Not all wealth is visible. Some people wear it on their wrist or park it in the driveway. Others let it grow quietly in their portfolio. This is the story of two high earners–Mitchell and Lynette–who made nearly the same income, but took radically different paths when it came to spending and saving. The difference? One chased a lifestyle, the other built a future.

How Smart Spending and Long-Term Discipline Can Build True Financial Freedom

Meet Mitchell and Lynette. Both are high-income earners, pulling in approximately $600,000 per year during their later working years. On paper, they’re nearly identical — intelligent, successful, and earning in the top 1% of Americans. But their financial outcomes couldn’t be more different. What separates them isn’t luck or income, but behavior, particularly around spending and saving.

Let’s walk through their financial journeys to understand how discipline and frugality can dramatically influence long-term wealth.

Phase 1: Pre-Retirement – Earn, Spend, or Save?

During their working years, both Mitchell and Lynette earned roughly $600,000 annually. But that’s where the similarities ended.

Mitchell lived large. He leased a luxury car every three years, maintained a country club membership, owned a time-share in Aspen, and purchased a second lake house. His lifestyle cost him roughly $400,000 per year, leaving just $200,000 to save — less, once taxes were paid.

Lynette, on the other hand, lived modestly. She drove an older Camry, took modest vacations, and avoided unnecessary lifestyle inflation. She kept her spending to $200,000 a year, saving and investing the rest. Over time, those savings — compounded consistently — created a significant wealth gap.

Phase 2: Retirement

At age 65, both Mitchell and Lynette retired.

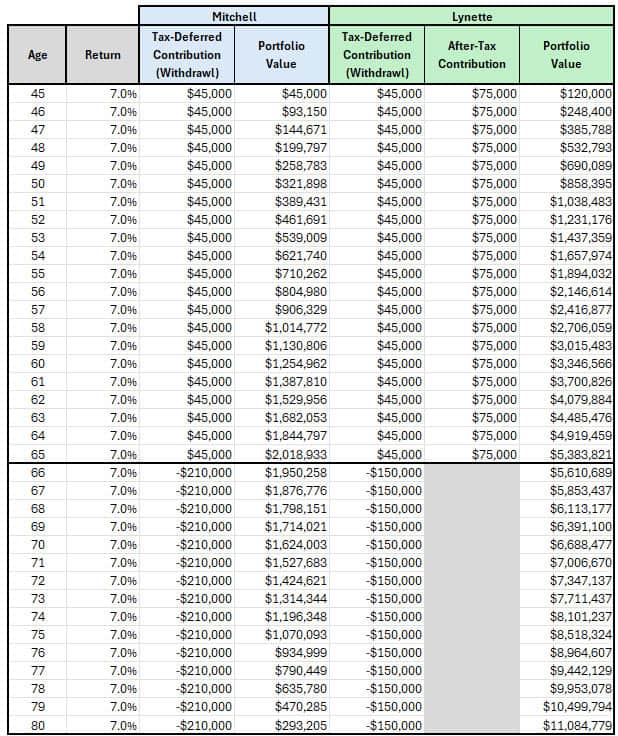

- Mitchell’s nest egg: $2.0 million

- Lynette’s nest egg: $5.3 million

Mitchell, still living rather large, decided to withdraw about 6% annually ($210,000), believing markets would continue to grow steadily. Lynette, by contrast, stuck to the 4% rule, withdrawing only $150,000 (well below the 4% threshold) – enough to maintain her modest lifestyle, but conservative enough to preserve her portfolio.

In the first year, both were comfortable. But markets soon turned.

