By Indexopedia Research Team | January 8, 2025 | In

Investing successfully isn’t just about picking the right stocks and bonds. It’s about ensuring your portfolio is structured to minimize inefficiencies and maximize results. An efficient portfolio – one tailored with precision to spread risk and eliminate hidden costs – can achieve what an inefficient portfolio often fails to: sustainable, long-term results.

Before exploring the critical impacts of retail portfolio inefficiencies, let’s first understand what makes a portfolio inefficient. Inefficiencies can stem from:

- Hidden Costs: High hidden fees within mutual funds, ETFs, and other investment products add up. They come in the form of expense ratios and internal trading fees. Most funds make it easy to see the expense ratio, but the trading fees are an added cost that can further reduce the return to the investor.

- High Advisor Fees: Many investors pay an advisor 1% or more to manage their portfolio. The question is, are you getting your money’s worth? The advisor is quite often outsourcing the money management responsibilities to a third-party such as a mutual fund company or ETF. Many of the industry’s investment advisors promote one fee for all services, but seldom discuss the hidden fees for the management of the product they sell.

- Low-Quality Holdings: A market cap approach that invests in companies with weak fundamentals, excessive leverage, or poor earnings consistency.

- Pooled Ownership: Mutual funds and other pooled investments lack transparency and may force liquidation during market stress.

- Phantom Taxes: Taxable events triggered by fund activity, even if the investor hasn’t sold their holdings.

- Portfolio Overlap: Portfolio overlap occurs when multiple investment funds or vehicles share the same holdings, leading investors to unknowingly concentrate on only a few companies. This happens when investors or advisors invest in a multitude of mutual funds with the same holdings because they don’t have the software to view portfolio overlap.

- Small Investor Herding: Investor redemptions during downturns force managers to sell at inopportune times, locking in losses for shareholders. When mutual funds or ETFs have a large exodus of small investors, this triggers trading fees and taxes. Internal trade spreads can also be wider during times of heightened volatility, negatively impacting investors who remain in the fund.

- Pricing Disadvantages: Retail funds, particularly bond funds, often face inefficiencies, especially during volatility, as managers sell at losses to meet redemptions, leaving investors with overpriced bonds with minimal yields. Bond funds can also carry low yield-to-maturity or yield-to-call because the bonds were bought in large denominations prior to investors entering the fund. Direct bond ownership provides control, transparency, and the ability to hold bonds to maturity, avoiding reinvestment risk and protecting against rising rates.

Below, we analyze how these inefficiencies manifest across four critical areas: upside capture, downside capture, long-term compounding, and time to recovery.

1. Upside Capture: Harnessing Growth Opportunities

An efficient portfolio captures more of the market’s upside because it avoids structural and behavioral inefficiencies that limit returns. Conversely, an inefficient portfolio, one laden with overlap, low-quality holdings, and indirect ownership, fails to fully capitalize on market gains.

Example: A common inefficiency arises in pooled bond funds. Suppose a bond fund’s manager sells securities prematurely to meet redemptions (a phenomenon known as small investor herding), forcing investors to incur trading fees and miss out on potential price appreciation when rates fall. By contrast, an efficient portfolio with bonds owned directly allows investors to hold those securities until maturity, locking in gains while maintaining control over the timing of reinvestments.

Hypothetical Data:

- Inefficient Portfolio: A pooled bond fund may have a total cost to the investor between 3 and 4%, when considering all of the costs including the advisor fee, expense ratios, internal trading costs, and trade spreads.

- Efficient Portfolio: A portfolio of directly owned bonds earns 5% annually, reflecting better upside capture through lower costs and strategic management.

Over 10 years, a $2 million efficient portfolio grows by $628,894, while the inefficient portfolio lags behind with $583,200, a $45,694 difference simply due to just this one structural inefficiency.

2. Downside Capture: Managing Losses During Market Stress

Inefficiencies in a portfolio amplify losses during market downturns. Hidden costs, low-quality holdings, and pooled ownership all increase vulnerability to declines. An efficient portfolio, by contrast, focuses on quality, diversification, and strategic cost control to minimize losses.

Example: During the Great Financial Crisis of 2008-2009, inefficient portfolios heavily invested in high-risk, leveraged financial products or concentrated in underperforming sectors suffered devastating losses. Bond funds tied to subprime mortgage-backed securities and financial stocks were hit especially hard. For many investors, losses were compounded by fees and the forced selling of assets (small investor herding).

Efficient portfolios, emphasizing diversification and high quality, fared better. Direct exposure to government bonds, high-quality blue-chip stocks, and defensive sectors like consumer staples shielded investors from the worst impacts and allowed quicker recovery as markets rebounded.

