Markets are living, breathing organisms. They pulse with opportunity and risk, shaped by investor psychology, innovation, and, at times, sheer irrationality. As an investor, understanding market history isn’t just an academic exercise – it’s essential for making better decisions today.

The Tulip Bubble: A Lesson in Speculation

The Dutch tulip bubble is often cited as the world’s first recorded speculative bubble. In the early 1600s, tulips became all the rage in the Netherlands, prized for their rarity and beauty. As demand soared, so did prices, and ordinary people jumped into the market. They weren’t just purchasing tulips for their gardens–they were treating them like today’s tech stocks, speculating that prices would keep climbing. Tulips were traded as contracts, often with no intention of actual delivery, not unlike the derivatives markets we see today.

At the height of this frenzy, a single tulip bulb could cost more than a house. But, as with all bubbles, reality eventually intervened. By 1637, tulip prices collapsed almost overnight. Investors who had speculated on further price gains were left with nothing but a fistful of worthless contracts. Sound familiar? Think of the dot-com crash centuries later, where companies with no profits and shaky business models were valued based purely on hype.

The South Sea Bubble: Government Intervention Gone Awry

Fast forward to the early 1700s and we encounter the South Sea Bubble, another famous episode of market mania. The South Sea Company was a British corporation that promised vast profits through trade with South America. The British government endorsed the company, and this endorsement stoked speculation.

Investors believed that the company would monopolize the riches of the New World, leading to a massive stock price surge. At its peak in 1720, the company’s stock price increased eightfold. But the South Sea Company had a fatal flaw: it wasn’t making money. The promise of future wealth turned out to be an illusion, and when investors finally realized this, the stock price collapsed. As fortunes were lost, the British government had to step in to mitigate the damage.

What’s crucial to remember here is that bubbles are often fueled by some element of truth–whether it’s the allure of foreign trade or the potential of new technology. But when expectations outpace reality, it can cause a crash that reverberates across the entire economy. Government involvement, as we saw in the South Sea Bubble, can sometimes add fuel to the fire rather than calm markets.

The Mississippi Bubble: A French Speculative Frenzy

While the South Sea Bubble was unfolding in Britain, France experienced its own financial meltdown with the Mississippi Bubble. In the early 1700s, John Law, a Scottish financier, convinced the French government to let him take control of the country’s financial system and establish the Mississippi Company, a trading venture in Louisiana. He promised immense wealth from the undeveloped territories, which fueled a speculative mania.

Investors flocked to buy shares in the company, causing its stock price to skyrocket. The French government printed more money to keep the frenzy going, leading to rampant inflation. Just like with the South Sea Bubble, the company’s perceived value was based more on imagination than reality. By 1720, the bubble burst, leading to economic chaos in France and devastating the finances of thousands of investors.

The Mississippi and South Sea Bubbles share a common theme: government involvement in speculative ventures. The lesson? Be cautious when governments promote investments based on unproven future potential. It’s a theme that reappears throughout market history.

The Railway Mania: Industrial Revolution Fever

As the 19th century progressed, the Industrial Revolution brought sweeping changes to economies around the world. One of the most transformative industries was railroads. In the mid-1800s, the promise of fast, efficient transportation ignited what became known as the Railway Mania in Britain.

Investors poured money into railway companies, believing that rail would revolutionize trade and travel. Many companies were created, some with legitimate plans and others that existed purely to capitalize on the speculative fever. By the late 1840s, railway stocks were grossly overvalued, and when the bubble burst, thousands of investors were wiped out.

The collapse of the Railway Mania is a perfect example of how investors can be swept up in the excitement of new technology. Even if the technology itself is sound, the investments based on overoptimistic projections can be dangerous. This may be a cautionary tale for modern investors tempted to value new technologies, such as electric vehicles, AI, or other emerging sectors, without considering the fundamentals.

The Panic of 1873: The First Global Financial Crisis

The Panic of 1873, often called the “Great Depression” before the 1930s, was one of the first truly global financial crises, marking the end of the post-Civil War boom in the United States and the collapse of the speculative railroad bubble. This crisis began in Europe, with the collapse of a major bank in Vienna, Austria, and quickly spread across the Atlantic to the U.S., where the overheated railroad industry was at its peak.

Overinvestment in railroads, combined with widespread speculation in related industries, led to a massive economic downturn. The stock market crashed, banks failed, and unemployment soared. The effects of the Panic of 1873 lasted for years, leading to economic stagnation and widespread hardship in both Europe and the U.S.

