The recency effect plays a subtle but powerful role in investment decision-making. In essence, people tend to place disproportionate importance on recent performance while discounting the long-term lessons the market has taught us. In markets, this often leads investors to chase what has recently done well and abandon investments that may be temporarily underperforming. While it may feel intuitive to follow recent performance, it often leads to poor outcomes and missed opportunities.

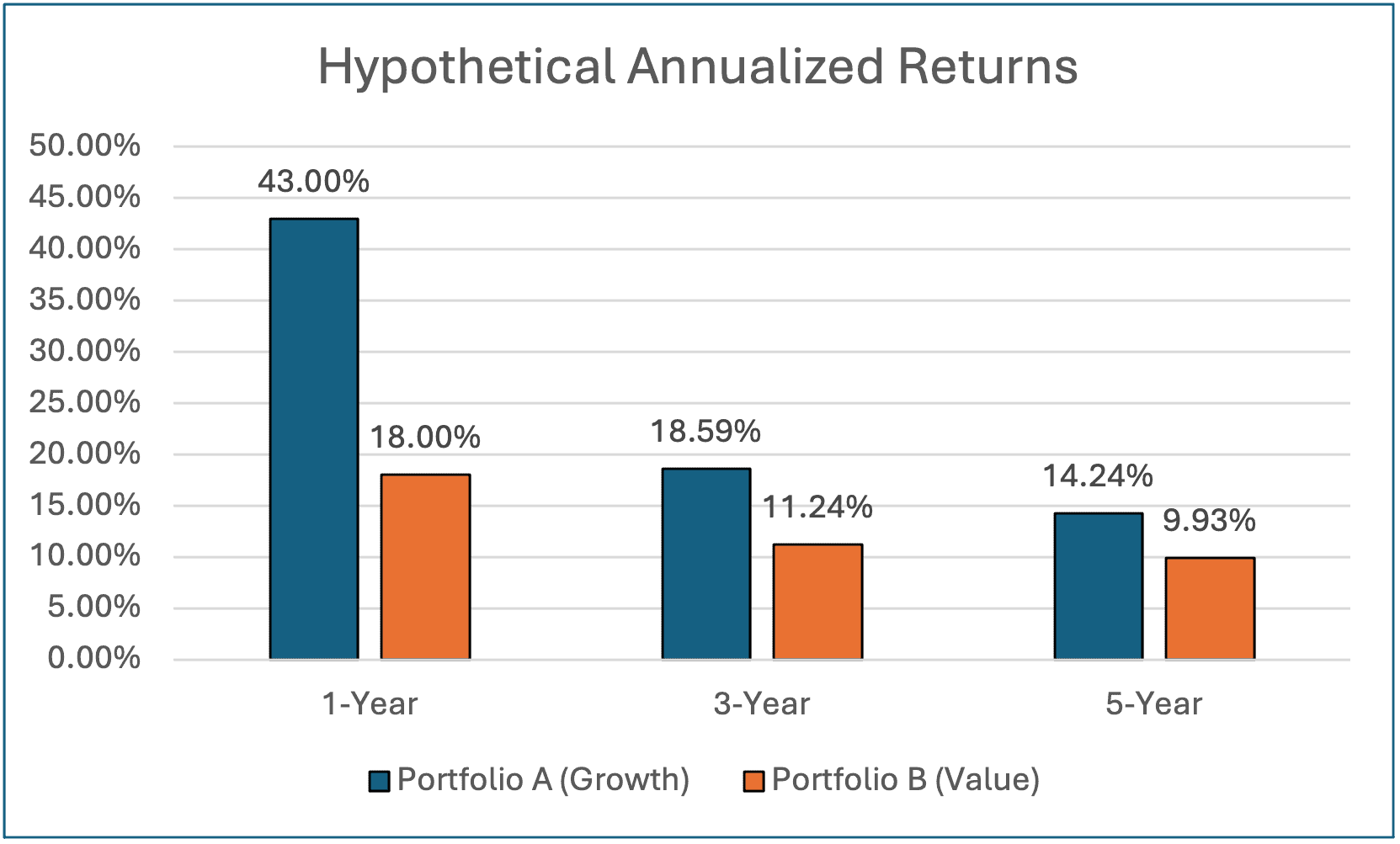

Consider this simple example: Two hypothetical portfolios, Portfolio A and Portfolio B, generate the same average return for four years straight, 8 percent annually. In the fifth year, however, growth stocks surge by 43 percent, while value stocks rise just 18 percent. Portfolio A, which leans into growth, now has far better one-, three-, and five-year average returns than Portfolio B. An investor looking at trailing returns might conclude Portfolio A is the superior strategy and move money accordingly.

(These hypothetical returns and time periods shown are included strictly for illustrative purposes. These returns are not reflective of any investment strategy by the investment adviser nor are they the results of any client account managed by the adviser)

