, 2025