Index mutual funds have become synonymous with low-cost investing, promising investors market returns with minimal fees. For small investors, the appeal of these funds lies in their low expense ratios, which can be a fraction of the fees charged by actively managed funds. For example, the Vanguard 500 Index Fund Admiral Shares (VFIAX) boasts an expense ratio of just 0.04%, and the Fidelity ZERO Total Market Index Fund (FZROX) even offers a 0.00% expense ratio. While these figures are enticing, they don’t tell the whole story. The truth is that fund companies often make money through other channels, and there are additional costs borne by investors that aren’t immediately apparent.

How Fund Companies Make Money off Your Assets

1. Securities Lending

One significant source of revenue for fund companies is securities lending. This involves lending out the securities held in the fund’s portfolio to short sellers and other market participants in exchange for a fee. While this can generate income for the fund it also introduces additional risks. If a borrower defaults, the fund could suffer losses, which would impact the investors.

Example: In 2020 alone, one of the world’s largest asset managers earned over $1 billion from securities lending.

2. Payment for Order Flow

Another revenue stream is payment for order flow, where brokerage firms pay mutual fund companies for directing trades through their systems. This practice, while legal, can lead to conflicts of interest, as it may not always result in the best execution prices for trades, potentially affecting the overall performance of the fund.

Example: Fund companies known for their low-cost index funds have faced scrutiny over payment for order flow practices. Although advocates maintain that they seek the best execution for their clients, opponents argue that it creates a conflict of interest.

3. Soft-Dollar Compensation

Soft-dollar compensation involves fund managers receiving research and other services from brokers in exchange for directing trades to them. This can lead to higher trading costs as brokers recoup their costs through higher commissions. These costs, although not directly charged to investors, are embedded in the fund’s overall trading expenses and can erode returns.

Hidden Costs Passed on to Investors

1. Phantom Tax Liabilities

Index funds, like all mutual funds, must distribute capital gains to shareholders at the end of each year. These distributions are taxable to investors, even if they have not sold any shares. This can create “phantom” tax liabilities, where investors incur taxes on gains they did not realize.

Example: In 2020, many investors in one of the largest stock index funds received significant capital gains distributions despite a market downturn earlier in the year, leading to unexpected tax bills.

2. Delistings

Delistings, or the removal of stocks from an index, can have a considerable impact on index performance, which can be viewed as a cost of owning an index fund. Delistings can distort the performance of an index, especially if the removed stock has experienced significant price fluctuations. If a delisted stock performed exceptionally well or poorly before its removal, its absence from the index can create a distortion in the overall index performance, potentially skewing the returns and characteristics of the index. And these performance impacts are reflected as a hidden cost due to the fact that index funds are required to hold the stock until it becomes delisted, whereas direct investing has no such requirement.

Below are examples of some recent high-profile delistings (Exhibit 1):

Notable S&P 500 Delistings since 2000 | ||||

Year | Company | High | Price at Delisting | Decline |

2021 | Xerox | $167.79 | $24.84 | -85% |

2011 | Radio Shack | $23.40 | $15.14 | -35% |

2010 | Eastman Kodak | $9.08 | $5.12 | -44% |

2008 | Lehman Brothers | $85.76 | $0.00 | -100% |

2001 | Enron | $84.90 | $0.00 | -100% |

3. Cash Drag

Index funds need to maintain a cash reserve to meet redemption requests and to take advantage of buying opportunities. This cash drag can reduce the overall returns of the fund, especially in a rising market where the cash is not earning the same returns as the invested assets.

Example: During bull markets, funds with significant cash holdings can underperform compared to fully invested funds. A study by Morningstar found that cash drag can reduce annual returns by up to 0.1% for large index funds.

4. Internal Trading Costs

Mutual funds and ETFs incur trading fees when rebalancing their portfolios to match the underlying index. These fees can add up over time and reduce the net returns to investors. In fact, a Wall Street Journal article indicated that internal trading costs can range between 0.14% and 2.96% annually. Almost three percent! In addition to these trading costs there are also fees associated with the clearing firm, as the price paid for executing trades.

Example: The SPDR S&P 500 ETF (SPY) incurs trading costs when it rebalances to reflect changes in the S&P 500 index, such as the inclusion or exclusion of companies. These costs, although not prominently disclosed, affect the fund’s overall performance.

5. Advisor fees

Some financial advisors charge as much as 2% on top of all the other costs and fees. Financial advisors typically charge fees based on a percentage of assets under management (AUM), known as the asset-based fee structure. This fee structure is designed to align the advisor’s compensation with the client’s investment portfolio size. However, in some cases, advisors charge fees on top of the expenses associated with index funds.

The Illusion of Low-Cost Investing

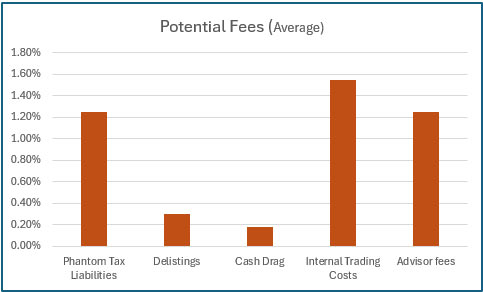

The low expense ratios advertised by index funds can be misleading. While they do represent the direct cost of managing the fund, they do not capture the full picture of the costs and revenue mechanisms involved. The combination of phantom gains, delistings, hidden trading fees, and other “soft” costs means that investors might not be getting the bargain they think they are. Below is a table summarizing the potential hidden costs of investing in “low cost” index funds (Exhibit 2):

Potential Cost | |||

Category | Low | High | Source |

Phantom Tax Liabilities | 0.50% | 2.00% | Kiplinger |

Delistings | 0.10% | 0.50% | Internal Research |

Cash Drag | 0.10% | 0.25% | Internal Research |

Internal Trading Costs | 0.14% | 2.96% | WSJ |

Advisor Fees | 0.50% | 2.00% | Benzinga |

Total | 1.34% | 7.71% | |

In the end, minimizing costs is one of the most effective ways to protect your portfolio during down markets as well as allowing for quicker recovery.

EXIBIT 3

Conclusion

Investors are naturally drawn to index funds due to their low expense ratios and the promise of market returns with minimal fees. However, it is essential to understand that these low costs are often a marketing gimmick used to attract investors. Fund companies have various ways of generating revenue that are not immediately transparent, and investors ultimately bear hidden costs such as phantom tax liabilities, cash drag, and trading fees. As with any investment, it is crucial for investors to look beyond the surface and consider the full range of potential costs and risks. Only then can they make informed decisions and align their investments with their financial goals.

Related Articles

Should I worry about index funds pooled ownership?

Index Investing,

Investment Principles,

Top Index FAQs,

Top Investment Principles FAQs,

October 23, 2023

Do index funds have trading fees?

Index Investing,

Top Index FAQs,

November 2, 2023

Do I need to pay an investment advisor a fee to buy index funds?

Index Investing,

Top Index FAQs,

Types of Indexes,

September 30, 2024