When headlines turn dark and geopolitical tensions erupt into open conflict, financial markets often react with immediate volatility. Prices swing sharply. Commentators warn of worst-case scenarios. Investors feel the deeply human pull toward safety. The instinct to “do something” -often to sell – can feel overwhelming.

Yet history tells a strikingly consistent story: markets have generally moved higher in the periods immediately after war breaks out. While the initial shock can rattle confidence, long-term returns have tended to reward patience rather than panic.

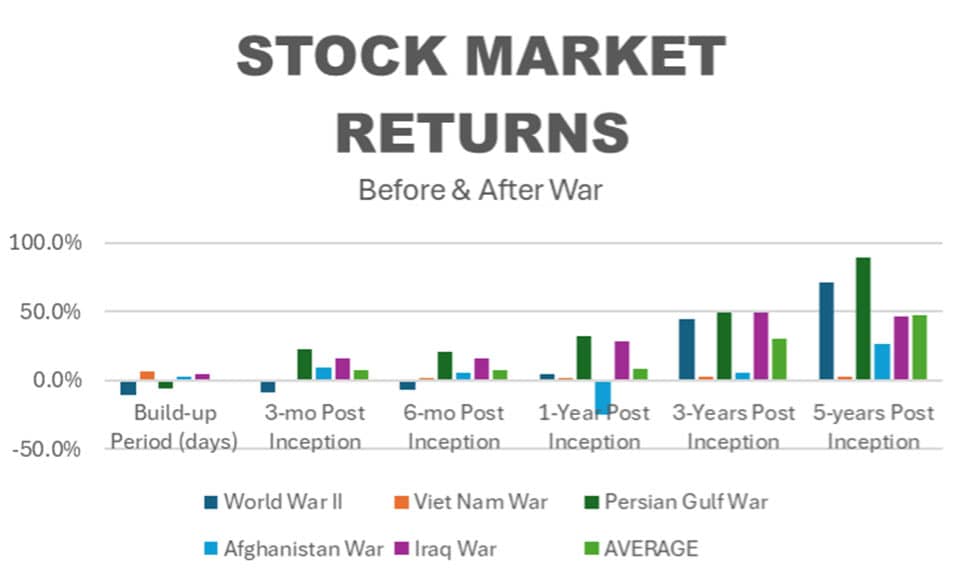

Most wars don’t start out of the clear blue sky. In the grand sweep of history, there are many geopolitical reasons that cause one nation to square-off against another. But, in retrospect, there are often moments that mark the build-up to war: Perhaps a leader is assassinated. A ship is sunk. A neighboring nation is invaded. Or new laws are passed. While arbitrary in nature, hindsight offers some clues to suggest the moment that urgency of war had begun. For instance, the US Congress passed the Lend-Lease Act on March 11, 1941 to provide aid to our allies who were already involved in World War II – about 8 months before Congress declared War on Japan. Likewise, Congress passed the Gulf of Tonkin Resolution on August 7, 1964 – about 7 months before our first deployment of combat troops to Viet Nam. And similar events took place prior to other conflicts. The point of this exercise is not to debate the exact moment war was inevitable, but rather to lend insight into market behaviors prior to the onset of war. As illustrated in the table below, markets have the poorest results during this build-up phase – when fear tends to sweep over markets.

The most challenging data point in the entire table is the 1-year Post Inception of the Afghanistan War. The War began shortly after the events of 9-11, but this ignores the bursting of the Tech Bubble, the onset of recession, the collapse of Enron, World-Com, and others in a wave of high-profile scandals, the ascendancy of China, skyrocketing commodity prices, etc. In other words, the economy and markets had a powerful array of antagonizing events that directly impacted earnings, liquidity and stock prices. But the economy eventually recovered and so did the markets.

Why?

First, markets are forward-looking. By the time a war officially begins, investors have often been pricing in rising tensions for months. The uncertainty that weighed on markets beforehand begins to resolve – not because war is positive, but because clarity replaces speculation. Markets prefer known risks over unknown ones. When the event finally occurs, the removal of uncertainty can itself stabilize sentiment.

Second, economic systems are remarkably adaptive. Businesses adjust supply chains, governments recalibrate fiscal policy, and central banks respond to shifting conditions. In many historical cases, wartime spending has stimulated industrial production, employment, and technological innovation, lifting overall spending. Moreover, governments can and do increase debt to finance these expenditures, and, not surprisingly, often increase monetary support for the economy as well, which tends to stimulate the flow of credit. And we are not just talking millions of dollars, but rather hundreds of billions of dollars and perhaps trillions. While war brings undeniable human and geopolitical costs, economic activity frequently proves more resilient than investors initially assume.

Consider the pattern: in numerous past conflicts, markets experienced a short-term drop near the onset of hostilities – sometimes days, sometimes weeks – followed by recovery and eventual gains over subsequent years. Investors who sold in the early days of fear often locked in losses and missed the rebound.

The real risk during wartime is not volatility. Volatility is normal. The real risk is abandoning a long-term plan at precisely the wrong moment.

Behavioral finance explains why this happens. Humans are wired for survival, not for portfolio optimization. Fear sharpens focus on immediate threats and amplifies worst-case thinking. Loss aversion – our tendency to feel losses more intensely than gains – makes temporary declines feel permanent. In uncertain times, cash feels safe, even if inflation quietly erodes its value.

But markets do not reward emotion. They reward discipline.

A diversified investor with a long-term horizon is not investing in a single headline, a single administration, or a single conflict. They are investing in global productivity, innovation, human ingenuity, and the compounding power of capital over decades. Wars have occurred throughout modern financial history – and yet equity markets, over long spans, have trended upward.

This does not mean every period is smooth. There will be volatility. There may be drawdowns. Some sectors may suffer while others benefit. Energy, defense, commodities, and infrastructure may move differently than technology or consumer sectors depending on the nature of the conflict. But broad markets have historically demonstrated resilience.

The cost of mis-timing the market can be severe. Missing just a handful of the strongest recovery days – which often occur amid peak fear – can dramatically reduce long-term returns. Investors who step aside waiting for “clarity” frequently re-enter only after prices have already recovered.

None of this suggests ignoring risk or abandoning prudent asset allocation. Portfolio alignment with time horizon, liquidity needs, and risk tolerance remains essential. But reacting impulsively to geopolitical shock rarely improves outcomes.

In moments of crisis, it can help to zoom out. Ask: Has human enterprise permanently stopped? Has innovation ceased? Has global commerce ended? History suggests the answer is no. Even in the aftermath of profound global conflicts, economies rebuild, industries evolve, and markets advance.

The disciplined investor acknowledges uncertainty without surrendering to it. They rebalance when appropriate. They maintain diversification. Most importantly, they stay invested.

War heightens emotion. Markets amplify it. But long-term wealth has typically accrued to those who resist the urge to flee at the sound of alarming headlines.

The next time geopolitical tension dominates the news cycle and markets tremble, remember: fear is temporary. Compounding is powerful. History favors patience.