Why Long-Term Investors Should Focus on Ownership, Not Short-Term Portfolio Fluctuations

In a world built around constant noise and real-time results, it’s no surprise that many investors struggle to achieve long-term success. We live in an era where portfolio values are available at the click of a button, refreshed second by second, inviting constant judgment and reaction. Unfortunately, this easy access often encourages short-term thinking—exactly the kind of thinking that undermines positive long-term results. Not because markets fail them—but because behavior does.

Years ago, investing looked very different. Investors owned individual stocks and bonds directly. Share certificates were mailed. Account values were updated infrequently. When markets declined, phones rang—not with panic, but with opportunity. Investors wanted to add shares at lower prices. Bad news wasn’t feared; it was welcomed.

Today, the opposite is often true. As access to real-time portfolio values has increased, patience has declined. Temporary price movements now feel permanent, and the natural ups and downs of the market are mistaken for crises. The result is a shift in focus—from ownership to value.

That shift matters.

Accumulating Shares Is How Wealth Is Built

Real wealth is built through the accumulation of high-quality assets over time—shares of stocks and bonds that generate earnings, dividends, and interest. The day-to-day value of those assets matters far less than how many shares you own and what those shares produce over a full market cycle, which is often 10-20 years.

When high-quality companies experience price declines, the underlying business often hasn’t changed. People still drink Coca-Cola. Electricity is still consumed. Goods and services are still produced. A lower stock price simply means your claim on those future earnings can be increased more cheaply.

