By Indexopedia Research Team | August 14, 2024 | In

Owning a second home is a dream for many, evoking images of relaxing weekends by the lake, cozy winter getaways, or perhaps a stylish urban apartment in a favorite city. The allure of having a dedicated place to escape is undeniable. But before you dive into the world of second home ownership, it’s crucial to weigh the pros and cons carefully. The financial and logistical implications can be significant, and the dream of a second home can quickly turn into a financial burden if not approached with caution.

The Appeal of a Second Home

Let’s start with the appealing aspects. One of the biggest perceived advantages of buying a second home is the potential for investment growth. Real estate often appreciates in value over time, and a well-chosen property can potentially provide a return on investment. This is particularly true in popular vacation spots or growing urban areas where property values tend to increase more steadily. However, while most people consider the long term possibility they seldom consider the pain, cost, and lost to their personal savings (or worse) during a recession.

Ongoing Expenses and Maintenance

Another critical factor to consider is the ongoing expenses associated with owning a second home. These include property taxes, insurance, and maintenance costs, all of which can quickly add up. Unlike your primary residence, a second home often requires additional insurance coverage, particularly if it’s located in an area prone to natural disasters like hurricanes, earthquakes, or floods (as is the case for a home near the ocean).

Long-distance maintenance is not just about physical repairs and upkeep. It includes managing utility bills, arranging for lawn care, and handling unexpected issues that arise. The stress and inconvenience of coordinating these tasks from afar can quickly become overwhelming. Many second homeowners find themselves spending more time and money than they anticipated, leading to frustration and regret.

Another perceived benefit is the convenience of having a guaranteed vacation spot. Many people think owning a second home means they no longer need to worry about booking hotels or rentals during peak seasons, as your home-away-from-home is always available. This can lead to more spontaneous trips and extended stays, allowing you to fully enjoy your favorite destination without the hassle of planning and booking every detail. And yet again, when you actually do the math to calculate the cost of each night you may realize that this is a substantially more expensive way to vacation. For example, let’s say it costs $96,000 a year between mortgage, taxes, insurance, annual maintenance, and a whole host of other expenses most people don’t even think about when buying a second home. Now let’s assume that the happy second home buyer spends two weekends a month at the second home, which is consistent with typical usage rates. That’s a total of 48 nights (12 months x 2 nights x 2 times per month) or $2,000 a day, something we refer to as “Per Visit Cost” or PVC. This reflects the true cost of a single night’s sleep in your oasis. Not to mention that much of the time spent at the home is focused on fixing items or finding someone to do it for you. Consider that much of your time will likely be spent tracking down plumbers, electricians, the cable company, landscapers, exterminators, driveway sealers, and any of a host of other service providers and suddenly the dream of a relaxing vacation can quickly be replaced by an administrative and logistical nightmare.

The realization that it might cost upwards of $2,000 a day leads to another downside, and that’s travel guilt. Many second homeowners feel a sense of guilt if they don’t use their property as often as they planned. This guilt can turn the dream of a vacation home into a source of stress and anxiety. You might find yourself feeling obligated to spend every weekend, or vacation, at the second home even when you’d prefer to explore other destinations.

The realization that it might cost upwards of $2,000 a day leads to another downside, and that’s travel guilt. Many second homeowners feel a sense of guilt if they don’t use their property as often as they planned. This guilt can turn the dream of a vacation home into a source of stress and anxiety. You might find yourself feeling obligated to spend every weekend, or vacation, at the second home even when you’d prefer to explore other destinations.

The cash tied up in a second home also limits your financial flexibility. With a significant portion of your assets invested in real estate, you may find yourself with fewer funds available for other important purchases or investments. This can be particularly frustrating if unexpected expenses arise or if you want to take advantage of new investment opportunities.

Lawn care and general upkeep are additional responsibilities that can become burdensome over time. Unlike a primary residence, which you might maintain regularly, a second home often requires you to arrange for services remotely. This can lead to higher costs and less control over the quality of work performed.

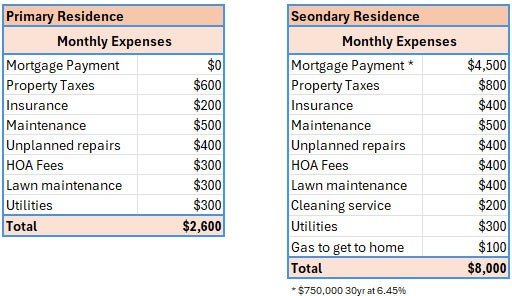

Travel time is another practical consideration. The effort required to get to your second home can diminish the enjoyment of owning it, especially if it’s located far from your primary residence. As you age, the appeal of long journeys may wane, making it more challenging to visit and enjoy your second home. See Exhibit 1 for a typical breakdown of monthly expenses.