The lesson here? Even seemingly robust sectors such as railroads in the 19th century can collapse when too much speculative capital flows in without regard to long-term sustainability. When an industry becomes a one-way bet in the eyes of investors, that’s usually the time to get cautious.

The Panic of 1907: The Precursor to Modern Financial Regulation

Before the creation of the Federal Reserve, the U.S. economy was prone to sudden financial panics. One of the most famous occurred in 1907. This crisis was triggered by a failed attempt to corner the market on United Copper Company stock, but the underlying cause was more systemic: an over-leveraged banking system and speculative investments.

As panic spread, depositors rushed to withdraw their money, leading to widespread bank failures. The crisis only subsided when J.P. Morgan personally stepped in to shore up failing institutions, demonstrating a dangerous reliance on individual financial titans to stabilize the economy.

The Panic of 1907 highlighted the need for a central banking system to act as a lender of last resort during financial crises. The Federal Reserve was established in 1913 to prevent such panics from happening again, but it also serves as a reminder of how fragile the financial system can be when faced with unchecked speculation. Even today, we see echoes of the 1907 panic in debates about the balance between free markets and financial oversight.

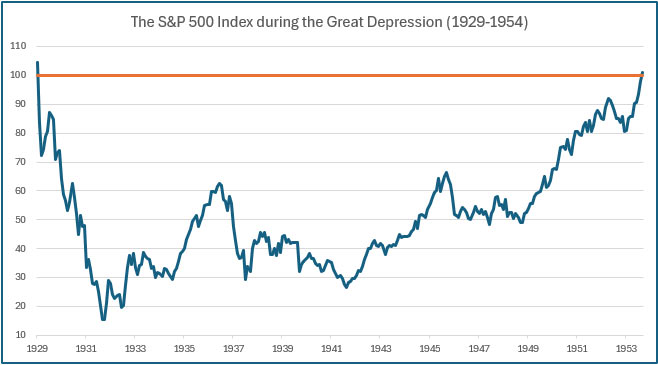

The Roaring Twenties and the Great Depression: Irrational Exuberance

The stock market in the 1920s was driven by the explosive growth of American industry, consumer goods, and financial innovation. The decade was one of prosperity for many, as investors eagerly piled into stocks. The introduction of buying on margin–borrowing money to purchase stock–allowed even more people to participate in the boom.

Speculation became rampant, with investors convinced that the stock market could only go up. Entire sectors, particularly in industries like automobiles and radio, saw meteoric rises in their stock prices, often with little regard to whether the companies could sustain such growth.

By 1929, the market had grown to unsustainable levels, and as we all know, it came crashing down on “Black Tuesday.” The Great Depression followed, wiping out vast amounts of wealth and leaving scars that lasted generations. The lesson here? Leverage and overconfidence can turn a boom into a bust with staggering speed.

The parallels to today’s markets are hard to ignore. Leverage and speculation are still rampant, especially with the advent of newer financial tools like options and derivatives. The Great Depression taught us that while markets can soar in times of prosperity, they can also fall hard, especially when inflated by speculative excess.

Exhibit 1 (Source: Factset)

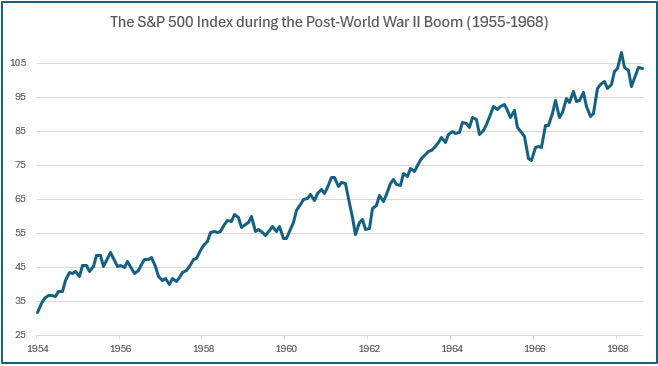

Post-World War II Boom: The Birth of Modern Markets

Following the Great Depression and World War II, the U.S. economy entered one of its longest periods of sustained growth. The 1950s and 1960s marked the rise of the American middle class, fueled by government programs such as the G.I. Bill and infrastructure development, which spurred consumer spending and industrial growth. The stock market, which had languished through the Depression years, recovered and soared during this era, driven by robust economic expansion and technological advancements in manufacturing, energy, and transportation.

