A well-crafted financial plan is like a detailed map guiding an investor toward long-term financial success. It accounts for goals, risk tolerance, cash flow needs, and investment strategies. However, even the most carefully constructed plan can be rendered useless if an investor falls victim to emotional decision-making. Fear, greed, impatience, and other behavioral pitfalls have the power to derail financial progress, often leading to damaged results or even financial ruin. In the world of wealth management, planning alone is not enough – discipline and adherence to the plan are equally critical.

The Best Plan in the World is Useless If You Can’t Follow It

Imagine an investor who has worked with a financial advisor to create a comprehensive plan for retirement. The plan includes an efficient portfolio of stocks and bonds, a systematic distribution strategy, and an emergency fund to handle unexpected expenses. Yet, when the market experiences a sharp decline, fear takes over. The investor panics and liquidates their portfolio at the worst possible time, locking in losses and abandoning the carefully laid-out strategy. The plan, which was designed to weather market volatility, is now meaningless because the investor failed to follow it.

Similarly, consider the opposite scenario. An investor sees a sudden surge in technology stocks. Despite having a financial plan that discourages excessive risk-taking, greed takes hold, and they invest a large portion of their assets in a highly volatile asset class. When the speculative bubble bursts, the investor suffers significant losses, jeopardizing their long-term financial security.

1. Emotional Decision-Making

Investors often make decisions based on emotions rather than rational analysis. Fear and greed are two of the most powerful drivers of investment mistakes. When markets are soaring, investors may experience FOMO (fear of missing out) and pile into stocks at overinflated prices. Conversely, when markets decline, panic selling often sets in, leading investors to sell at a loss.

Consider the financial crisis of 2008: Many investors, spooked by plummeting stock prices, sold their holdings at the bottom. Those who stayed invested, however, saw their portfolios recover and grow significantly in the following years. The key takeaway? Emotional decision-making can lead to buying high and selling low–the exact opposite of a sound investment strategy.

