Building wealth, particularly for retirement, is not a complex puzzle – at least not in theory. At its core, every successful wealth-building strategy relies on three fundamental pillars: saving money, achieving solid investment results, and allowing time for compounding to work its magic. However, while these principles are straightforward, investor behavior can often be the greatest threat to long-term success. No matter how well-constructed a financial plan may be, reckless spending, inadequate savings, and emotional investment decisions can sabotage even the most promising financial future.

Pillar One: Saving – The Foundation of Wealth

Every wealth-building journey begins with savings. Before an investor can take advantage of market growth, they must first accumulate capital. Yet, many people struggle with saving enough, often falling into the trap of spending more as their income rises or failing to prioritize long-term financial security.

Common Saving Pitfalls:

- Lifestyle Creep – As income increases, so do expenses. Many investors find themselves in a perpetual cycle of upgrading their homes, cars, and vacations, leaving little left for retirement savings.

- Low Savings Rates – Some individuals save the bare minimum required for their employer’s retirement plan match but fail to contribute enough to secure a comfortable future.

- Procrastination – Many believe they can “catch up later” on savings, failing to recognize the lost potential of compound interest over time.

The Fix:

A disciplined approach to saving is essential. Automating contributions to retirement and investment accounts ensures consistency, while maintaining a modest lifestyle allows for higher savings rates. The sooner savings begin, the more time there is for compounding to generate exponential growth.

Pillar Two: Investment Performance – Efficiency Matters

Saving alone is not enough – investment results play a crucial role in wealth accumulation. However, not all investment strategies are created equal. An efficient portfolio, focused on quality companies with proven earnings power, structured to minimize hidden fees, is far more likely to deliver strong long-term results than one riddled with unnecessary risks and excessive costs.

Common Investment Pitfalls:

- Chasing Performance – Investors often move money into assets that have recently performed well, only to see them falter. Buying high and selling low is a wealth-destroying cycle.

- Overtrading – Frequent buying and selling not only incurs high transaction costs but also disrupts long-term compounding.

- Market Timing – Attempting to jump in and out of markets often leads to missing the best-performing days, significantly reducing long-term returns.