In this period, companies like General Motors, IBM, and Coca-Cola became household names, representing the growing influence of corporate America. The birth of mutual funds during this time allowed retail investors to participate in the stock market like never before, diversifying their holdings with professional management. It was during this post-war boom that the concept of “buy and hold” gained traction among investors who were becoming more optimistic about long-term economic growth.

However, the market’s steady rise wouldn’t last forever. By the late 1960s and early 1970s, cracks in the post-war economic structure began to appear, setting the stage for the turbulent decade that followed.

Exhibit 2 (Source: Factset)

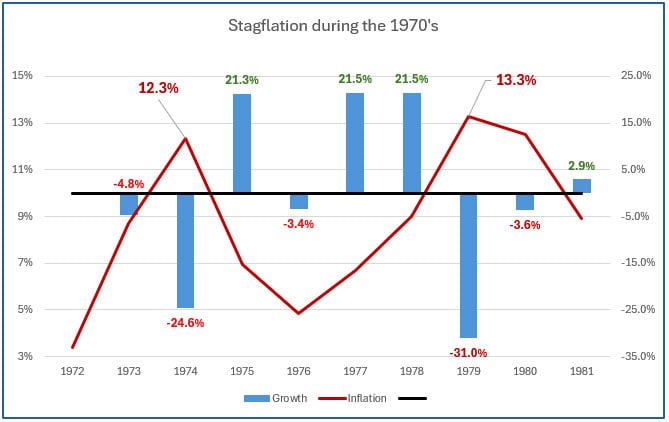

The 1970s: Stagflation and the Oil Crisis

The 1970s were a period of economic turbulence that tested the resilience of both investors and markets. This era is best remembered for the phenomenon of “stagflation,” a rare combination of stagnant economic growth and high inflation. The traditional economic wisdom of the time–that inflation and stock prices were inversely related–was turned on its head. Investors watched as stock prices languished in a period of slow growth, while inflation eroded purchasing power.

Adding fuel to the fire, the 1973 oil embargo imposed by the Organization of the Petroleum Exporting Countries (OPEC) quadrupled oil prices virtually overnight. This triggered an energy crisis in the West, leading to soaring fuel costs, long lines at gas stations, and deep concerns about the economic outlook.

Exhibit 3 (Source: GDP: FRED, St Louis Fed; CPI: InflationData.com)

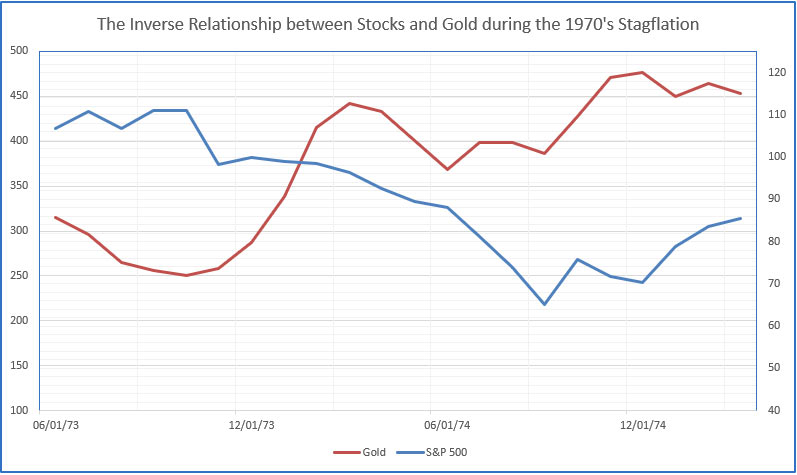

For investors, the 1970s were a sobering reminder that markets don’t always go up. The S&P 500 Index, which had risen steadily throughout the post-war period, stagnated during the decade, making it one of the least profitable times for stock market investment in modern history. Gold, however, became a star asset during this period, as investors sought a safe haven from inflation and currency devaluation. This reinforced the importance of diversification across asset classes, particularly during times of economic uncertainty.

Exhibit 4 (Source: Factset)

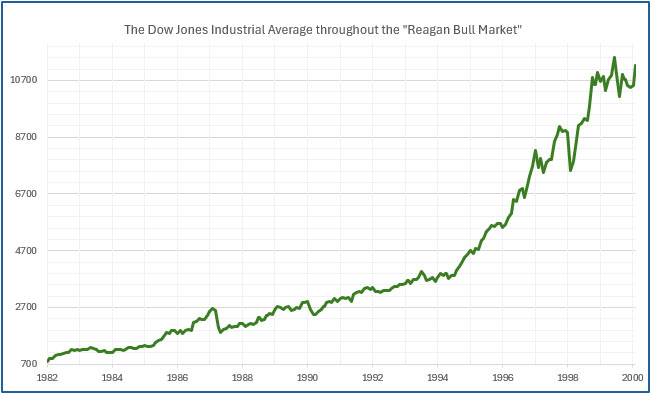

The Reagan Bull Market and the Rise of the Financial Industry

By the early 1980s, the economic landscape was primed for change. Inflation remained high, but a shift in Federal Reserve policy under Chairman Paul Volcker broke the back of inflation through aggressive interest rate hikes. While this initially caused a recession, it set the stage for one of the most powerful bull markets in history.