2. Market Timing

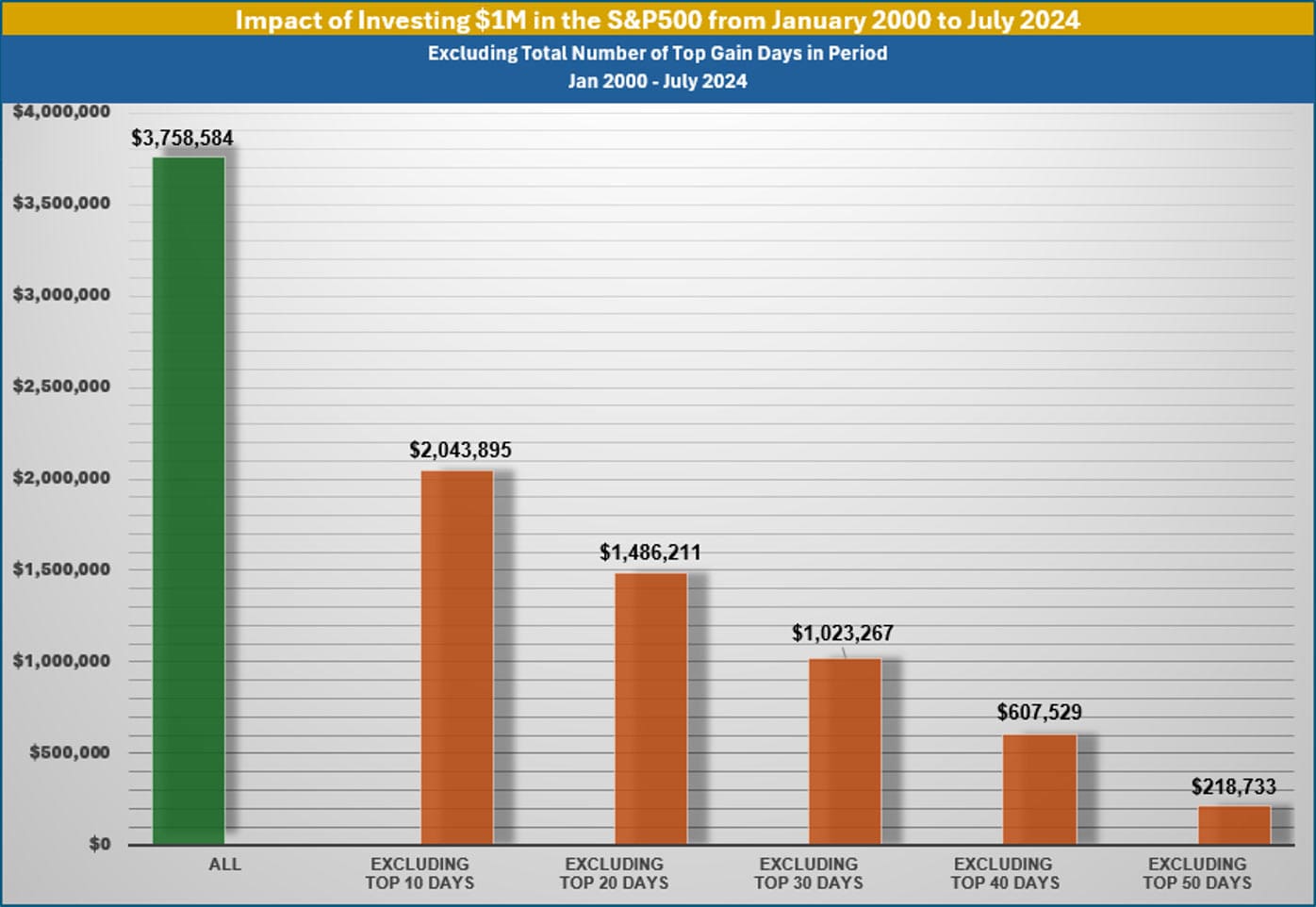

Many investors believe they can outsmart the market by timing their entries and exits perfectly. The problem? Even professional investors with decades of experience struggle to do this consistently. The market’s best days often follow its worst days, and missing even a handful of these best days can significantly hurt long-term returns (see Exhibit 1).

Exhibit 1 (Source: Factset, S&P)

For example, an investor who stayed fully invested in the S&P 500 from 2000 to 2024 would have earned an annualized return of around 6%. However, missing just the 10 best days during that period would have cut that return nearly in half. Instead of attempting to time the market, disciplined investors stick to their plan and ride out volatility.

3. Chasing Performance

Investors frequently chase past performance, believing that recent winners will continue to outperform. This often leads them to invest in assets that are already overvalued, only to experience disappointment when the hot streak ends.

For example, many investors rushed into technology stocks during the late 1990s tech bubble, only to suffer heavy losses when the bubble burst. Similarly, in the early 2020s, speculative assets like meme stocks and cryptocurrencies soared, attracting a flood of investors–many of whom later experienced significant declines. Carefully spreading risk via a diversified, disciplined approach may prevent such costly mistakes.

4. Lack of Patience

Investing is a long-term endeavor, but many investors lack the patience required for successful outcomes. When an investment doesn’t deliver immediate results, impatience can lead to premature selling.

Consider the case of Amazon. In its early years, Amazon’s stock was highly volatile, and it took more than a decade to become consistently profitable. Many investors who lacked patience sold their shares too soon, missing out on one of the greatest growth stories in stock market history. The lesson? Long-term investing rewards patience.

5. Overtrading

Frequent buying and selling of investments – also known as overtrading – can erode returns through excessive transaction costs and taxes. Many investors mistakenly believe that staying active in the market equates to better performance, when in reality, high turnover often leads to worse outcomes.

For instance, a study by DALBAR1 found that the average investor underperforms the broader market largely due to excessive trading. The costs associated with frequent buying and selling – such as brokerage fees, bid-ask spreads, and short-term capital gains taxes – eat into returns. A disciplined, low-turnover strategy is typically more effective.

6. Lack of Discipline

Investors who lack discipline often abandon their financial plans when faced with short-term market noise. A solid financial plan should include clear asset allocation guidelines, risk management strategies, and periodic rebalancing. However, many investors veer off course when markets become volatile or when they’re tempted by short-term fads.

Take, for example, investors who deviated from their long-term plans during the COVID-19 market crash in early 2020. Those who panicked and sold at the bottom locked in losses, while those who remained disciplined and rebalanced their portfolios saw substantial gains as markets rebounded.

7. Failing to Seek Professional Guidance

Investors who work with financial advisors benefit from objective perspectives and disciplined decision-making. Advisors help clients navigate volatile markets, avoid behavioral pitfalls, and stay focused on their long-term goals.

For instance, a financial advisor can help an investor stay the course during a market downturn by providing historical context and reinforcing the importance of sticking to a long-term strategy. Advisors also assist with tax-efficient investing, estate planning, and risk management – areas where individual investors often make costly mistakes.

How to Avoid Behavioral Pitfalls

To ensure that a financial plan is effective, investors should implement strategies to mitigate behavioral biases. Some key approaches include:

- Automating Contributions: Dollar-cost averaging ensures that investments are made consistently, regardless of market fluctuations, reducing the temptation to time the market.

- Setting Clear Rules: Establishing guidelines for asset allocation, rebalancing, and risk management can prevent impulsive decision-making.

- Practicing Mindfulness: Recognizing emotional reactions to market movements can help investors pause and reflect before making financial decisions.

- Working with an Advisor: A financial professional can act as a buffer against emotionally driven mistakes and keep an investor focused on long-term goals.

Conclusion

A financial plan is only as good as the behavior of the investor following it. Without discipline, even the most well-designed strategy will fail to produce the desired results. Investors must recognize and combat behavioral biases, stay committed to their plan, and seek professional guidance when needed. By doing so, they can navigate market volatility, avoid costly mistakes, and achieve lasting financial success.

References

1. DALBAR Quantitative Analysis of Investor Behavior (QAIB), 2024

Related Articles

How Portfolio Overlap Could Be Putting Your Investments at Risk!

Financial Planning,

Investment Principles,

Personal Finance,

Top Investor Mistakes,

December 10, 2024

Investor Behavior

Behavior,

Investment Principles,

November 1, 2023

Trifecta: Three Negative Influences on Investor Behavior

Behavior,

Investment Principles,

January 30, 2025