Phase 3: Storm Clouds – The Dot-Com Bust and the Great Recession

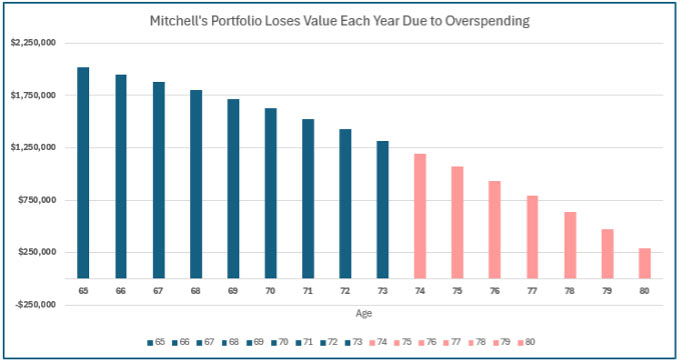

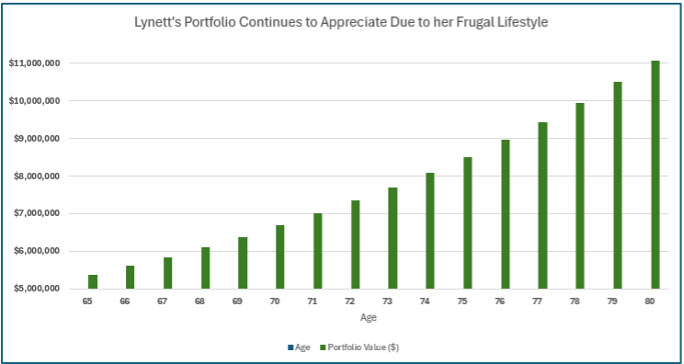

As you will see in Exhibit 1, Mitchell is slowly depleting principal whereas (as seen in Exhibit 2), Lynette’s portfolio continues to experience steady growth:

Exhibit 1

Exhibit 2

Dot-Com Crash (2001-2007):

In this hypothetical scenario, over seven years, the market posted an average annual return of -3%.

Mitchell continued withdrawing the same $210,000 per year, while also losing 3% to the market — a total portfolio drawdown of nearly 9% annually. Lynette, withdrawing less than 4%, saw total drawdowns closer to 6% annually.

- By 2008, Mitchell’s portfolio had dwindled to $1.4 million

- Lynette’s portfolio stood at around $7.3 million

Great Financial Crisis (2008-2012):

Markets once again delivered negative real returns, and Mitchell’s behavior didn’t change. He kept spending at pre-retirement levels, drawing the same $210,000 per year while his portfolio was already hemorrhaging.

By 2015:

- Mitchell was nearly broke. He had sold his second home, his prized power boat, and was effectively forced to rely on Social Security to get by.

- Lynette thrived. Though impacted by market volatility, her careful withdrawals and conservative approach allowed her portfolio to recover quickly.

Phase 4: Long-Term Outcomes – Wealth and Wisdom

By 2024:

- Mitchell is destitute. His once-luxurious lifestyle is a memory. He rents a small apartment and receives about $3,000/month in Social Security.

- Lynette is worth well over $10 million. She continues to live modestly, still driving her 2012 Toyota Camry. She donates generously, mentors younger investors, and enjoys complete financial freedom.

Two once wealthy investors experienced vastly different outcomes as a result of their investing behavior. It’s a sobering reminder: wealth is not what you earn, but what you keep.

The Real Meaning of “Frugal”

Frugality isn’t about deprivation. It’s about freedom — the ability to withstand life’s economic storms, stay invested through downturns, and enjoy peace of mind. Mitchell thought wealth was about what you could buy. Lynette understood that true wealth is about what you can keep, grow, and pass on.

Exhibit 3

Related Articles

Your Investments Can’t Save You: How Poor Financial Habits Destroy Retirement Dreams

Personal Finance,

March 28, 2025

The Surprising Truth About Owning a Second Home – Is It Worth It?

Investment Principles,

Personal Finance,

Top Investor Mistakes,

Top Personal Finance FAQs,

August 14, 2024

How Can I Teach my Kids How to Save and Invest Wisely?

Personal Finance,

Top Personal Finance FAQs,

November 7, 2024