For families looking to fund education costs in a tax-efficient manner, 529 college savings plans remain one of the most powerful tools available. While each state sponsors its own plan and details vary widely, the core concept is consistent. A 529 plan is a tax-advantaged account that allows families to invest money for qualified education expenses, such as college tuition, fees, and in many cases K–12 tuition.

Because 529 plans are run at the state level, investors should understand not only the federal rules but also the specific features of the plan they are considering. Below we review the main attributes of 529 plans and explain what they mean for investors.

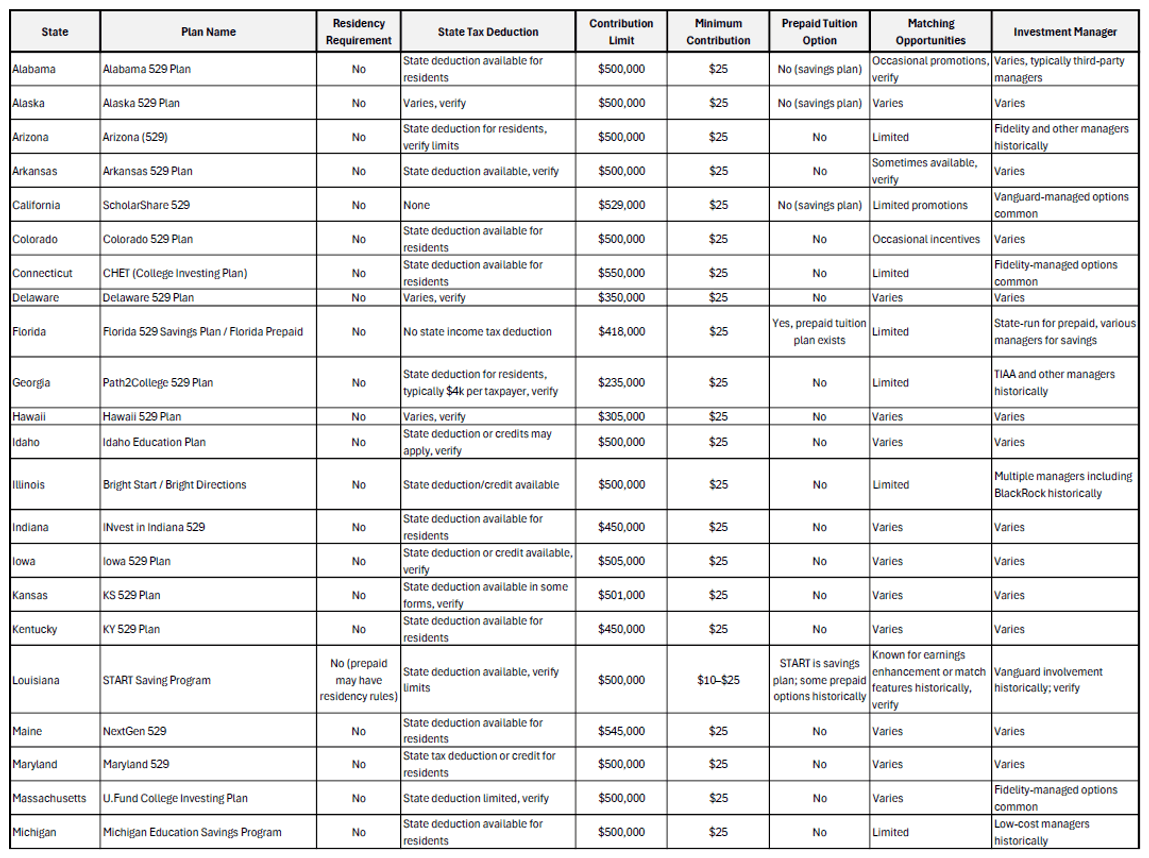

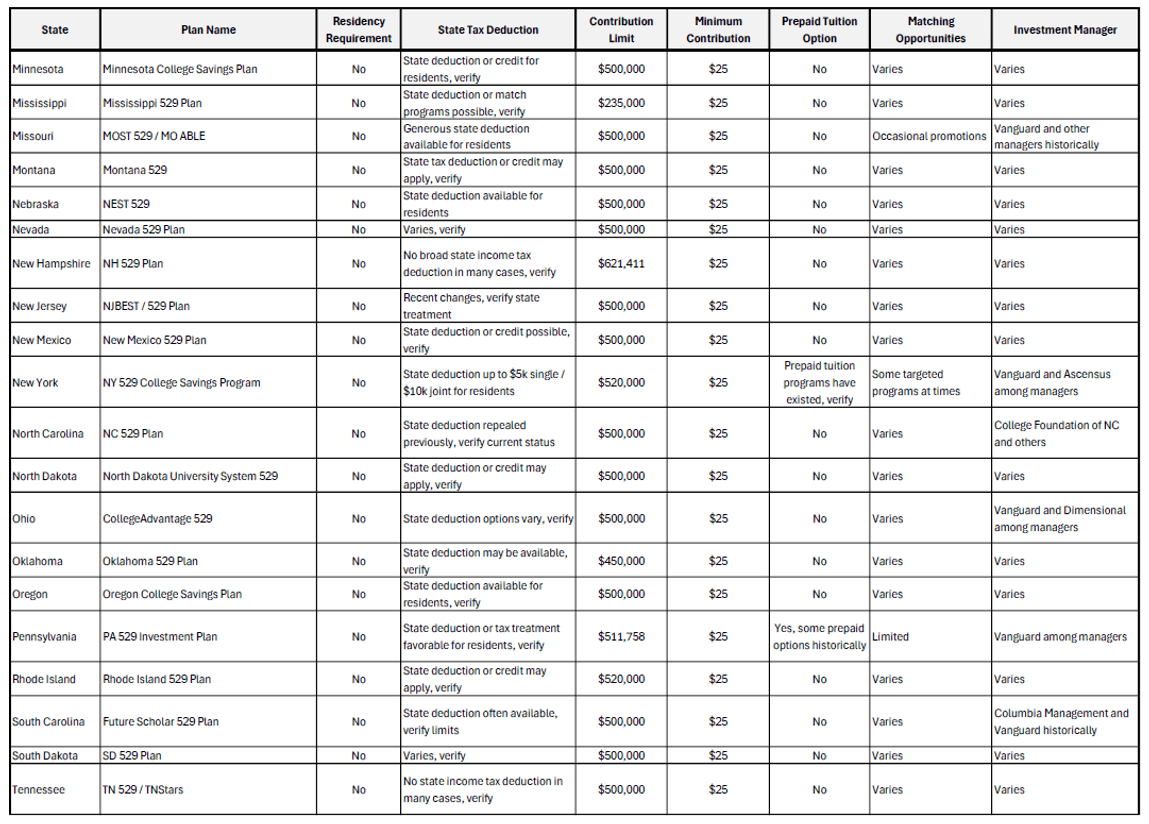

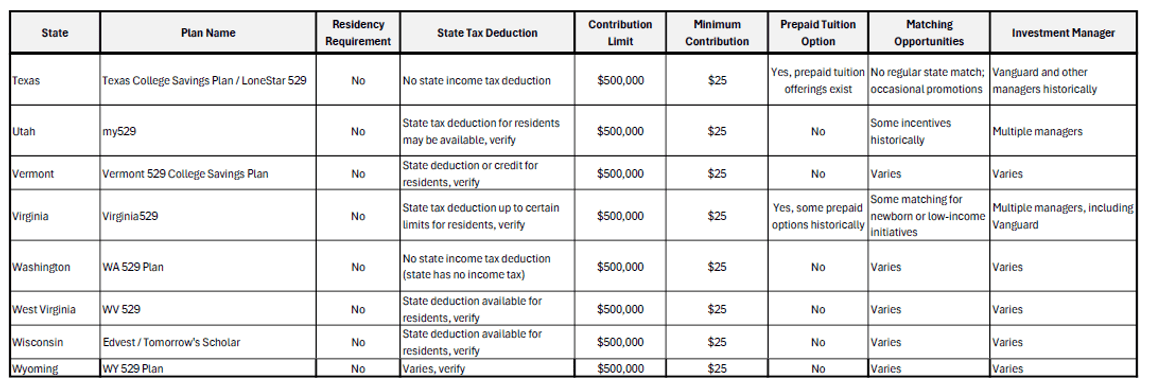

Key Attributes of 529 Plans

Fees

Every 529 plan charges administrative and investment management fees. These can range from very low (often under 0.25% annually for passively managed portfolios) to much higher if using actively managed funds or advisor-sold plans. Fees directly impact returns, so understanding the cost structure is essential.

