By Indexopedia Research Team | November 19, 2024 | In

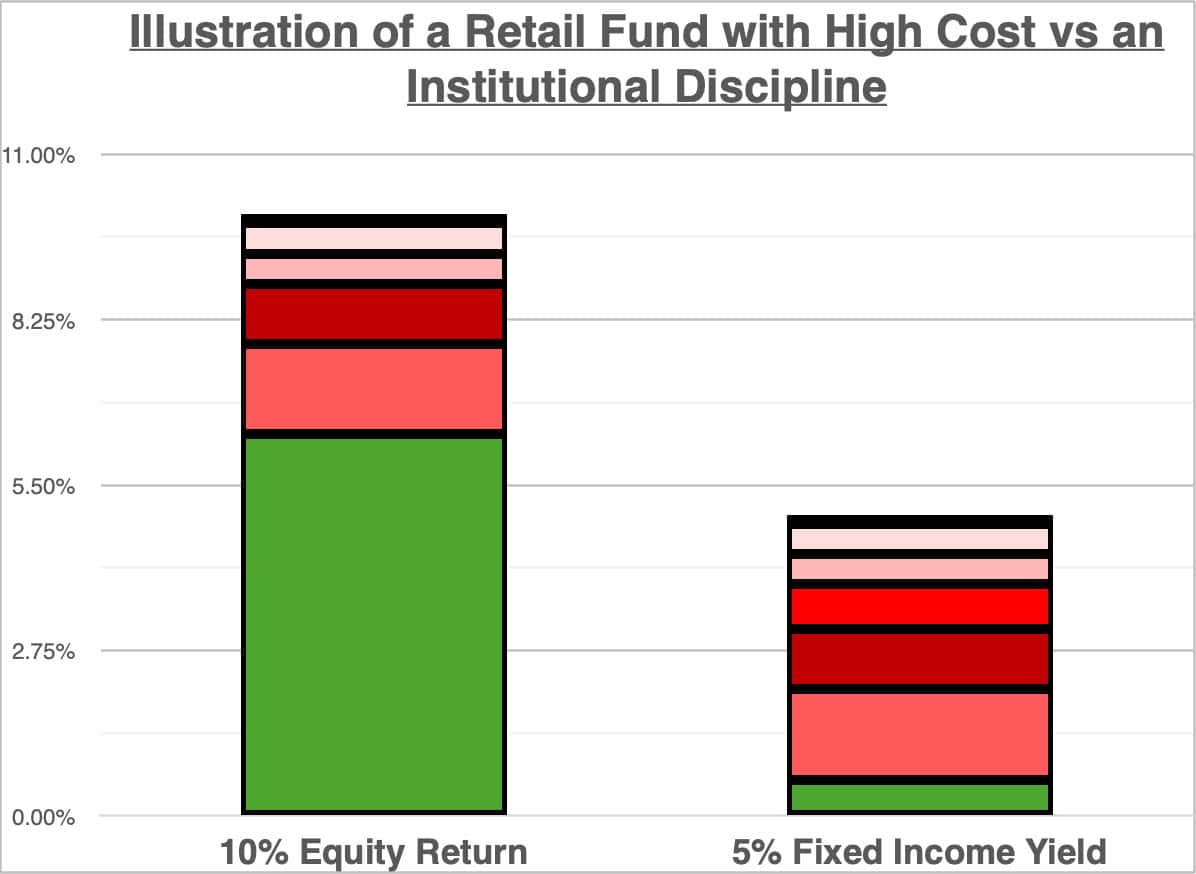

Mutual funds allow investors to pool their money to collectively invest in stocks, bonds, and other securities. These funds are portfolios consisting of money from various investors, used to build a diversified collection of assets including stocks, bonds, and other securities. While this collective investment approach can offer benefits to small investors, it is often less efficient than options like Institutional Direct. The following chart highlights how inefficiencies reduce overall returns for investors:

*Fees and cost are hypothetical and not reflective of any specific cost associated with a particular fund.

Inefficiencies of Mutual Funds:

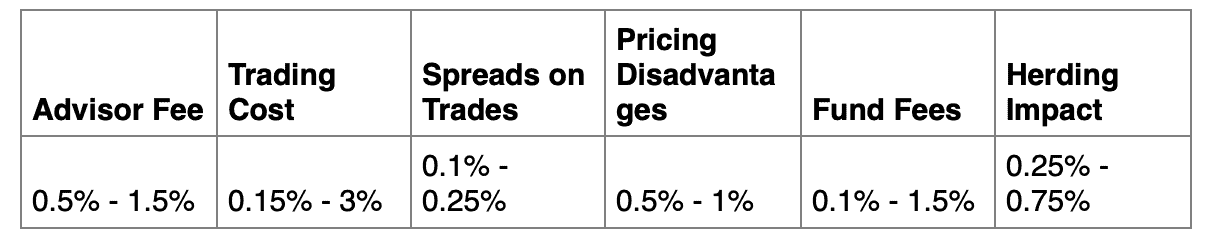

1. Fees and Expenses

- RIA Advisor Fee – Advisors often charge fees for portfolio construction and asset allocation but may simply invest clients in funds they don’t directly manage or construct.

