By Indexopedia Research Team | July 11, 2024 | In

Stocks are considered risk assets. Every stock can either move up in value, or down in value. Losing value is considered downside risk, and it is this risk that is of most concern to investors. In the 1950’s Harry Markowitz, the father of Modern Portfolio Theory, figured out that the overall risk of a portfolio could be meaningfully reduced by simply spreading a stock’s individual risk by owning a portfolio of several stocks.

Concentrated portfolios, those dominated by a small number of names, often arrive at this point due to rapid price appreciation. So, while concentration presents a real and measurable risk, many investors are reluctant to recognize it, let alone do something about it. They may view their brokerage statements and be enamored by the results.

The problem is that a stock which experienced a rapid 20% rise in price may also experience a 20% decline. Investors have short memories, and even large market “corrections” are often quickly forgotten, replaced with the euphoria of watching a few high-flyers soar increasingly higher. It can be intoxicating. But it also represents a significant risk.

So just how large and dangerous is the risk of overconcentration? It depends. Some portfolios hold hundreds of positions, so the risk of being overly concentrated is minimal. This risk can be much greater for smaller portfolios.

How did I get here?

The most common path to concentration risk is owning market cap weighted index funds. These are the traditional passive investment vehicles favored by a majority of investors. The problem is that the weighting methodology is based almost entirely on a stock’s market cap, which is defined as the number of shares outstanding multiplied by the current price. So, if a stock has risen by 20%, its weight in the index will increase. And the investor will likely now own far more of that stock than he or she intended. A simple way for investors to mitigate that risk is to seek investment portfolios that are weighted by something other than market cap. For instance, an equal-weighted portfolio – one in which each stock is assigned the same weight – provides enhanced diversification and offers better downside protection.

How concentration risk impacts your portfolio

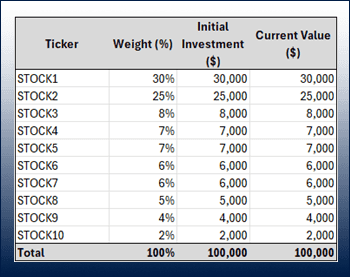

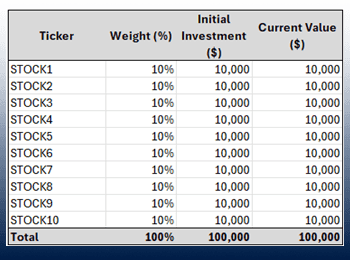

Assume we have a portfolio that holds ten stocks, and that the portfolio is weighted by size (market capitalization). Two of the stocks happen to be quite large and comprise positions of 30% and 25% respectively (see Exhibit 1):

EXHIBIT 1

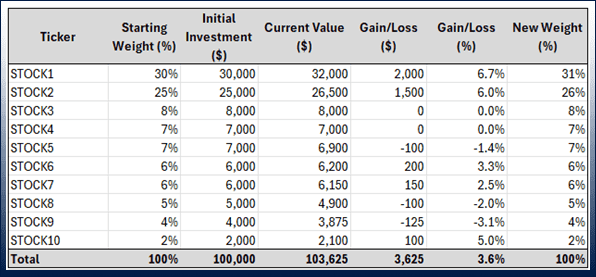

Let’s see what happens during a typical 6-month market cycle. Assuming the overall market rose by 2.5%, we can see in Exhibit 2 that the hypothetical portfolio outperformed the market by 1.1% (3.6% – 2.5%):

EXHIBIT 2

In this case, the high-flyers (STOCK1 and STOCK2) accounted for 97% of the performance as they were up an average of 6.3% during the period. The rest of the portfolio increased only 0.50% on average, but that underperformance was offset by the two outsized positions and, as a whole, the portfolio beat the market.

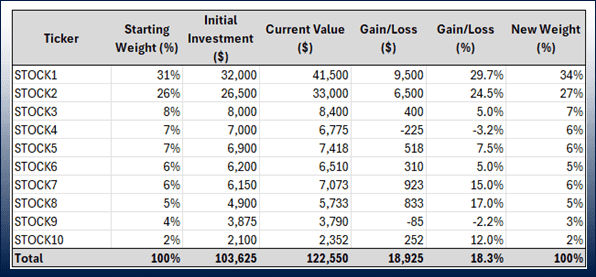

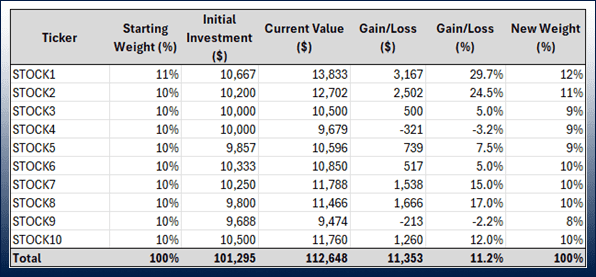

Let’s now see what happens when the market rises sharply, by say 10% over the following 6 months. Below is a picture of how the portfolio would appear at the end of this period:

EXHIBIT 3

In this case the portfolio handily beat the market by 8.3% (18.3% – 10%). The high-flyers (STOCK1 and STOCK2) still accounted for the bulk of the overall performance. They were up an average of 27.1% and were responsible for 85% of the total performance. Most investors would be thrilled to find themselves in this position, admirably beating a hot market by such a wide margin (Exhibit 3).

