When it comes to investing, asset allocation is one of the most critical decisions you can make. It defines the mix of stocks, bonds, cash, and other investments in your portfolio. But once you’ve set your allocation, how often should you change it?

The simple answer is: not as often as you’d think.

The Importance of Your Advisor’s Skill and Experience

The skill and experience of your financial advisor or planner play a crucial role in setting an effective asset allocation. A knowledgeable advisor will consider your financial goals, risk tolerance, time horizon, and market conditions to create a balanced and strategic allocation. Their insights can help you avoid emotional decision-making and ensure your portfolio is built for the long term. Relying on an experienced professional from the outset increases the likelihood that your allocation will serve you well through various market conditions.

Changing allocations to fit a portfolio model can penalize strong asset classes while rewarding weak ones. Because asset classes move between periods of dominance and weakness over cycles lasting several years, changing allocations too frequently can mean leaving strong assets before the rally is over in favor of adding to weak positions. For example, large-cap stocks performed very well from 2019-2024. If you rebalanced every year, you might have missed out on the latter parts of this rally. Constant shifting can clip the wings of your dominant asset class.

You may be thinking: isn’t selling in strength and buying in weakness what experts say to do? Not always! Historically it is impossible to know when an asset class that is lagging will become dominant, or when the dominant asset class will become a lagger. Sometimes an asset class can be a lagger for years, as is the case recently for international and emerging markets. Leaving the dominant asset class for a laggard for the sake of maintaining an allocation can hurt long-term results.

Waiting for the Market to Come to You

Changing your allocation isn’t necessarily a bad thing, but real wealth is always built on the principles of investing in good companies, spreading risk, and letting time be your friend. It is about time in the market, not timing the market. When you allocate between quality stocks of different sectors, and spread your risk across equities and fixed income, you are buying quality and spreading risk. The only other ingredient needed for success is patience! Changing your allocation too often may not reduce risk and will most likely hurt results. Let the market come to you!

Changing your allocation isn’t necessarily a bad thing, but real wealth is always built on the principles of investing in good companies, spreading risk, and letting time be your friend. It is about time in the market, not timing the market. When you allocate between quality stocks of different sectors, and spread your risk across equities and fixed income, you are buying quality and spreading risk. The only other ingredient needed for success is patience! Changing your allocation too often may not reduce risk and will most likely hurt results. Let the market come to you!

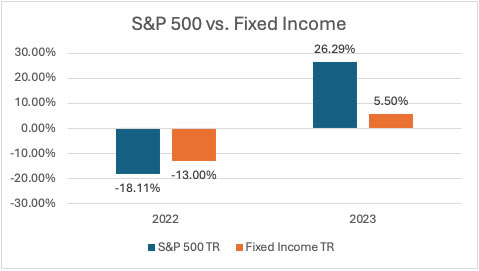

Let’s look at an example. In 2021 bonds were down -1.5%. If your allocation was 60/40 at the beginning of the year, by the end of the year you would need to move more to bonds because the stock market grew so much. You would be selling the asset class that recently performed well, like large-cap stocks which returned 28.7% in 2021 and buying the asset class that recently performed poorly (bonds). Unfortunately, the Federal Reserve increased interest rates 11 times between March of 2022 and July of 2023, which caused fixed income prices to decline by -13% in 2022. By the end of 2022 you’re worse off because you fed an asset class that moved down significantly. In this case you are focusing too much on allocation, rather than letting the markets settle and work themselves out.

5 Reasons You May Want to Let the Market Settle Rather Than Chasing An Allocation

- When you own bonds directly and the bond market moves down, that doesn’t change the outcome of the bond unless it fails. If one owns bond directly (not in a bond fund) and the market moves down, it affects the value of your bonds and therefore your allocation. However, while the value of your bonds has decreased, the coupon payments and payment at maturity have not.

- Changing allocation based on short-term market fluctuations means that you’re not allowing the markets to settle. For example, the decline in bonds in 2022 would make your portfolio seem heavily weighted towards equities, but the 2023 bond rally would bring that allocation back in line with your allocation.

- Changing allocation too often can hurt the performance of the portfolio.

- Advisors changing the allocation based on a model portfolio can create unwanted capital gains.

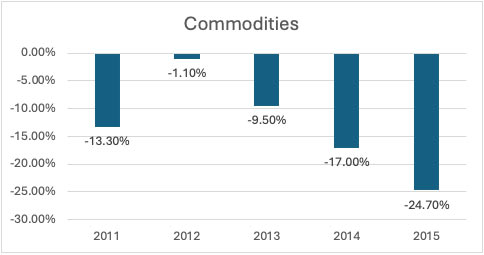

- May reward asset classes that lag for years, like in the case of commodities. Some retail advisors that use model portfolios adjust the allocations regularly but may be feeding a weak asset class for years and not considering what it does to the portfolio results.

S&P 500 total return. Fixed Income total return is Bloomberg U.S. Aggregate. It is not possible to invest directly in an index.

As you can see from the above chart, if you had kept adding to commodities to maintain your initial allocation, you’d be feeding a weak asset class.

When Should You Change Your Asset Allocation?

You should only reconsider your asset allocation when there’s a meaningful change in your personal circumstances or financial goals. Here are some key moments that may warrant a shift:

- Life Stage Changes: If you’re nearing retirement, your risk tolerance and need for liquidity will likely shift. An allocation suited for wealth accumulation may need to be adjusted to preserve capital and generate income.

- Changes in Risk Tolerance: Sometimes your comfort with risk changes due to major life events or shifts in personal outlook. If your risk tolerance decreases or increases significantly, your asset allocation should reflect that.

- Financial Goals Evolve: Perhaps you’re planning to buy a house, fund a child’s education, or take an early retirement. As your financial goals change, your allocation may need to be rebalanced accordingly.

- Significant Income Changes: A major change in your income–such as a job loss, promotion, or inheritance–could alter your capacity to invest or your need for financial stability.

Conclusion

Changing or adjusting your allocation is not necessarily a bad thing, especially if your risk tolerance, growth and income needs, or time horizon changes. However, it is not necessary to change your allocation every time your portfolio is underperforming. After three decades of managing money, we’ve seen sectors rotate for dominant to weak, and from weak to dominant. Sometimes it’s better to let time and the market do the work. Remember, timing the market usually doesn’t work, while time in the market does!

Related Articles

Building a portfolio with a correction in mind vs timing the correction

Investment Principles,

Markets,

Portfolio Considerations,

October 1, 2024

The Power of Diversification: How Different Asset Classes Complement Each Other in a Balanced Portfolio

Behavior,

Index Sectors,

Investment Principles,

Markets,

Portfolio Considerations,

September 17, 2024

The Importance of Rebalancing a Portfolio

Investment Principles,

Portfolio Considerations,

Top Investment Principles FAQs,

August 12, 2024