State Tax Deduction or Credit

Many states offer residents a state income tax deduction or credit for contributions. For example, New York offers up to $5,000 for individuals and $10,000 for joint filers, while Georgia offers $4,000 per taxpayer per year. Some states, such as California and North Carolina, provide no deduction at all.

Contribution Limits

Although contributions are made with after-tax dollars, growth is tax-deferred and withdrawals for qualified expenses are tax-free. Most states set very high lifetime contribution limits, often in the $500,000 range per beneficiary. This makes 529 plans viable not just for college but also for advanced degrees.

Minimum Contributions

Plans typically require a modest minimum to open, usually between $25 and $50. Automatic contribution programs allow families to save regularly with ease.

Investment Options

Most plans offer both age-based portfolios, which gradually become more conservative as the beneficiary nears college age, and static portfolios, which allow investors to select a fixed asset allocation. Some plans also offer guaranteed or principal-protected options.

Investment Managers

States partner with asset managers such as American Funds (Capital Group), Vanguard, Fidelity, TIAA, and BlackRock, etc to manage investment portfolios. Manager choice influences cost, performance, and breadth of options.

Prepaid Tuition Options

A handful of states, including Florida and some universities within Texas, offer prepaid tuition plans where families lock in today’s tuition rates for future use. These differ from 529 savings plans and have unique risks and restrictions.

K-12 Tuition Use

Federal law allows families to use up to $10,000 per year for K-12 tuition from a 529 plan. However, state tax treatment varies. In some states, withdrawals for K-12 may trigger a recapture of deductions.

Residency Requirements

Anyone can invest in any state’s 529 plan, but only residents of the sponsoring state typically qualify for state income tax deductions or credits. Nonresidents may choose a plan based on fees, investment lineup, or performance.

Matching Opportunities

Some states offer contribution matching programs or scholarships tied to 529 savings. These tend to be income-limited but can provide meaningful boosts for qualifying families.

Gifting Tools

529 plans make it easy for extended family and friends to contribute. Many programs include online gifting platforms and tools for milestone contributions, which can help build balances over time.

Notable State Highlights

- New York: Offers a well-regarded plan with both static and age-based options. Residents benefit from state tax deductions.

- California: Provides no state tax deduction, but the ScholarShare plan is known for low costs and strong investment choices managed by Vanguard.

- Michigan: Offers both strong tax deductions and highly rated investment options.

- Colorado: Allows residents to deduct the full amount of contributions from state taxable income, one of the most generous benefits.

- Georgia: Provides a $4,000 deduction per taxpayer each year, though its overall contribution cap is somewhat lower than in many states.

- Louisiana: Offers a unique feature called the Earnings Enhancement, a state match on contributions that can boost returns for residents. This is one of the most investor-friendly state benefits in the country.

- Texas: Does not have a state income tax, so there is no state-level tax deduction, but Texas offers a prepaid tuition plan in addition to savings plans. This allows families to lock in tuition rates at public universities, which can be attractive for residents.

Which States Stand Out?

- Colorado and New Mexico stand out for their very broad state tax deductions.

- Louisiana is unique in offering an earnings enhancement, effectively a state match on contributions.

- Texas is notable for its prepaid tuition option despite not having an income tax benefit.

- California offers no deduction, but its low-cost structure and flexibility make it appealing even to nonresidents.

Why 529 Plans Matter for Affluent Investors

Even high-net-worth families benefit from the combination of tax-free growth, high contribution limits, and estate planning advantages of 529 plans. Contributions are considered completed gifts for tax purposes, but investors can “front-load” up to five years’ worth of contributions without triggering gift tax, which is a powerful wealth transfer tool.

The ability to control the account while shifting assets out of the taxable estate, combined with tax-free growth for education, makes 529 plans highly attractive for affluent families.

Final Thoughts

529 plans are versatile, tax-advantaged tools that can be tailored to fit many families’ goals. Because the specifics vary by state, investors should carefully evaluate fees, tax benefits, and investment options before committing. For families with significant wealth, these plans not only ease the burden of education costs but also serve as an effective estate planning and gifting strategy.

Summary of 529 Plans

Related Articles

Surviving a Market Correction: What Every Investor Needs to Know

Behavior,

Investment Principles,

Markets,

Top Markets FAQs,

August 12, 2024

Costs and Benefits of rolling a 529 Plan to a Roth IRA

Financial Planning,

Personal Finance,

Tax,

August 6, 2024

What Happens to Unused 529 Funds?

Personal Finance,

Tax,

August 12, 2024