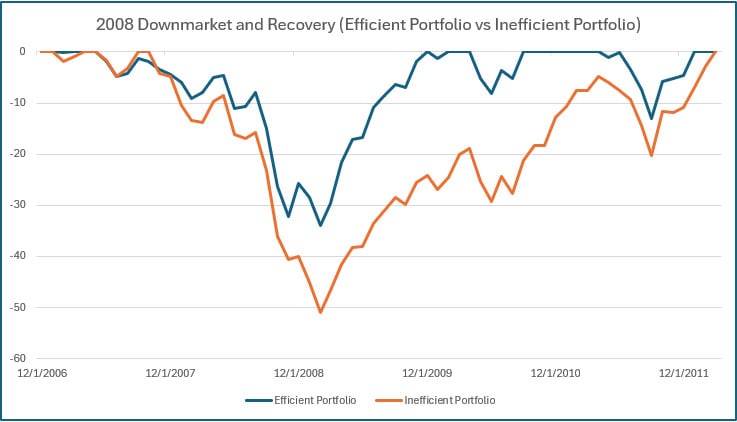

Exhibit 1: A comparison of an efficient Linden Thomas blended fund versus the broader equity market (S&P 500 Index).

Exhibit 1 (source: Zephyr)

3. Recovery Time After a Down Market: Speed Matters

An inefficient portfolio often takes longer to recover after a market downturn due to excess fees, poor-quality holdings, and indirect ownership. In contrast, efficient portfolios, with a focus on quality investments and cost-effective structures, recover much faster. A quicker recovery allows the resumption of compounding returns, significantly enhancing long-term results.

Example: An inefficient portfolio concentrated in high-volatility tech stocks during the dot-com crash of the early 2000s took nearly a decade to recover its value. By contrast, diversified portfolios with exposure to defensive sectors like healthcare and consumer staples recovered in just a few years.

Hypothetical Data:

- Inefficient Portfolio: After a 30% loss, it takes 7 years to recover due to high fees and concentrated risks.

- Efficient Portfolio: Suffers the same 30% loss but recovers in 4 years due to diversification and lower costs.

The longer a portfolio remains underwater, the more difficult it becomes to regain lost ground. Efficient portfolios resume compounding sooner, leading to significantly better long-term results.

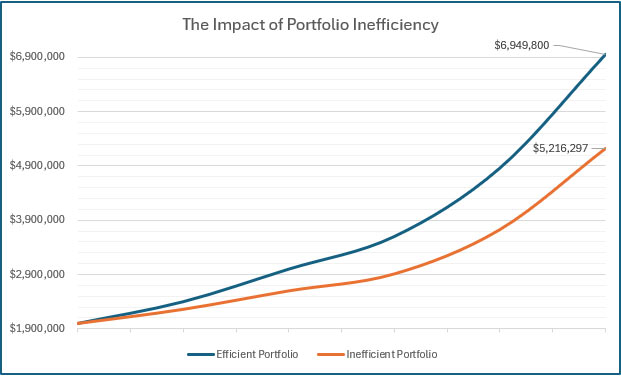

4. Long-Term Compounding: The Power of Efficient Growth

Portfolio inefficiencies hinder the exponential growth potential of compounding. Hidden costs, phantom taxes, and low-quality holdings quietly erode returns, reducing the ability of an investor’s wealth to grow over time. An efficient portfolio, free from these drags, maximizes compounding potential.

Theoretical Example: Consider two portfolios with identical initial investments and market conditions but different expense ratios. Over 20 years, the drag from hidden fees and other inefficiencies can dramatically widen the gap between an efficient and an inefficient portfolio.

Hypothetical Data:

- Inefficient Portfolio: 3.4% annual return.

- Efficient Portfolio: 5.6% annual return.

After 20 years, a $2 million investment grows to:

- Inefficient Portfolio: $5.22 million.

- Efficient Portfolio: $6.95 million.

That’s a difference of nearly $1.7 million due solely to cost management.

Exhibit 2 (source: Zephyr)

Conclusion: Efficiency Isn’t Just About Costs – It’s About Outcomes!

While market performance is often unpredictable, portfolio efficiency is entirely within an investor’s control. By eliminating inefficiencies such as overlap, low-quality holdings, indirect ownership, phantom taxes, hidden costs, high advisor fees, and pricing disadvantages affluent investors can build portfolios that not only capture more upside but also mitigate losses, maximize long-term growth, and recover more quickly from market downturns.

At Linden Thomas & Co., we specialize in constructing efficient portfolios tailored to our clients’ unique goals and risk tolerances. The difference between an efficient and inefficient portfolio isn’t just a matter of percentages; it’s a matter of achieving financial objectives faster and with greater certainty. By peeling back the layers of inefficiency, you can reveal a portfolio that’s aligned with your long-term vision for wealth and legacy.

Related Articles

How Quality of the Portfolio Impacts Down Market Recovery and Compounding

Investment Principles,

Top Investment Principles FAQs,

January 15, 2025

What Does Your Portfolio and an Onion Have in Common?

Financial Planning,

Personal Finance,

October 1, 2024

Building a portfolio with a correction in mind vs timing the correction

Investment Principles,

Markets,

Portfolio Considerations,

October 1, 2024