By Indexopedia Research Team | July 24, 2024 | In

Social Security is a vital program that provides income to retirees, disabled individuals, and survivors of deceased workers. For many individuals, Social Security benefits are their primary source of income during retirement. While there is the option to take Social Security benefits as early as age 62, some individuals choose to delay taking benefits in order to receive a higher monthly payment in the future. The difference in monthly payouts can be significant, often eclipsing $1,000 per month. This means that if a retiree defers receiving their social security benefit until age 70 (when the benefit maxes out), they may be able to squeeze an additional $1000 in monthly income. However, there are several compelling reasons why taking Social Security benefits earlier in life, rather than later in life, may be a better financial decision for you.

In 2024, for example, the maximum Primary Insurance Benefit (PIA) for an individual is $3,743 per month. This is the most that a person could receive if they were to delay taking their social security until their Full Retirement Age (FRA), typically 67 years old. If they further elect to defer commencing their benefit until age 70, they may be eligible for an additional amount, an additional 24% to 32% of their PIA (see Exhibit 1). It is for this reason that many retirees often aim to delay benefit commencement until they reach the age of 70. The alternative, for many people, is to start taking distributions from their retirement accounts in order to provide the funds necessary to support themselves. This begs the question: Is it better to withdraw funds from their retirement accounts or start taking social security prior to the maximum benefit date.

Exibit 1

Category | Age | Reduction/Increase | Benefit Amount |

Earliest | 62 | 30% Reduction | $2,620.10 |

Full Retirement Age | 67 | No Reduction | $3,743.00 |

Investment Risk | 70 | 24% Increase | $4,640.32 |

A common strategy is to hold off on taking social security benefits for as long as possible (up to the age where you would be eligible to receive the maximum monthly payout). However, assuming you are no longer employed (and therefore no longer drawing a regular income), you will need to have at least some source of income. And for many retirees they look to their retirement accounts. However, there are three primary reasons why you should consider avoiding this particular behavior:

- Taking Social Security benefits earlier allows you to keep more of your money invested in your retirement accounts, where there is a potential for further growth.

- Social Security benefits basically expire when the recipient dies, and since no one knows how long they’ll live, it is possible that you may never even live to see a single dollar of your promised benefit. In contrast, your investments will be passed on to your heirs.

- It is widely known that the Social Security program in the United States is under stress and will likely enter an underfunded status sometime in the near future. That could lead to a cause a reduction in benefits. Thus, the more prudent, and conservative, approach might be to “take it while you can.”

Another argument in favor of taking social security early is that, depending on your health and associated life expectancy, you might actually be able to maximize your overall lifetime benefits. While it is true that delaying benefits can result in a higher monthly payment, it takes many years to make up for the benefits that you would have received by taking benefits early. In fact, according to the Social Security Administration, the break-even point for delaying benefits is typically around age 80 or later. This means that if you delay benefits and live beyond the break-even point, you will ultimately receive more in total benefits. However, if you do not live past this age, you may end up receiving less in total benefits than if you had taken benefits early. By taking benefits early, you can ensure that you maximize your overall lifetime benefits, especially if you have concerns about your longevity.

Furthermore, taking Social Security benefits early can provide financial assistance to your family members. Social Security benefits can also be available to certain family members, such as a spouse or children, if they meet certain eligibility requirements. By taking benefits early, you can provide additional financial support to your loved ones who may rely on your benefits for their own well-being. This can help alleviate financial stress and ensure that your family members are taken care of.

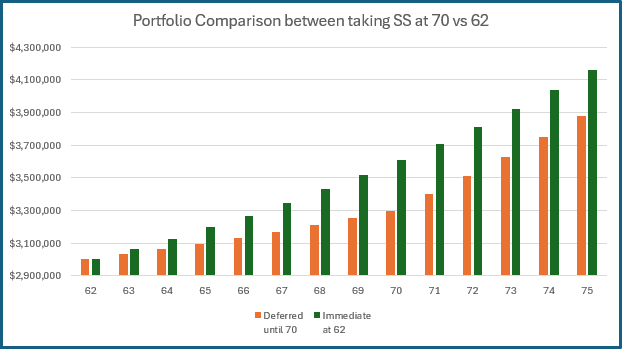

Let’s assume that an investor just retired on his 62nd birthday with a retirement portfolio worth $3 million that is earning an average annual return of 6%. Let’s also assume that he needs $150,000 annually in order to support his lifestyle. That translates into a monthly flow of $12,500. The question becomes: should he withdraw the entire $12,500 from his portfolio or should he supplement that payment by taking social security immediately? If he were to take Social Security right away, he would receive approximately $2,630 each month ($31,560 annually). Let’s perform a comparison of his portfolio immediately preceding his 76th birthday:

Exibit 2

As you can see from the green bars in Exhibit 2, at the end of the investor’s 75th year his portfolio would be worth approximately $280,000 more if he had started taking his Social Security benefit.

In conclusion, taking advantage of Social Security benefits sooner than later can be a smart financial decision for many individuals, especially when compared to the alternative of drawing funds off of retirement accounts. By taking Social Security benefits early you allow your retirement accounts to continue compounding.

Related Articles

Why is Income Important in Retirement?

Fixed Income,

Personal Finance,

Top Personal Finance FAQs,

Why to Buy & Where,

August 14, 2024

How to Start Saving for Retirement

Financial Planning,

Investment Principles,

Personal Finance,

Top Investment Principles FAQs,

May 14, 2024

What does Age have to do with Asset Allocation?

Investment Principles,

Personal Finance,

Top Personal Finance FAQs,

October 23, 2023