Two properties sell for the same price. One owner walks away largely tax-free. The other faces a six-figure tax bill.

What’s the difference?

Of course, there are many variables, but most of the time, it comes down to how the property was used. The IRS treats primary residences and investment properties very differently, and those distinctions ripple through capital gains taxes, exclusions, depreciation, and available deductions.

Before listing a property or agreeing to a deal, it’s worth understanding how the sale will be taxed and what steps can help manage the impact.

Primary Residence vs. Investment Property

From a tax perspective, how a property is classified can mean the difference between walking away largely tax-free or owing a meaningful portion of the sale proceeds to the IRS.

That’s because primary residences may qualify for one of the most generous tax benefits available to individual taxpayers, while investment properties generally do not.

Under current rules, homeowners can exclude up to $250,000 of capital gains from the sale of a primary residence if filing individually, or up to $500,000 for married couples filing jointly. Investment properties, on the other hand, are typically subject to capital gains taxes (and, in many cases, depreciation recapture) with no comparable exclusion.

What Qualifies as a Primary Residence?

A primary residence is the home where you live most of the time. To qualify for the capital gains exclusion, you must meet both:

- Ownership test: You owned the home for at least two of the past five years.

- Use test: You lived in the home as your primary residence for at least two of the past five years.

If those criteria are met, a portion (or all) of the gain may be excluded from federal capital gains taxes.

What Qualifies as an Investment Property?

An investment property is real estate held primarily to generate income or appreciation, including:

- Rental properties

- Commercial real estate

- Second homes or vacation properties not used as a primary residence

- Properties owned through pass-through entities such as LLCs or partnerships

Investment properties do not qualify for the primary residence exclusion. Instead, gains are taxed based on holding period and income level, and prior depreciation deductions are subject to recapture.

Gray Areas

Some properties don’t fit neatly into one category:

- A primary residence later converted into a rental

- A vacation home used personally and rented part-time

- A property occupied for part of the ownership period

In these instances, gains may be prorated or partially taxable, making timing and planning quite important.

Selling a Primary Residence: Tax Treatment

In many cases, especially for homeowners whose properties haven’t appreciated significantly, the exclusion eliminates federal capital gains taxes. For example, a married couple who sells a home with a $400,000 gain may owe no federal capital gains tax at all if they meet the eligibility requirements.

In higher-priced markets or long-held properties, gains can exceed the exclusion limits. As a result, the portion above the exclusion is subject to capital gains tax — likely at long-term capital gains rates if the home was held for more than one year.

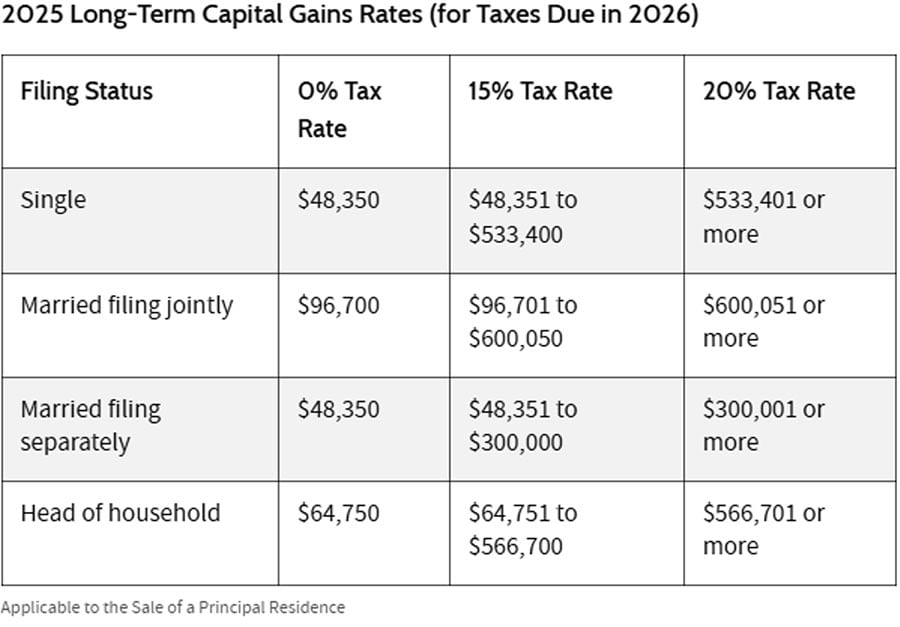

For example, if a married couple realizes a $650,000 gain on a house they’ve owned for 20 years, $500,000 may be excluded, but the remaining $150,000 would generally be taxable. Assuming they file jointly, a 15% tax rate would apply.