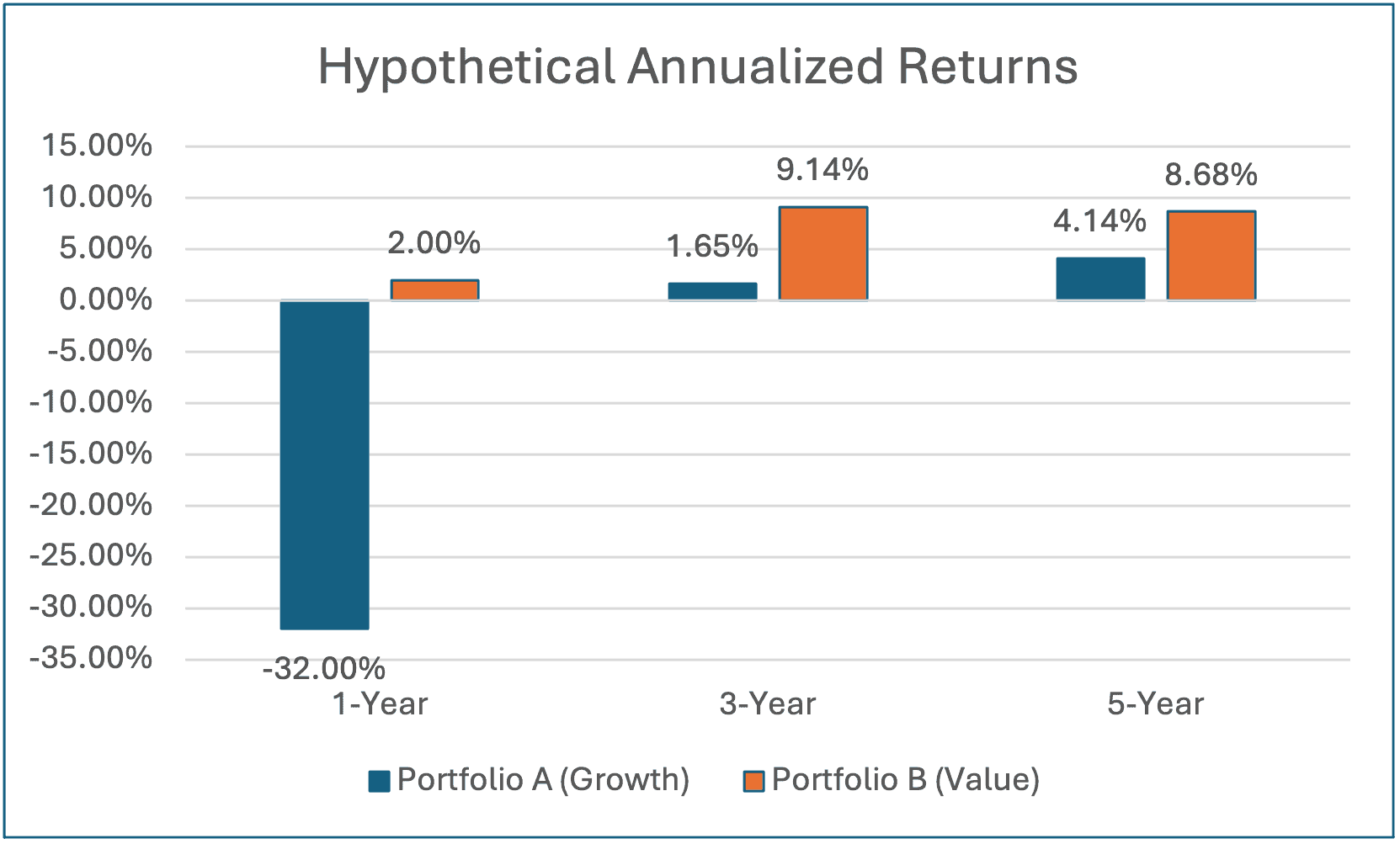

But in year six, if growth stocks decline and value rebounds, the entire narrative can flip.

(These hypothetical returns and time periods shown are included strictly for illustrative purposes. These returns are not reflective of any investment strategy by the investment adviser nor are they the results of any client account managed by the adviser)

At the end of year 5, Portfolio A’s 1-, 3-, and 5-year average return suggested that Portfolio A was the stronger performer, but in year 6 the opposite was true. This highlights how a single year’s return can flip average returns, and perceptions, on their head.

This is the core danger of the recency effect: allowing short-term performance to bias our interpretation of an entire investment strategy. Twelve months can drastically alter averages. Investors may feel tempted to chase returns, even if the underlying assets are now overvalued, or abandon high-quality investments simply because they have underperformed temporarily. The better strategy is to stay disciplined, spread risk, and remain grounded in valuation and fundamentals.

This pattern repeats across decades. The “Nifty Fifty” stocks in the early 1970s, widely regarded as sure things, collapsed during the 1973 to 1974 bear market. During the tech bubble of the late 1990s, the S&P 500 posted an average five-year return of nearly 29 percent. By the time the bubble burst in 2000, many investors had abandoned diversified portfolios to chase large-cap tech, just in time to capture three straight years of losses.

The 2020 to 2021 recovery following the COVID crisis provides another modern example. After a rapid crash in March 2020, the S&P 500 rebounded sharply, driven by high-growth tech names. Investors who shifted heavily into those winners based on recent gains were then whipsawed by value and energy leading the market in 2022.