- Expense Ratios – Mutual funds impose expense ratios, which encompass management fees and operational costs, directly impacting investor returns.

2. Ownership & Transparency

Pooled market-cap mutual funds do not give investors direct ownership or transparency. Pooled ownership leaves investors with little insight into their investments, the quality of their holdings, or cost-basis. Assets are pooled with other investors and managed by a third-party. Every investor in the fund has different needs, risks, and concerns. This lack of transparency leaves investors with little understanding of the inefficiencies in their pooled products.

Control & Customization

Mutual funds offer limited control and customization, as they are pre-packaged investment products. While investors can select funds based on the strategy they follow, they have little say over the individual securities held. In contrast, Institutional Direct provides greater flexibility, allowing investors to exclude specific securities or align their portfolios with personal values and preferences, offering a more tailored investment strategy.

- Investors in mutual funds don’t have the ability to gift appreciated shares or tax-loss harvest, meaning that they have less control over their taxes.

Pricing Disadvantages

Mutual funds sometimes purchase bonds priced at premiums or discounts, which can create pricing disadvantages when investors buy shares. For instance, when bonds are purchased at a premium, new investors pay more than the bond’s face value. Conversely, bonds bought at a discount could result in lower yields for the investor.

Herding Impacts

Frequent inflows and outflows from smaller investors can force fund managers to buy and sell positions to meet redemption needs. This dynamic creates inefficiencies, as fund managers must maintain cash reserves to cover redemptions, which often yield little to no return but still incur expenses. During market downturns, panicked small investors tend to sell, forcing fund managers to liquidate positions at suboptimal times, further eroding fund performance.

Spreads on Trades

The spread is the difference between the bid price (the price at which someone is willing to buy a security) and the ask price (the price at which someone is willing to sell a security). The fund may be selling assets for less than an individual investor would, and buying assets for more than an individual investor would, due to the typically large size of each trade. The result is a drag on the fund’s performance.

Internal Trading Costs

Also known as turnover costs, these expenses arise from the buying and selling of securities within a pooled fund’s portfolio. Mutual funds with higher turnover ratios have higher internal trading fees, as more frequent buying and selling of securities leads to increased transaction costs.

Capital Gains Taxes

Mutual funds distribute capital gains to their shareholders, which can create tax liabilities, even for investors who haven’t sold their fund shares. Additionally, investors have no control over the timing of these distributions, potentially leading to higher tax bills.

- A fund’s turnover ratio refers to the frequency with which it buys and sells securities. A fund that executes many trades throughout the year has high asset turnover. The result is most capital gains the fund generates are short-term gains, which means they’re taxed at your ordinary income tax rate and not the lower capital gains tax rate.

- Example: Let’s say your mutual fund owns 10 stocks and one of them, Amazon, sees a big jump in value. The mutual fund manager decides to sell some of the Amazon shares to manage risk and maintain the fund’s asset allocation. By passing the proceeds from the Amazon stock sale back to investors, it triggers a capital gains tax event for shareholders, even if they didn’t sell their shares in the fund.

Down Market Pass-Through Taxes

Because mutual funds and exchange-traded-funds are pooled, and the equities are often bought prior to many investors entering the fund, investors can be stuck with a tax liability even during down markets. When the portfolio manager sells appreciated holdings within the fund, the tax impacts are passed on to all of the fund’s investors. This is doubly painful when investors make a large investment, see the market decline by 10-30%, but still realize a taxable capital gain due to legacy holdings. This is another reason Linden Thomas & Co. set out to build a more efficient index for affluent investors by allowing investors to own positions directly.

Proxy Voting

A less talked about disadvantage of pooled index funds is how much power big index fund companies have. Because large index funds pool investors, small investors have no say in the proxy votes of the companies they own. This is why big Wall Street index companies exercise so much control over corporate actions and the selection of boards of directors. Small investors have no power to vote based on their faith or corporate belief, which is yet another reason why direct ownership of holdings matter.

It is evident that mutual funds come with several disadvantages but can still offer easy diversification for small investors. Investors with large portfolios would be better served by an approach that allows for direct ownership and control, such as Institutional Direct.

Related Articles

Comparing the Tax Efficiency of Mutual Funds, ETFs, and Institutional Money Managers. Which should you choose?

Index Investing,

Indexing for the Affluent,

Personal Finance,

Top Personal Finance FAQs,

September 17, 2024

Exploring the Different Forms of Index Investing: Mutual Funds, ETFs, and Institutional Indexing

Index Investing,

Top Index FAQs,

Types of Indexes,

September 24, 2024

Are advisor fees and costs important to investment results?

Investment Principles,

Top Investment Principles FAQs,

January 8, 2025