Some mutual funds grow so large they start to resemble overcrowded restaurants — once highly coveted for their quality, now overwhelmed by demand.

And that tends to strain performance.

This phenomenon, known as mutual fund bloating, happens when a fund attracts more assets than it can efficiently manage. While it sounds contradictory, success can eventually hinder the fund’s flexibility, impact returns, and make it harder to implement its original strategy.

Let’s break down what mutual fund bloating actually means, why it happens, and how it can affect your portfolio, especially if you’re relying on actively managed strategies.

What Is Mutual Fund Bloating?

Mutual fund bloating occurs when a fund’s ballooning size starts to work against it. In practical terms, the fund’s assets under management (AUM) exceed the level at which the manager can efficiently deploy capital without sacrificing returns or deviating from the fund’s original investment strategy.

Bloating is typically most relevant for active managers, particularly those focused on small-cap stocks and less liquid markets. With more capital to deploy, managers may feel pressure to spread assets across additional holdings or shift into larger, more liquid companies. While those decisions aren’t unsound on the surface, they may lead to style drift.

Over time, bloating can:

- Dilute performance, as new holdings may not offer the same return potential as original selections

- Reduce agility, making it harder to move in and out of positions without impacting prices

- Increase overlap with benchmarks, causing the fund to behave like an index (despite charging active management fees)

In short, size can become a liability. More capital can make it challenging to maintain the performance that attracted investors in the first place.

How Do Funds Become Bloated?

Bloating is often the byproduct of success. One classic case is the Fidelity Magellan Fund under Peter Lynch. From 1977 to 1990, Lynch grew the fund’s assets from $18 million to $13 billion while delivering an impressive 29% average annual return. Assets continued to swell even after his departure, eventually peaking near $100 billion by the late 1990s.

Without Lynch at the helm and with such enormous size to manage, the fund struggled to replicate its prior outperformance. Many attribute that in part to the constraints that come with managing massive inflows.

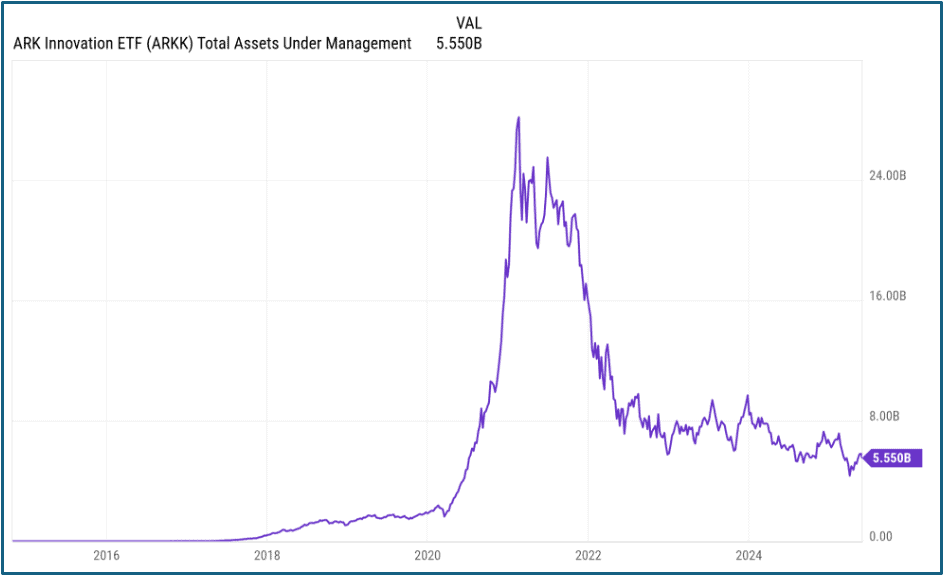

Bloating isn’t exclusive to mutual funds either. The flagship exchange-traded fund of Cathie Wood’s ARK Invest, Ark Innovation ETF (ARKK), is a prime example.

After gaining 153% in 2020, the fund saw its assets balloon from $2 billion to about $28 billion in just over a year. But with rapid inflows came new challenges: finding enough high-conviction ideas and maintaining its success. As performance cooled, so did investor enthusiasm; as of May, ARKK’s assets have retreated to just $5.5 billion.

Is Asset Bloating Always Bad?

The accumulation of assets isn’t inherently bad — generally, that’s a good sign that a fund is doing something right.

Some funds even benefit from scale. Index funds and broadly diversified strategies can take in large inflows, because their objective isn’t to beat the market; they’re designed to replicate it. And in the case of bond funds, larger size can even improve access to new issues and better pricing.

The primary determining factor is strategy structure. A passive, large-cap fund tracking the S&P 500 can comfortably handle hundreds of billions in assets.

How Managers Try to Prevent Asset Bloating

Many fund managers will take steps to mitigate the risk of bloating before it impedes their strategy and performance. Two common approaches include:

- Closing the fund to new investors. This is one of the most direct methods. By limiting new inflows, managers can preserve their investment approach and avoid being forced into less optimal positions. While not exactly popular with asset managers seeking to grow AUM, it strongly indicates integrity and commitment to current investors.

- Launching new share classes or similar strategies. Rather than stuffing more assets into a single vehicle, some fund families will launch similar strategies with slightly different mandates to spread capital more efficiently across offerings.

Each tactic comes with trade-offs. That’s why understanding how a manager is approaching size constraints — or whether they acknowledge them at all — is an important part of fund due diligence.

What Can Investors Do About Bloating?

Bloating isn’t obvious, and not every fund is vulnerable to it. But for investors evaluating actively managed funds, there are a few ways to stay vigilant:

Look at asset flows and AUM trends. If a fund has recently seen a surge in inflows, such as after a stretch of outperformance, it may be at risk of bloating. Parabolic growth can outpace a manager’s ability to deploy capital effectively.

Understand the strategy’s capacity limits. Smaller-cap or high-conviction strategies tend to be more sensitive to size. If the fund’s portfolio starts drifting toward mega-cap names or growing in number of holdings, that could be a red flag.

Watch for benchmark creep. If an active fund increasingly resembles its benchmark but still charges active fees, it may be losing its strategic edge. Bloating could be part of the reason.

Don’t chase past performance alone. History is littered with funds that ascended rapidly, gathered billions in assets, then underperformed as size eroded their agility. A more measured approach may lead to better long-term outcomes.

Consider whether the fund has limited inflows. Some managers will proactively close funds to new investors to avoid bloating and preserve their strategies. That’s not always possible or desirable, but when it happens, it at least signals an awareness of capacity constraints — and a willingness to prioritize current stakeholders over asset accumulation.

As with any investment decision, the key is context. Bloating isn’t necessarily a dealbreaker (nor is it guaranteed to happen even with strong performance), but it’s a worthwhile consideration, especially when you’re relying on a manager’s skill to outperform.

Related Articles

How delistings impact investment results, especially when it comes to index funds

Index Investing,

October 15, 2024

What is the Real Turnover of Pooled Index Funds?

Index Investing,

January 8, 2025

What are Mutual Fund Inefficiencies?

Index Investing,

Indexing for the Affluent,

Investment Principles,

Top Investment Principles FAQs,

November 19, 2024