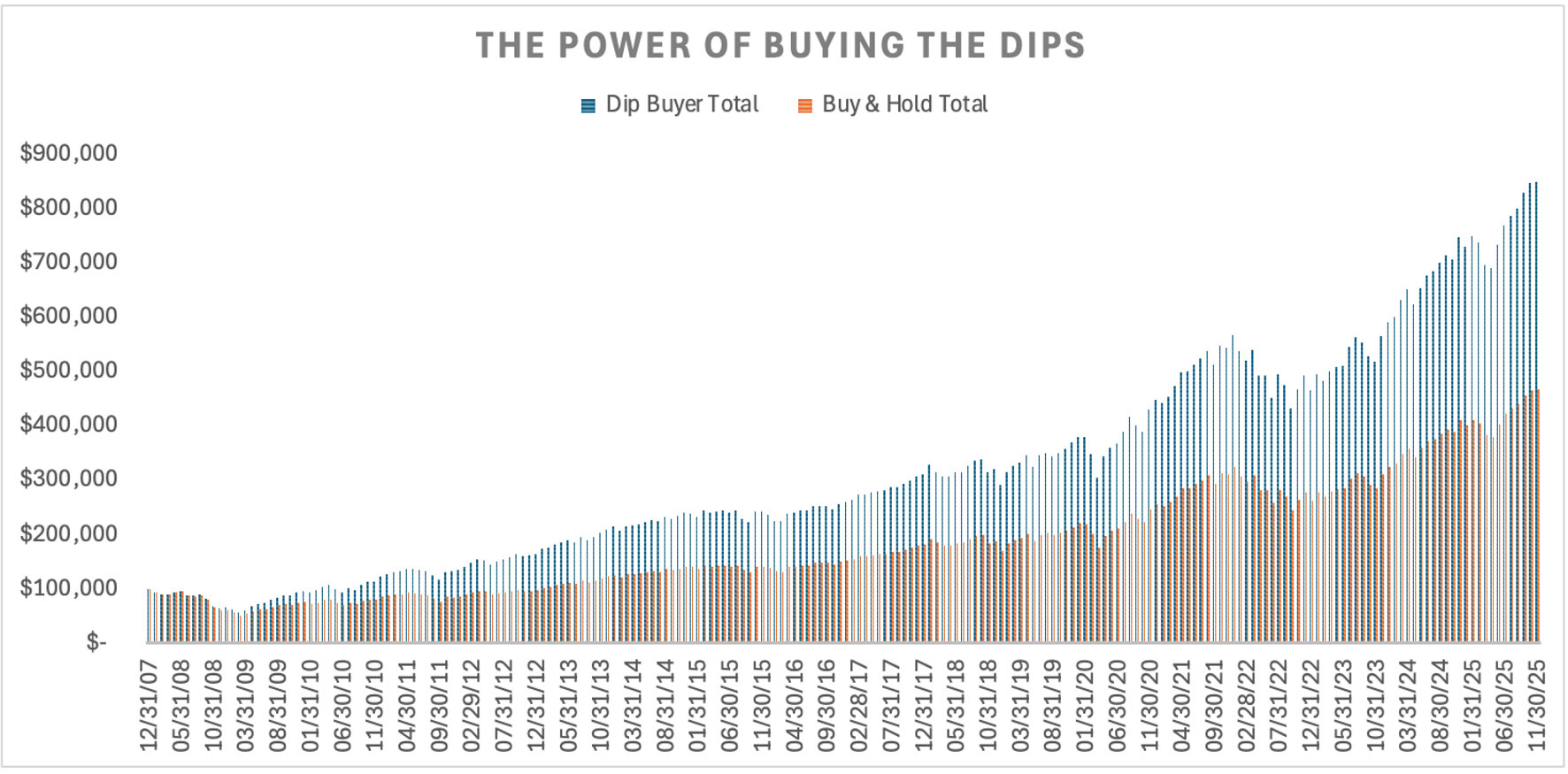

In the example below, two investors both started with a $100,000 account, but anytime the market was down more than 10%, they added $1,000 each month until it recovered. From January 2008 through November 2025, the “Buy the Dip” investor added a total of $83,000, but their portfolio grew to over $848,000. The “Buy & Hold” investor who did nothing saw their portfolio grow to just over $466,000.

*Source: Factset using S&P 500 monthly returns.

The same logic applies to bonds. When interest rates rise and bond prices fall, many investors focus on the temporary decline in market value and miss the more important reality: both new and old bonds are now available at higher yields. Income improves. Future cash flows increase. For long-term investors, this is not a problem—it’s an opportunity.

Bad news, in other words, is often good news for disciplined investors.

The Value Trap: Watching the Scoreboard Too Closely

One of the greatest behavioral challenges investors face is the constant monitoring of portfolio value. Watching daily fluctuations can distort decision-making and encourage exactly the wrong behavior—selling when prices are low and buying when prices are high.

A wise investor once put it this way: watching your portfolio value every day is like staring at your lawn waiting for fertilizer to work. Growth doesn’t happen because you watch—it happens because you plant seeds, water consistently, and give it time.

Investing works the same way.

Markets go up. Markets go down. That’s not a flaw—it’s the mechanism that creates opportunity. The investors who succeed over time are the ones who resist the urge to react to every fluctuation and instead focus on adding shares when prices are lower and letting compounding do the rest.

Unfortunately, fear and greed tend to reverse that logic.

When markets decline, fear convinces investors to stop buying—or worse, to sell. When markets rise, confidence returns and investors rush in, often paying higher prices for the same assets they avoided months earlier. This cycle of selling low and buying high is one of the most common—and costly—mistakes investors make.

A Simple Example: Value Down, Income Intact

Consider a straightforward bond example.

An investor owns $100,000 in individual bonds paying a 6% coupon, producing $6,000 in annual interest. If interest rates rise and bond prices fall by 10%, the market value drops to $90,000. Many investors focus on that decline and feel poorer.

But the reality hasn’t changed. The bonds are still paying $6,000 per year. The income is intact. And new bonds are now available at higher yields.

Because the cash flow on the current bonds has remained the same and bonds are now cheaper it increases the ability to buy bonds with better prices and higher yields with the income that the current bonds pay. Essentially buying power increases.

The value is temporary. The cash flow—and the long-term opportunity—is real.

The same principle applies to equities. If you invest $25,000 per year and the first $50,000 you invested is temporarily worth $40,000, does that invalidate the plan? Of course not. If anything, future contributions now buy more shares at lower prices—enhancing long-term results.

Down markets don’t stop compounding. Poor behavior does.

The Difference Between Wise and Poor Investor Behavior

Over full market cycles, all investors experience the same environments—booms, busts, recoveries, and uncertainty. What separates outcomes is behavior.

Wise investor behavior:

Individual ownership + down markets = opportunity to buy and accumulate more shares at a discount.

Poor investor behavior:

Pooled or fund ownership based on value + down markets = fear, inaction, or liquidation (keep in mind owning shares directly gives one control of the assets while mutual fund ownership is pooled with other investors who may be selling fund shares and forcing asset liquidation at depressed prices).

The math doesn’t change. The markets don’t change. The difference is how investors respond.

Long-term success requires doing what often feels uncomfortable and unpopular—adding to high-quality assets when prices are lower, staying disciplined when headlines are loud, and focusing on ownership rather than short-term value.

The Journey Matters More Than the Moment

Building wealth is not about winning a single year or avoiding every decline. It’s about staying invested long enough for compounding to work—through good markets and bad.

Temporary declines are not failures; they are part of the process. They create the conditions for future returns. Investors who understand this don’t fear volatility—they use it.

The journey matters more than the destination, because the destination is shaped by how you behave along the way.

Focus on shares, not value. Ownership, not headlines. Discipline, not emotion.

That’s how long-term results are achieved.