By Indexopedia Research Team | January 8, 2025 | In

Investment fees and costs can have a profound impact on the long-term performance of a portfolio. While many investors focus on visible fees like the standard advisor fee or mutual fund expense ratios, there are numerous less intuitive costs that can erode returns over time. These hidden fees and market dynamics, such as investor herding, bond fund pricing disadvantages, and inefficiencies in fund structures, can gradually diminish the compounding of your portfolio. Advisors typically advertise fees in the 0.5% to 1.5% range, but many investors don’t realize that this fee does not include other hidden costs that impact investor results.

The Dangers of Small Investor Herding

One hidden cost of investing comes from small investor herding, particularly during market downturns. When markets are falling, individual investors often panic, triggering a wave of redemptions from pooled mutual funds. This “run for the exits” mentality forces fund managers to sell assets at depressed prices to meet these redemption demands, which not only reduces the value of the fund for those who remain, but also locks in losses for investors who panic. When this happens within equity funds, trading is increased, driving up trading costs and the internal trade spreads.

For example, during the financial crisis of 2008, many retail investors rushed to redeem their shares from equity mutual funds, causing widespread selling. Fund managers, compelled to meet these redemption requests, were forced to liquidate high-quality stocks at bargain prices. This created a vicious cycle, with more selling pressure driving the market down further. The result was that many investors who cashed out locked in substantial losses, while those who stayed in the fund were subject to the higher costs, significant losses, and potential pass-through taxes (if held in a non-qualified account).

In contrast, investors who maintain a long-term view and resist the herd mentality avoid forcing these fire-sale scenarios. Investors who remained in the fund after the 2008 crash saw substantial gains during the recovery, but still were punished for the bad behavior of others in the fund. This is one of the many reasons our team at Linden Thomas & Co. set out years ago to build an institutional index for affluent investors.

Advisor Fees

Advisors typically advertise fees in the range of 0.5% to 1.5% but many investors don’t realize this fee is simply for their “advice” and does not cover all the other expenses and costs associated with ownership in a pooled fund. But if the advisor is simply placing money in third-party pooled mutual funds or ETFs then the investor will be exposed to multiple layers of hidden expenses and inefficiencies.

Expense Ratios and 12b-1 Fees

The expense ratio of a fund includes administrative costs, management fees, and marketing costs (often referred to as 12b-1 fees). While the management fee compensates the portfolio manager, 12b-1 fees are used to market the fund, which does nothing to benefit the investor directly. For example, if a fund has an expense ratio of 1.5%, it means that 1.5% of the fund’s assets are deducted annually, regardless of the performance. Over time, high expense ratios can erode returns, especially in a low-return environment.

Bond Fund Pricing Disadvantages

While many investors assume bond funds are less expensive, they often aren’t. When investors put money in a bond fund, they are essentially investing in a large pool of bonds bought prior to the investor’s entry into the fund. Not only do they not own or control the bonds directly, but the pool of bonds may have very low net-yields due to the coupons and maturity dates. This translates to low returns. When you add in the annual expense ratio, trading costs, and the investment advisor costs, what’s left often isn’t enough to meet the investor’s needs. Another challenge of pooled ownership is being subject to the behavior of others in the fund. When the markets move down, you’re impacted by other investors’ bad behavior. Why? Because the fund is forced to sell bonds to create the liquidity needed for investor redemptions. Cost, ownership, and control are all important factors in any efficient portfolio.

Sales Fees and Trading Costs

Sales fees, often referred to as loads, are charged when you buy or sell a mutual fund. These fees can range from 1% to 5% of your investment and are typically paid to the advisor or broker who sells you the product. Over time, these seemingly small fees can take a big bite out of your overall returns, especially when you consider the effect of compounding. Additionally, frequent trading within a portfolio incurs transaction costs, which can add up over time. Even low-cost ETFs and mutual funds can have internal trading costs, which may not be fully transparent to the investor.

Bid-Ask Spreads

When buying or selling stocks or bonds, investors often pay a small difference between the price they buy at (ask) and the price they sell at (bid). While this difference may seem minimal for individual transactions, frequent trading or investing in illiquid securities can cause bid-ask spreads to accumulate and impact long-term returns.

Cash Drag

Additionally, cash drag, the impact of holding uninvested cash within a portfolio, can reduce growth potential. If a significant portion of a portfolio is sitting in cash during a rising market, the investor misses out on potential gains, further impacting compounding.

Stock Delistings

Another potential drag on performance comes from stock delistings. When a company is delisted, whether due to poor performance or regulatory issues, shareholders often see a significant decline in the value of their investment. Additionally, mutual funds and ETFs that hold such stocks may experience sudden drops in value, which can affect fund performance.

Phantom Tax Liabilities

Phantom tax liabilities arise when mutual funds distribute capital gains to shareholders, even if the investor didn’t sell any shares. These gains are triggered by the fund’s internal trading, meaning investors could owe taxes on gains they didn’t personally realize. Over time, these unexpected tax liabilities can add to the overall cost of investing in funds, particularly for high-net-worth investors in higher tax brackets.

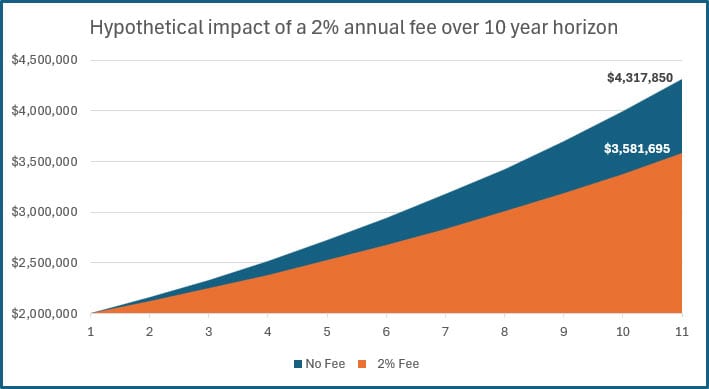

The Importance of Managing Costs

Over time, even small fees and inefficiencies compound, reducing the overall growth of a portfolio. For example, consider a $2,000,000 portfolio with an average annual return of 8%. Without any fees, this portfolio would grow to approximately $4.3 million over ten years. However, if the investor pays a total of 2% per year in various fees (advisor, expense ratios, and trading costs), the portfolio will grow to only about $3.6 million, a difference of approximately $700,000 over the decade due to fees alone!

Conclusion: Mind the Hidden Costs

While visible costs like advisor fees and sales loads are important, the less obvious costs, such as small investor herding, lower bond yields, and phantom tax liabilities, can significantly erode long-term returns. Being aware of these hidden costs and taking steps to minimize them can have a profound impact on your overall investment results, helping to ensure that more of your money stays invested and working for you, rather than being siphoned off by fees and inefficiencies.

Carefully selecting investments with low expense ratios, minimizing trading, and avoiding herd mentality can help preserve your portfolio’s growth potential. Investing in direct ownership of bonds or high-quality stocks may reduce hidden costs, allowing for better compounding over time, which is critical to long-term wealth accumulation.

Related Articles

Do I need to pay an investment advisor a fee to buy index funds?

Index Investing,

Top Index FAQs,

Types of Indexes,

September 30, 2024

What is the real cost of index funds?

Index Investing,

Top Index FAQs,

Types of Indexes,

October 21, 2024

What are Advisor Fees?

Index Investing,

Personal Finance,

Top Index FAQs,

Top Personal Finance FAQs,

October 23, 2023