By Indexopedia Research Team | September 30, 2024 | In

Most retail investment advisors charge investment advisory fees to invest in model portfolios, index funds, and ETFs. Because index funds, ETFs, and portfolio models are often managed by a third-party investment company, investors are subject to hidden expense ratios and trading fees. When investors pay an investment advisory fee in addition to the hidden fees of the funds, the total cost can sometimes be as high as 2.5% to 4%. All too often, when retail investment advisors discuss costs, they sometimes fail to disclose the real costs of the funds, which are not always transparent to investors.

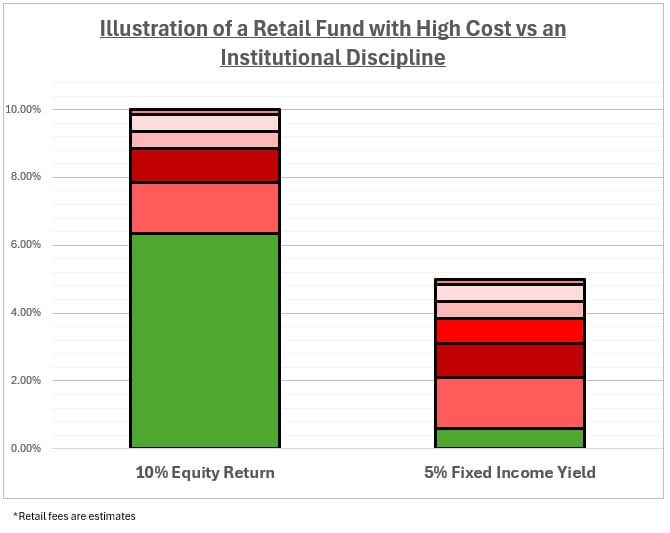

So, when you’re investing, especially in portfolio models, pooled mutual funds, or ETFs, be aware that you generally don’t need to use a retail investment firm unless they are actively giving advice. For example, if you’re using an investment advisor and paying them 1% for advice while being invested in a portfolio model of mutual funds, the 1% advisory fee is just a part of the total cost. Expense ratios, trading costs, and clearing costs are other expenses that may easily push your total cost to over 3.7% (see exhibit 1).

Exhibit 1

While hidden costs negatively impact returns, other factors affecting results should also be considered, such as the quality of holdings, direct ownership, small investor herding impact, pass-through taxes, low yields to maturity, and pricing disadvantages.

If you’re paying an investment advisor a 1% fee for a model of ETFs or index funds and they don’t add significant value through trading or portfolio management, you may want to reconsider your options. Why? Most investment advisors are not actually money managers. In fact, most don’t own the investment firm; they are employees of a larger broker-dealer. The key is that, as an investment advisor, they are licensed to give advice. That advice comes at a cost, typically in the form of an annual advisory fee. However, that fee is often separate from the asset management fee. Essentially, the investment advisor charges you to place your money with another party that manages it, which comes with its own set of costs.

Unless the advisor can simplify your financial life or demonstrate long-term value, the fees may be too high, the results may be average to low, and there may be no real need to continue paying advisory fees when your money isn’t being managed directly.

Unless the advisor can simplify your financial life or demonstrate long-term value, the fees may be too high, the results may be average to low, and there may be no real need to continue paying advisory fees when your money isn’t being managed directly.

Costs seem to be one of the biggest concerns for investors, but if one were to examine the details of their portfolio, they would find other factors impacting investment results. These might include small investor herding impacts, reconstitution of market-cap index funds, quality of holdings, cash drag, pooled ownership, and more.

This is why Linden Thomas & Co. set out years ago to build a firm focused on private institutional earnings through equity indexes and private fixed-income portfolios. This approach allows affluent investors to avoid the high costs of retail investing while still having their portfolios managed directly through individual stocks and bonds. No more high investment advisory fees and the hidden fees of the funds they own.

So, if you’re only invested in a model of index funds or you’re a do-it-yourself investor, paying an annual fee for advice on something you could have bought without an advisor’s cost may not be necessary. For investors who wish to manage and trade their investments independently, our brokerage accounts allow them to buy funds directly through a trading account without an annual investment advisory fee.

Related Articles

What are Advisor Fees?

Index Investing,

Personal Finance,

Top Index FAQs,

Top Personal Finance FAQs,

October 23, 2023

Are advisor fees and costs important to investment results?

Investment Principles,

Top Investment Principles FAQs,

January 8, 2025

What Does Your Portfolio and an Onion Have in Common?

Financial Planning,

Personal Finance,

October 1, 2024