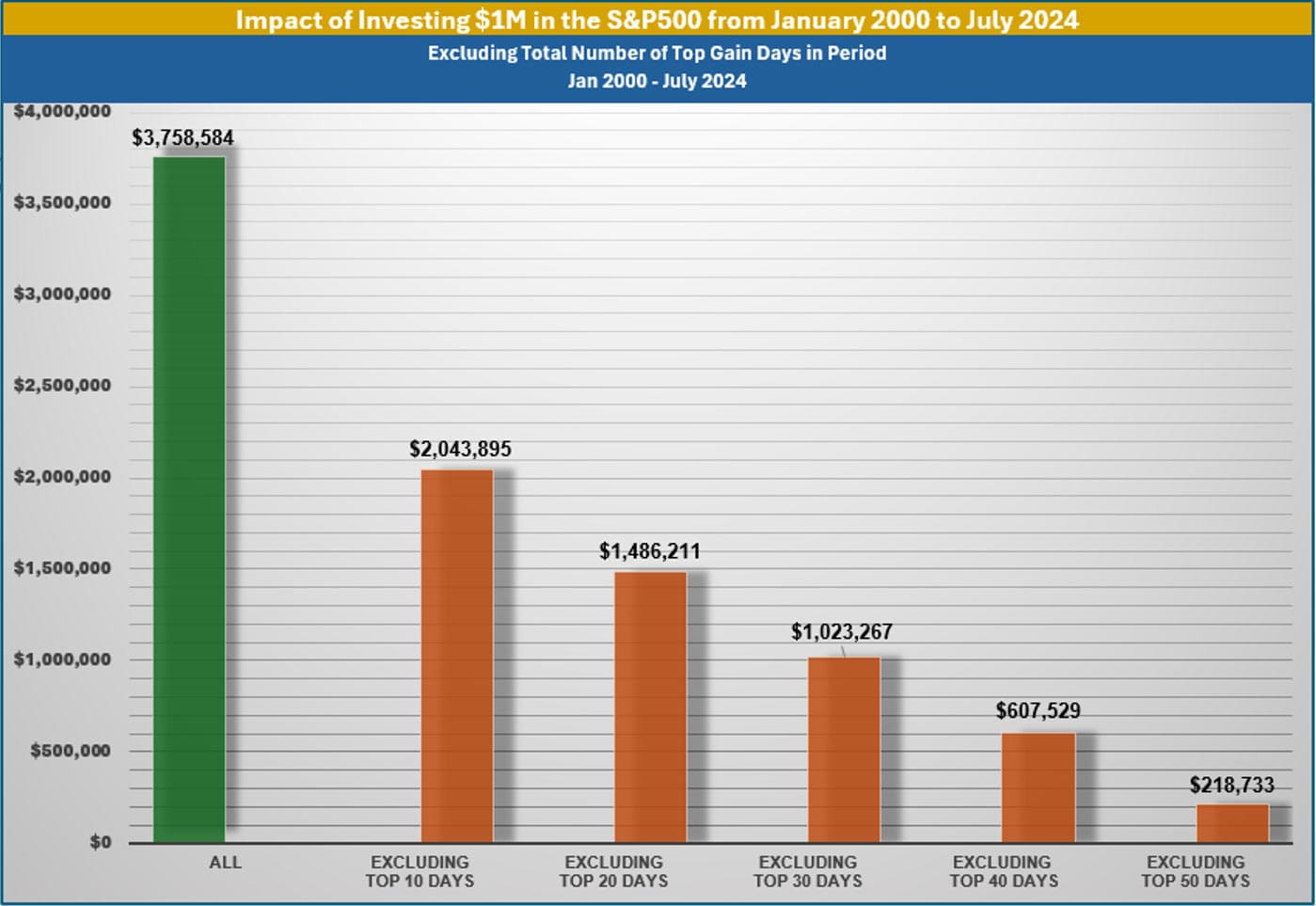

Exhibit 1 (Source: Factset, S&P)For example, an investor who stayed fully invested in the S&P 500 from 2000 to 2024 would have earned an annualized return of around 6%. However, missing just the 10 best days during that period would have cut that return nearly in half. Instead of attempting to time the market, disciplined investors stick to their plan and ride out volatility.

- Ignoring Fees and Hidden Costs – Many investors fail to realize how high-fee mutual funds, excessive advisory costs, and poorly structured portfolios can erode their long-term wealth.

The Fix:

Building an efficient portfolio requires discipline. Investing in high-quality companies, spreading risk, and minimizing costs through tax-efficient strategies and low-fee investment vehicles can significantly improve long-term results. Staying invested, rather than reacting to short-term market swings, is critical to achieving sustained growth.

Pillar Three: Time – The Most Powerful Ally

The final – and often most underappreciated – element of wealth-building is time. Even a high-income earner with solid investment returns will struggle to build significant wealth without giving their investments time to grow. Compounding is the force that turns small, consistent contributions into a sizable nest egg over decades.

Common Time-Related Pitfalls:

- Impatience – Many investors expect rapid results and abandon solid investment plans if they don’t see immediate gains.

- Starting Too Late – The later one begins saving and investing, the more aggressive they must be to reach their goals.

- Panic Selling – Market downturns are inevitable, but investors who sell in fear often lock in losses and miss out on subsequent recoveries.

The Fix:

Time in the market is far more important than timing the market. Starting early, staying invested, and allowing compounding to work over decades is the surest path to wealth. Investors must resist the urge to react emotionally to short-term volatility and remain focused on their long-term financial goals.

The Interplay Between Behavior and Success

While the three pillars of wealth-building are fundamental, investor behavior is the thread that holds them together – or tears them apart. The most well-structured financial plan can be undone by reckless spending, emotional decision-making, and a failure to stay the course.

Other Destructive Investment Behaviors to Avoid:

- Overconfidence – Believing one can consistently outperform the market often leads to excessive risk-taking.

- Neglecting Professional Guidance – A skilled advisor can help navigate market volatility and behavioral pitfalls, yet many investors make major financial decisions without expert input.

- Failure to Rebalance – Portfolios must be periodically adjusted to ensure that risk is being spread across enough asset classes and sectors.

Conclusion: Wealth Is Built Through Discipline

There is no secret formula to financial success – wealth-building is simply a matter of consistently saving, investing wisely, and allowing time to do the heavy lifting. However, the greatest challenge is not the market itself, but rather an investor’s ability to avoid the self-inflicted wounds of poor financial behavior.

By prioritizing savings, constructing an efficient portfolio, and committing to a long-term perspective, investors can maximize their financial potential. But none of this works if reckless spending, panic-driven decision-making, or performance-chasing undermine the plan. Financial success is not just about having the right investments – it’s about having the right behaviors to see the plan through. Those who can master their emotions, exercise discipline, and stay the course will be the ones who achieve lasting financial security.

Related Articles

Planning and Behavior: Why Even the Best Financial Plan Can Fail

Personal Finance,

March 28, 2025

How Can I Develop Good Investment Behavior?

Personal Finance,

Top Personal Finance FAQs,

February 11, 2025

How does FOMO negatively impact my investment results?

Investment Principles,

Personal Finance,

Top Investor Mistakes,

Top Personal Finance FAQs,

January 8, 2025