A Cautionary Case Study

Take Barry, for example. Barry was a successful surgeon who had a portfolio valued at over $6 million. He decided to go ahead and purchase his dream home in the mountains for $1.5 million – financing half and paying $750,000 cash for the balance. He now owned a vacation home and a portfolio worth $5.25 million. But what Barry hadn’t included in his calculation were all the incidental expenses this second home would incur. Barry was shocked to learn that he needed an additional $8000 per month in order to cover the following expenses, most of which he had not even considered prior to purchasing the home:

Exhibit 1

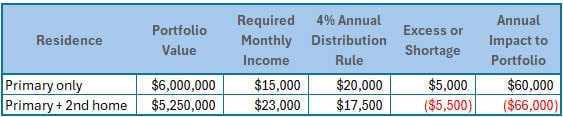

So now, instead of needing $15,000 a month, he needed $23,000. That translated into an annual income need of $276,000 ($23,000 x 12). And since the value of his portfolio had shrunk (due to the large cash withdrawal to pay for the house), his new income requirement represented an even higher percentage of his net worth. In fact, he was now depleting his nest egg at a rate of 5.3% per year. Prior to buying the second home, he was only taking a 3% distribution, a level of income easily covered by his portfolio and significantly below the recommended 4% distribution rate. Now that his required distribution rate had eclipsed 4% he had put his portfolio, as well as his future standard of living, in jeopardy. In the table below, you can see that the second home created a $66,000 annual deficit (Exhibit 2), which required Barry to liquidate a commensurate portion of his portfolio to cover the shortfall. This was not sustainable and would eventually cause him, and his family, to experience financial disaster.

Exhibit 2

Staying at a nice hotel actually may have been a far more affordable option! If we assume that the average daily rate of a nice hotel is $500 per night then the second home was actually costing Barry an additional $1500 per day, even more if he spent only one weekend per month there. See Exhibit 3 below:

Exhibit 3

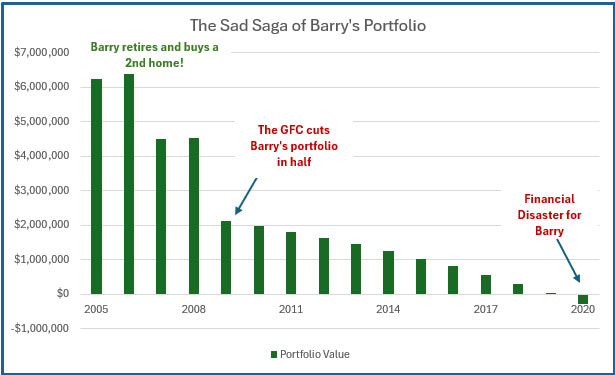

Now, what happens when the market falls? When the Great Financial Crisis hit in 2008, the stock market cratered, falling by nearly 50%, and Barry’s portfolio took a significant hit, falling to just under $2 million. This reduction in principal was devastating to his financial plan.

Barry was forced to withdraw over 15% of his portfolio that year, mainly to cover the incremental cost of owning the second home. Over time, this unsustainable rate of withdrawal would deplete his funds. Barry finally came to the realization that his second home had to go. However, the market downturn had spread to other sectors, including the real estate market. This meant that the value of his home had also fallen hard. And while the house sat idly on the market, Barry was unable to keep up with the required maintenance and, unfortunately, the house quickly fell into a state of disrepair. In the end, Barry wound up selling the house at a 30% loss relative to his initial purchase price. This story underscores the importance of carefully considering the financial implications before purchasing a second home.

This graph (Exhibit 4) highlights the disastrous impact Barry’s second home had on his portfolio and, ultimately, on his quality of life.

Exhibit 4

Conclusion

In conclusion, while the idea of owning a second home is undoubtedly appealing, it’s crucial to consider all the potential downsides. Barry’s story serves as a cautionary tale about the financial risks and responsibilities associated with a second home. The reduction in portfolio dollars, increased financial risk during market downturns, ongoing expenses, and the challenges of long-distance maintenance can all turn the dream of a second home into a significant burden.

Before making such a substantial investment, carefully weigh the pros and cons. Consider whether the benefits of having a dedicated vacation spot and potential rental income outweigh the financial and logistical challenges. It’s essential to have a clear understanding of the true costs and responsibilities involved. Sometimes, you might find that you don’t own the property; rather, the property owns you. By thoroughly evaluating these factors, you can make a more informed and financially sound decision about whether buying a second home is the right choice for you.

Related Articles

How Can I Develop Good Investment Behavior?

Personal Finance,

Top Personal Finance FAQs,

February 11, 2025

How Can I Teach my Kids How to Save and Invest Wisely?

Personal Finance,

Top Personal Finance FAQs,

November 7, 2024

The 4% Rule and Why Going Lower is Ideal

Financial Planning,

Personal Finance,

July 11, 2024