Partial Exclusions

Even if you don’t meet the full two-year ownership and use requirements, you may still qualify for a partial exclusion in certain circumstances, including a job relocation, health-related moves, or other IRS-approved unforeseen events.

If so, the exclusion is prorated based on the amount of time you lived in the home, which can still substantially reduce the tax impact.

Selling an Investment Property: Tax Treatment

If you sell an investment property, the difference between the sale price and your adjusted cost basis is considered a capital gain.

Short-term gains apply if the property was held for one year or less and are taxed at ordinary income rates.

Long-term gains apply if the property was held for more than one year and are taxed at long-term capital gains rates.

Most long-term real estate investors fall into the latter category, but the tax rate ultimately depends on income level and filing status.

Depreciation Recapture

During ownership, rental property owners are typically allowed to depreciate the property each year, reducing taxable income. While this provides valuable tax relief over time, the IRS requires that portion of the gain to be “recaptured” at sale.

In practical terms:

- The amount of depreciation taken (or that could have been taken) is taxed separately

- Depreciation recapture is generally taxed at a maximum federal rate of 25%

- This applies even if you didn’t actively claim the depreciation deductions

For many sellers, depreciation recapture accounts for a sizable portion of the total tax bill.

Net Investment Income Tax (NIIT)

Depending on your income level, an additional 3.8% Net Investment Income Tax may apply to investment property gains. This surtax typically affects higher-income taxpayers and applies on top of capital gains and depreciation recapture, further increasing the effective tax rate on the sale.

State and Local Taxes

Federal taxes are only part of the picture. Many states impose their own (usually) flat tax rate on capital gains, and in some cases, additional surtaxes or transfer taxes may apply.

The combined impact of federal, state, and local taxes can materially reduce net sale proceeds if not planned for in advance.

Example

Let’s assume an investor purchases a rental property for $495,000 and later invests $55,000 in capital improvements, bringing the total cost basis to $550,000. Over twelve years of ownership, the investor claims $216,000 in depreciation ($18,000 annually).

After accounting for depreciation, the adjusted cost basis is $334,000.

Now suppose the property is sold for $700,000.

Here’s how the gain is calculated:

Sale price: $700,000

Adjusted cost basis: $334,000

Total gain: $366,000

That gain is then taxed as follows:

- Depreciation recapture: The portion of the gain equal to depreciation taken ($216,000) is taxed at a maximum federal rate of 25%, resulting in $54,000 of tax.

- Long-term capital gains: The remaining $150,000 is taxed at long-term capital gains rates (assume 20%), resulting in $30,000 of tax.

- NIIT: An additional 3.8% surtax applies to the entire gain, adding $13,908.

Estimated tax liability: $97,908, before any state or local taxes.