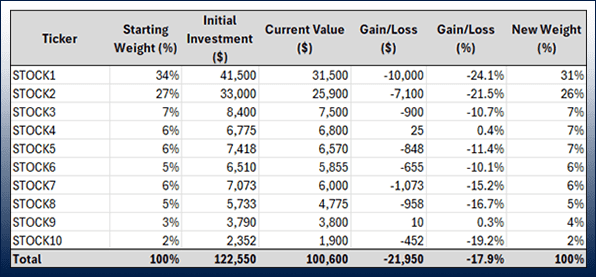

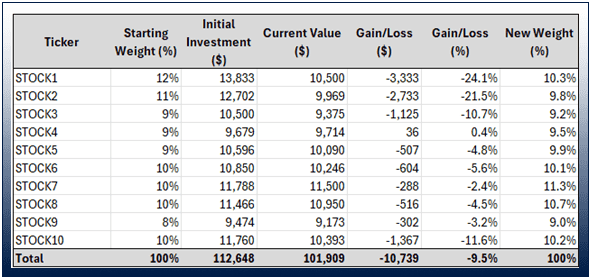

But what happens when there is a market correction, causing prices to fall sharply? Assume the market has just experienced a 10% decline, the typical definition of a correction, during the 6-month measurement period. What does the portfolio look like now?

EXHIBIT 4

In Exhibit 4, you can see that the portfolio severely underperformed the market, falling by almost 18%, a full 7.9% worse than the already abysmal performance of the market, which dropped by 10%. Once again, the collective culprit is the top two holdings, STOCK1 and STOCK2, which accounted for 61% (34% + 27%) of the total starting weight. In this case, the other eight stocks in the portfolio only fell by an average of 10.3%, in line with the broader market. The top two positions fell by almost 23%, dragging the entire portfolio down with them. This example clearly demonstrates just how destructive owning a highly concentrated portfolio can be, particularly in a down market.

Let’s see how the portfolio would have performed if each stock were weighted equally (Exhibit 5):

EXHIBIT 5

Revisiting the first scenario, a typical environment where the market ekes out a 2.5% gain during a 6-month period, the results of the equally-weighted portfolio are as follows (Exhibit 6):

EXHIBIT 6

In this instance, the portfolio outperformed the market by 1.2% (11.2% – 10%) and the high-flyers accounted for only 50% of the overall portfolio (vs 85% in the cap-weighted portfolio).

While this example clearly illustrates the benefit of diversification and the minimization of concentration risk, the largest impact is felt when there is a sharp decline in the market. Continuing with the hypothetical equal-weighted portfolio, this is what happens (Exhibit 7) when the market experiences that same 10% correction:

EXHIBIT 7

In this example, the portfolio actually beat the market. Compared to the market cap weighted version of the portfolio, this one outperformed by 8.4% (-9.5% vs -17.9%). In the cap-weighted portfolio, the two high-growth stocks were responsible for losing almost 14% of the value of the portfolio whereas in the equal weighted portfolio they were only responsible for losing 5.4%, effectively saving the investor almost 9% in losses!

The easiest way to avoid concentration risk

To avoid the risk of overconcentration an investor should plan accordingly. Investing in market cap weighted index funds, for example, is what leads many investors down this path. There are several alternatives to this style of investing. For example, an investor can choose equal weighted funds, similar to the example above. Direct index investing is another viable alternative. With the assistance of an investment advisor, an investor can gain direct exposure to a diversified portfolio of stocks, carefully curated by professional stock analysts who have experience navigating the pitfalls of a volatile market and can provide the knowledge and guidance necessary to avoid the perils of overconcentration.

What do to if you have a high degree of concentration risk

A common strategy is to simply sell or trim your outsized positions, reinvest the proceeds in a more diversified investment vehicle, and accept the tax consequences. Assuming you have held the investment for at least one year, you will most likely face a more lenient tax burden due to the long-term holding period of your investment.

Wrapping it up

Overconcentration in a handful of names can be particularly destructive to your long-term financial plan. The best way to mitigate the risk of overconcentration is to avoid it. Pursuing well diversified, professionally managed direct index funds is one of the best ways to ensure your portfolio steers clear of this potentially hazardous condition. Since this is not always an option, there are ways to deal with it after the fact. Unfortunately, these are usually accompanied by a hefty price tag, in the form of capital gains taxes.

Related Articles

How Portfolio Overlap Could Be Putting Your Investments at Risk!

Financial Planning,

Investment Principles,

Personal Finance,

Top Investor Mistakes,

December 10, 2024

Historical examples of hot sectors that didn’t end well

History of Markets,

Investment Principles,

Knowledge & Insights,

Markets,

Top Investor Mistakes,

July 11, 2024

How does FOMO negatively impact my investment results?

Investment Principles,

Personal Finance,

Top Investor Mistakes,

Top Personal Finance FAQs,

January 8, 2025