There’s an undeniable appeal to “set it and forget it.” That’s the explicit promise of target-date funds (TDFs): choose the year closest to your expected retirement, and your investment mix automatically adjusts as you age.

It’s a simple, convenient solution, especially for those who don’t want to worry about market timing or portfolio rebalancing.

But convenience comes with trade-offs. TDFs are designed for the average investor, not you. Their simplicity can mask important nuances around risk tolerance, retirement income needs, and outside assets. The one-size-fits-all approach may lead to a portfolio that’s misaligned with retirement goals at the very stage when alignment is of the utmost importance.

So, it’s important to understand what a TDF can (and can’t) do for your retirement plan.

How Target-Date Funds Work

You select a fund based on your expected retirement year (for instance, a 2045 Fund) and it handles the rest. The fund’s managers determine how much to allocate to stocks, bonds, and other assets based on how far you are from that date.

Early in your career, the mix is usually aggressive, tilted heavily toward stocks to capture growth. As the target date approaches, the fund automatically shifts toward bonds and cash equivalents to reduce volatility.

This gradual adjustment is known as the “glide path,” and it may continue past the specified target date. The exact duration varies by provider, which means two funds with the same target year can follow very different post-retirement strategies.

Index-based TDFs, which track market benchmarks instead of relying on active management, have become particularly popular in 401(k) plans. They’re low-cost, broadly diversified, and easy to understand, which is exactly why they’ve become the default investment option for millions of workplace retirement accounts.

Why They’re So Popular

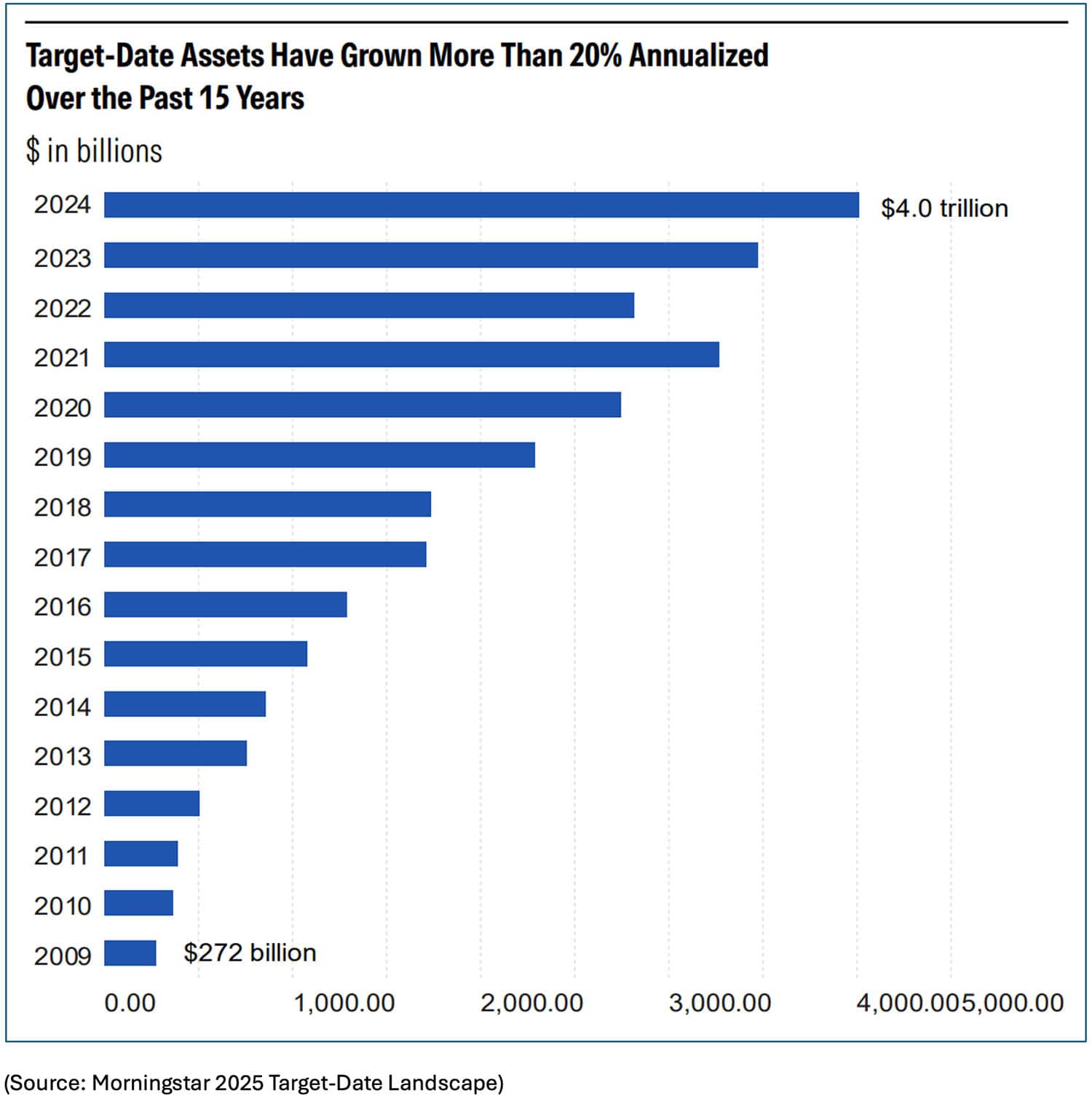

TDFs have grown from a niche experiment into a retirement investing staple. Assets in target-date strategies surpassed $4 trillion in 2024 — enough to make the category, if it were a country, the fourth-largest economy in the world. Over the past 15 years, assets have climbed at a 20% annualized rate, fueled by both market growth and steady inflows from workplace retirement plans.