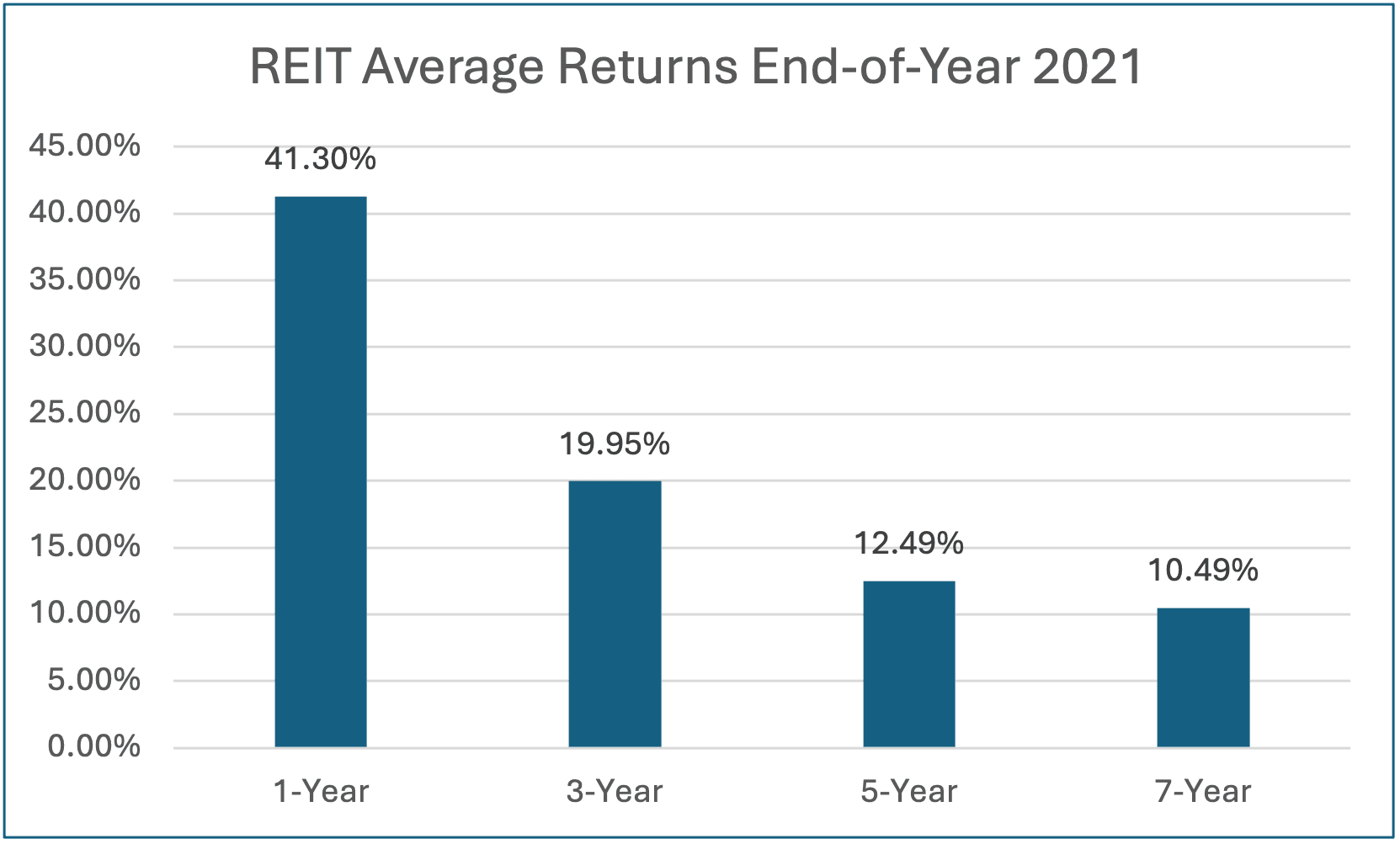

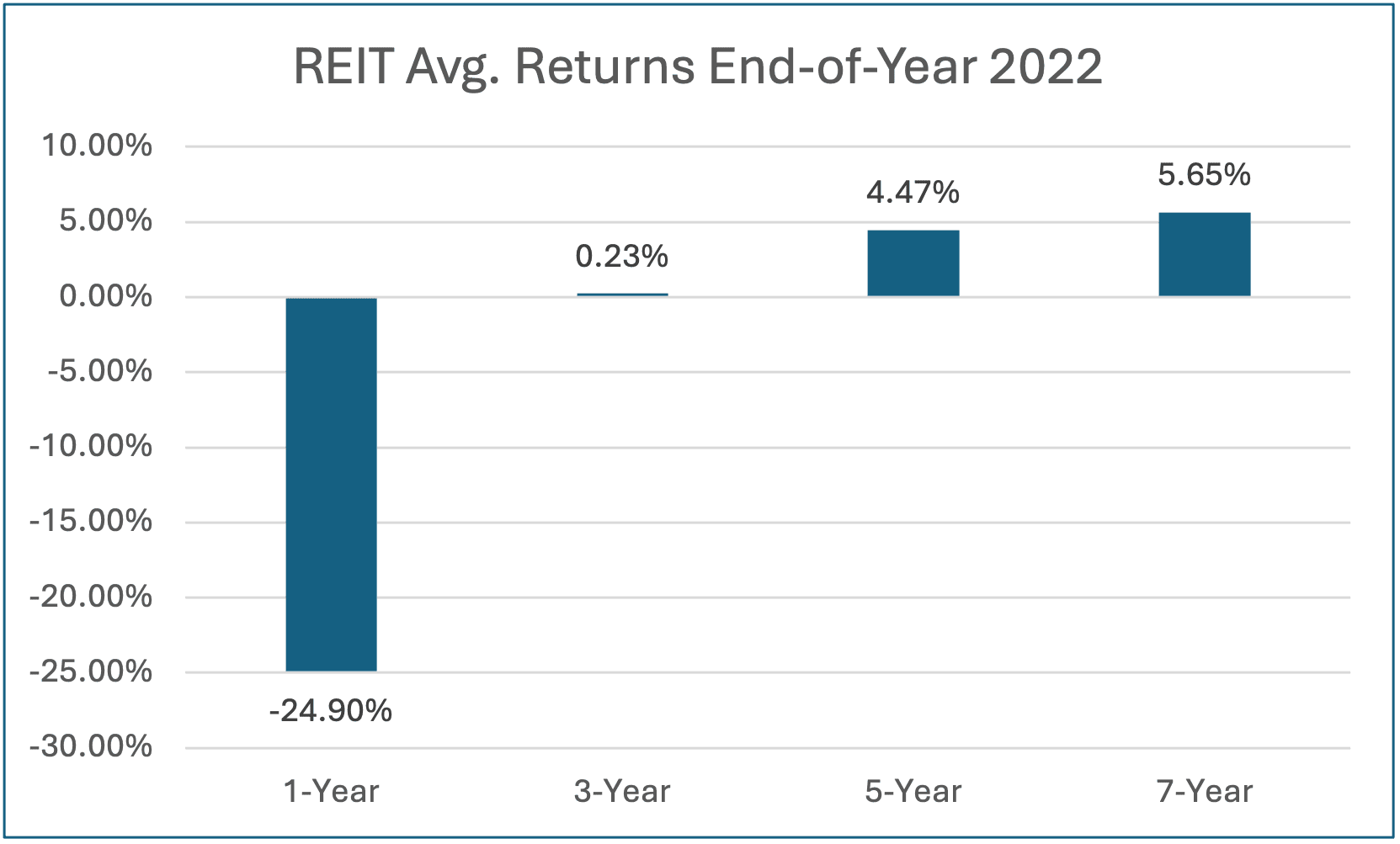

Even real estate investment trusts (REITs), which have long cycles, show this effect. In some years, REITs outperform traditional equities by a wide margin, attracting investors chasing strong trailing returns. But if those same investors abandon a balanced allocation to overweight REITs, they may regret it the following year, when returns often revert to the mean.

Source: JP Morgan Guide to the Markets (NAREIT Equity REIT Index)

(an index is unmanaged, and you cannot directly invest in an index)

(Past performance is no guarantee of future results)

According to research cited by Morningstar and Baird, nearly every top-performing long-term fund manager underperforms their benchmark over some rolling 12-month period. Yet many investors react to that underperformance by jumping ship. In reality, temporary underperformance can be the very thing that sets the stage for future outperformance!