The election of Ronald Reagan in 1980 also marked a new era of pro-business policies, with significant tax cuts, deregulation, and an emphasis on free markets. Investors were buoyed by optimism, and the stock market responded in kind. From 1982 to 2000, the Dow Jones Industrial Average grew from under 800 points to over 11,000, a staggering increase that cemented the stock market as a primary driver of wealth creation for millions of Americans.

Exhibit 5 (Source: Factset)

During this period, the financial services industry expanded rapidly. Investment banks, mutual funds, and pension funds became household names, offering an ever-expanding menu of financial products designed to meet the growing demand from a public eager to invest in the market. The 401(k), introduced in 1978, revolutionized retirement savings, allowing employees to direct a portion of their wages into tax-deferred retirement accounts invested in stocks and bonds.

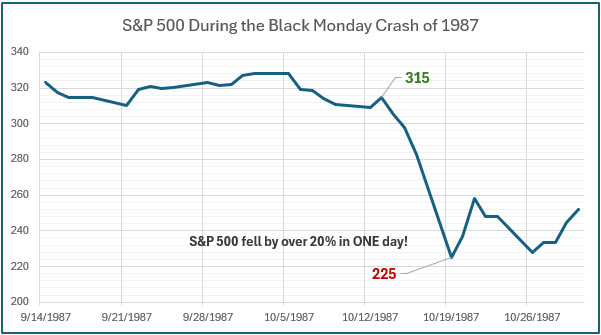

The 1987 Stock Market Crash: A Warning Shot

No bull market is without its hiccups, and on October 19, 1987, the stock market experienced one of the most dramatic single-day losses in history–what’s now referred to as “Black Monday.” The Dow plunged over 20% in one trading day, a drop that sent shockwaves through global financial markets.

Exhibit 6 (Source: Factset)

While the causes of Black Monday remain debated, it is widely believed that the advent of computerized trading and complex financial products exacerbated the market’s volatility. Despite the severity of the crash, the market quickly recovered and resumed its upward trajectory. But for many investors, Black Monday served as a stark reminder that even in times of exuberance, markets can turn on a dime.

More importantly, it demonstrated how financial innovation and technology–while beneficial in many respects–could also lead to unintended consequences, a theme that would emerge again during the dot-com bubble and the 2008 financial crisis.

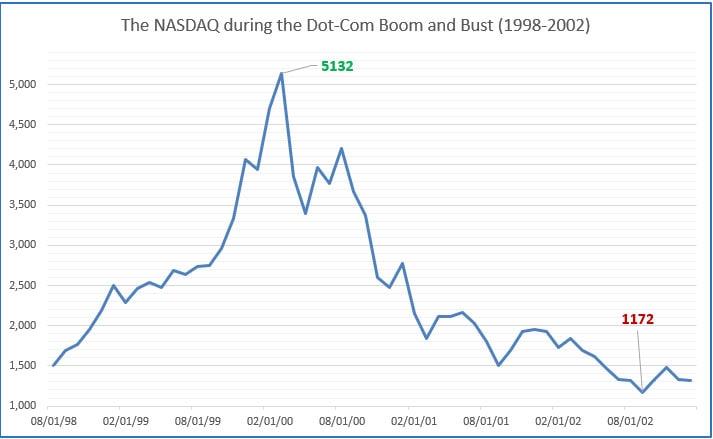

The Dot-Com Boom and Bust: Tech Fever Takes Hold

By the early 1990s, the U.S. economy had emerged from a mild recession, and the stock market was entering another growth phase. The rise of the internet sparked a new era of innovation and economic optimism, leading to the famous dot-com bubble. The internet promised to revolutionize everything from commerce to communication, and investors, flush with cash from a decade of economic growth, were eager to get in on the ground floor.

The rise of the internet sparked an investment frenzy that resembled the manias of centuries past. Companies that barely had a business plan or revenues were being valued at billions. Investors, convinced that the internet would revolutionize everything (which, to be fair, it did), ignored traditional valuation metrics.