That said, while TDFs do offer the convenient benefit of built-in diversification and automatic rebalancing, much of their colossal growth can be attributed to a regulatory change. In 2007, the US Department of Labor approved TDFs as a qualified default investment alternative (QDIA) for 401(k) plans. That single rule paved the way for these funds to dominate the industry.

In other words, new plan participants who didn’t choose their own investments were defaulted into them.

Today, most retirement savers own one — in many cases, without realizing it. According to Vanguard’s How America Saves report, 84% of 401(k) participants use TDFs, and 71% of those investors have their entire balance in a single fund. Surveys also show that nearly half of plan participants don’t know what their investment options are, which would suggest that most TDF investors’ entire retirement portfolio is sitting in a fund they didn’t actively select.

Convenience, however, is not a substitute for personalization.

The Shortfalls of Target-Date Index Funds

For all their convenience, target-date funds are built on broad assumptions. They aim to serve a large audience with a single, formulaic approach — a strategy that works well in theory, but not always in practice.

One Size Doesn’t Fit All

Target-date funds assume that investors with the same retirement year share similar needs and risk tolerance. But two people saving for 2045 may have completely different financial situations — different incomes, account balances, outside investments, and comfort levels with volatility.

A single glide path can’t account for those differences. For one investor, a 2045 fund may feel overly aggressive. For another, it may be too conservative, leaving long-term growth on the table.

That’s because glide paths, the formula that dictates how the mix of stocks and bonds shifts over time, are built around generalizations. The fund doesn’t know whether you plan to retire early, work part-time in your 60s, or rely on other income sources.

In short, target-date funds don’t adapt to you. You adapt to them.

Glide Paths Aren’t Standardized

Even within the same target year, glide paths can differ dramatically between providers. Some may keep higher equity exposure near retirement; others could reduce stock allocations much sooner.

These differences can be substantial — 30 percentage points or more in equity exposure near the target date. That variation can translate to material differences in returns and volatility, particularly in the critical years leading into retirement when sequence of returns risk is highest.

Along the same lines, glide paths also vary in duration (i.e., how long they continue adjusting after the target date). Some funds end their glide path immediately once an investor reaches retirement, locking in a static allocation from that point forward. Others continue to gradually de-risk for years or even decades, with some extending until the investor is age 75, 80, or even 95.

Sequence of Returns Risk

Sequence of returns risk is the possibility that a market downturn early in retirement can have an outsized and lasting impact on portfolio longevity. If you’re forced to sell assets to fund living expenses while markets are down, those losses are locked in, leaving less capital to recover when markets rebound.

Target-date funds don’t account for this timing risk. Two retirees could invest in the exact same 2025 fund, but if one begins withdrawals during a bear market and the other during a bull market, their long-term outcomes could diverge sharply. The fund’s glide path continues shifting on schedule regardless of market conditions or each investor’s withdrawal needs.

That rigidity can be costly. While target-date funds reduce risk gradually as investors age, they aren’t making dynamic adjustments based on real-time volatility or changing income needs. For investors drawing from their accounts, that means the comfort of a “conservative” allocation may not protect against the financial impact of an unfortunately timed market downturn.

This risk isn’t unique to target-date funds, but their design can make it harder to manage. A personalized plan that coordinates withdrawals, cash reserves, and tax strategy offers far more flexibility.

The Importance of Personalization

The closer you get to retirement, the more your plan should reflect you — not a composite investor born in the same decade.

A personalized strategy considers factors that target-date funds simply can’t:

- Income needs and spending goals. How much and when you plan to withdraw determines how much risk your portfolio can afford.

- Outside assets and savings vehicles. A 401(k) is rarely your only account. Balancing taxable, Roth, and other investments can meaningfully affect after-tax outcomes.

- Risk tolerance and flexibility. Some investors can stomach more volatility or plan to keep working longer.

Tax and estate considerations. Withdrawal sequencing, charitable giving, and legacy planning all play a role that a preset glide path doesn’t account for.

Related Articles

Are Index Funds Tax Efficient?

Index Investing,

Top Index FAQs,

October 28, 2024

How do market cap index funds work?

Index Investing,

Top Index FAQs,

Types of Indexes,

October 24, 2023

Why is Income Important in Retirement?

Fixed Income,

Personal Finance,

Top Personal Finance FAQs,

Why to Buy & Where,

August 14, 2024