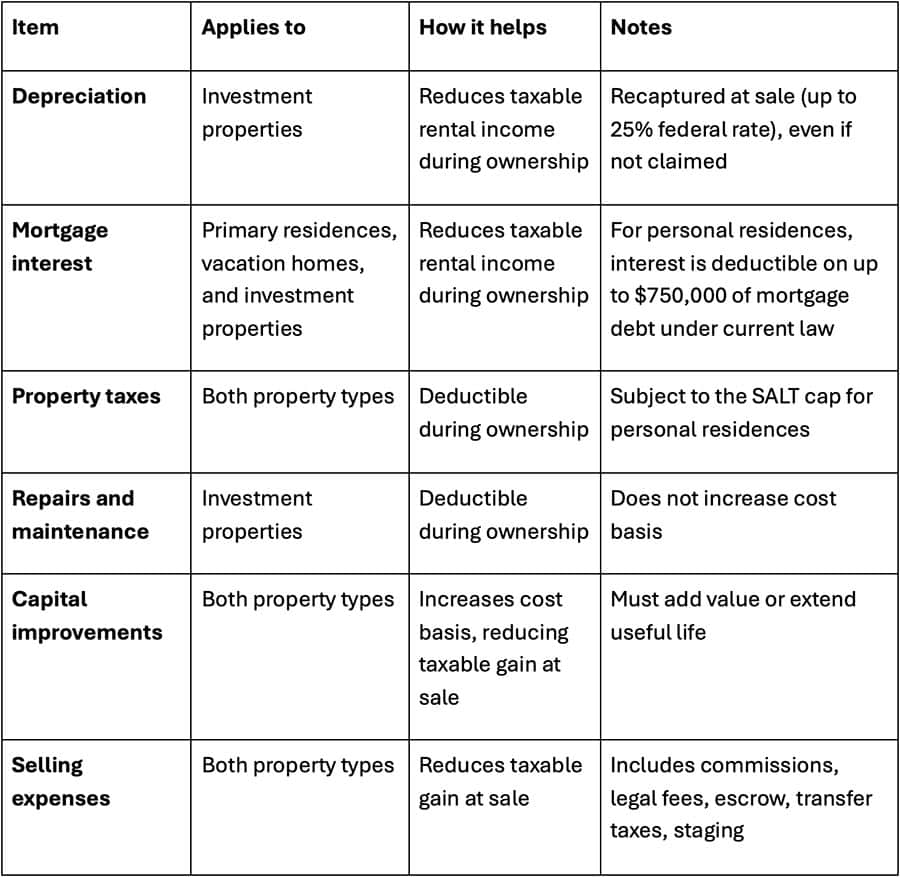

Adjusting the Taxable Gain

As you’d expect, your cost basis starts with what you paid for the property, including certain acquisition costs. Over time, that basis is adjusted upward or downward based on what you do with the property. The higher your adjusted basis, the lower your taxable gain at sale.

Your adjusted basis typically includes:

- Original purchase price

- Closing costs paid at acquisition (legal fees, title insurance, recording fees)

- Closing costs paid at acquisition (legal fees, title insurance, recording fees)

Capital improvements that add value or extend the property’s useful life

For investment properties, the adjusted basis is then reduced by depreciation deductions taken (or allowed to be taken) during ownership.

Improvements vs. Repairs

Capital improvements increase your basis and reduce taxable gain. That includes room additions, new roofs, HVAC systems, or major renovations.

On the other hand, repairs and maintenance (painting, fixing leaks, replacing broken fixtures) do not increase basis and are typically expensed in the year incurred.

That’s why it’s important to keep records of improvements over time, so you can document changes to your adjusted basis and materially affect the tax outcome when you sell.

Available Deductions and Basis Adjustments

While the sale of real estate itself doesn’t create many direct deductions, the period of ownership (and the transaction surrounding the sale) offers several opportunities to reduce taxable income or lower the taxable gain.

Key Takeaways

- If you’re selling real estate for a profit, the ensuing tax liability likely depends on whether the property is a primary residence or an investment property.

- Primary residences receive favorable treatment. Eligible homeowners can exclude up to $250,000 (single) or $500,000 (married filing jointly) of capital gains — a benefit that resets every two years.

- Investment properties face heavier tax exposure. Capital gains taxes, depreciation recapture, and potential surtaxes can significantly reduce net proceeds.

- Your taxable gain depends on the cost basis, improvements, and selling expenses which affect how much of the sale is actually taxed.

- Special situations can add complexity. Converted rentals, inherited properties, and mixed-use homes require extra planning to avoid tax surprises.

Related Articles

Real Estate Investment Trust

Index Investing,

Index Sectors,

Markets,

Top Markets FAQs,

November 3, 2023

The Impact of Taxes on Your Investment Portfolio: What Every Investor Needs to Know

Personal Finance,

Tax,

October 16, 2024

Tax Efficiency: Incorporating Qualified Opportunity Zones and 1031 Exchanges into an Affluent Investor’s Portfolio

Personal Finance,

March 18, 2025