Fund flows further illustrate the point. A study by Morningstar showed that investor cash flows tend to peak after periods of strong fund performance and fall during times of underperformance. The result: the average investor return often trails the return of the fund itself, simply because of poorly timed entries and exits driven by emotion and recency bias.

This is also why fund managers worry about size. A previously nimble fund that outperformed might become bloated with assets after a strong year. That can hinder flexibility and lead to lower returns. The Fidelity Magellan Fund under Peter Lynch is a classic case. As the fund grew from 18 million dollars to over 14 billion dollars in assets, its ability to continue outperforming narrowed.

The answer isn’t to ignore performance altogether, but rather to interpret it wisely. Trailing returns provide a data point, not a directive. Before abandoning a well-tailored portfolio, consider the reasons for past performance, the current valuation of assets, and the long-term outlook for each sector or strategy.

Spreading risk is a built-in defense against recency bias. By owning different asset classes and sectors, investors don’t have to bet on what is currently winning or worry about missing the next hot trend. If technology leads one year, energy may lead the next. The point is to remain positioned for both.

Time and again, markets have demonstrated that leadership rotates. Sectors that lag can eventually lead, and vice versa.

To build lasting wealth, investors must train themselves to look forward, not backward. Avoiding emotional shifts and return-chasing behavior is one of the most valuable skills an investor can develop. Stick with a plan, rebalance strategically, and evaluate opportunities based on fundamentals, not headlines. Recency should inform but never dictate. In investing, discipline trumps memory.