Companies like Pets.com, Webvan, and many others went public with no clear path to profitability, but that didn’t stop investors from piling in. Just as tulips had once seemed like the path to wealth, internet stocks became the new ticket to riches. But as we saw with tulips and the South Sea Company, reality eventually catches up.

In 2000, the bubble burst. The NASDAQ, which had surged past 5,000 points, fell more than 75% over the next few years. Countless internet companies went bust, and investors who had chased the excitement of the tech revolution were left with massive losses.

Exhibit 7 (Source: Factset)

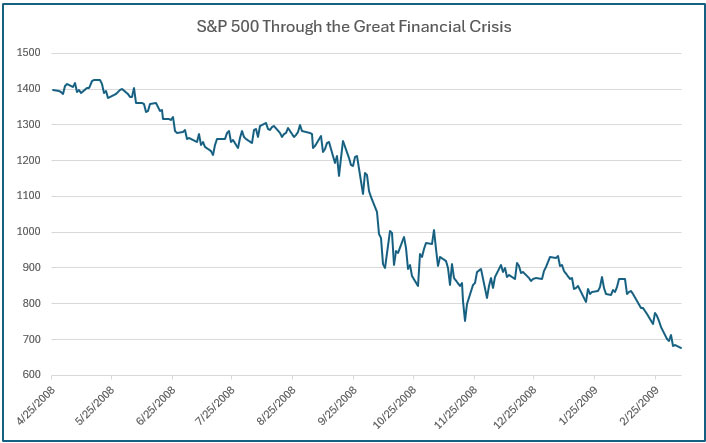

The 2008 Financial Crisis: A Different Kind of Bubble

By the mid-2000s, a new kind of bubble had formed–this time in real estate. Easy access to credit, speculative lending, and the widespread belief that “home prices always go up” fueled a housing boom unlike anything the U.S. had seen before. As with past bubbles, the optimism seemed rational at first. Homeownership was growing, and low interest rates made mortgages more affordable.

But the rise of subprime lending, where banks issued mortgages to borrowers with shaky credit, was the real problem. These risky loans were bundled into complex securities and sold to investors as safe, high-yield investments. When homeowners began to default on their loans, the entire system unraveled.

The 2008 financial crisis hit not just the housing market but the global economy. Major financial institutions collapsed or needed government bailouts. The S&P 500 Index fell by over 50% in less than a year. The crisis triggered the Great Recession, the worst economic downturn since the Great Depression.

Exhibit 8 (Source: Factset)

What Can Today’s Investors Learn?

So what can we learn from 400 years of market history? First, human psychology remains a consistent driver of financial markets. Whether it’s tulips, tech stocks, or real estate, markets are often driven by fear, greed, and the belief that prices will always go higher. Bubbles tend to form when optimism outweighs reality, and when investors ignore the basic principles of value and risk. This is why it is so important to maintain a well-diversifed portfolio and invest directly in quality companies.

Second, government intervention can not only exacerbate bubbles, but also help prevent financial disaster. The key is understanding when government policies–like low interest rates or tax incentives–are encouraging risky behavior. And finally, leverage has repeatedly proven to be a double-edged sword. It amplifies gains during bull markets, but also magnifies losses when the market experiences a downturn.

Keeping History in Mind

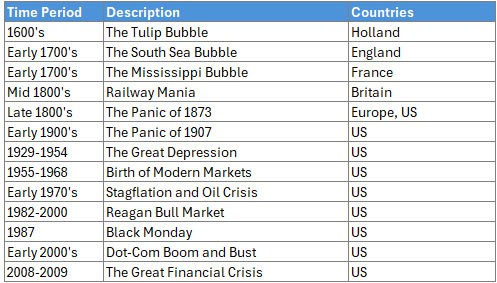

Exhibit 9

As we look to the future, today’s markets continue to show signs of exuberance. Tech stocks once again dominate headlines, cryptocurrencies offer speculative thrills, and the prospect of lower interest rates continue to fuel asset price inflation. Individually, none of these things are necessarily bad, but they should be a reminder to us to be cautious. History has shown time and again that markets are cyclical. Booms and busts are an inevitable part of investing which again makes the case for diversification and quality of holdings.

For investors, the lesson is clear: don’t ignore the past. Markets can seem like they’re rewriting the rules, but the fundamentals of valuation, risk management, and diversification have never changed. Those who remember the lessons of history will be better prepared to navigate whatever the markets bring next.