Making Comparisons at The Wrong Time

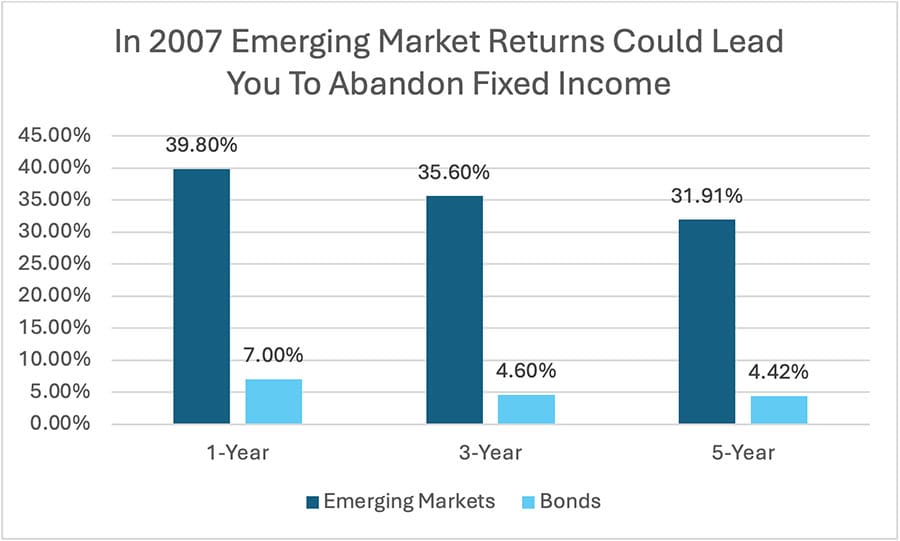

When markets are doing well, investors can forget the lessons of down-markets and unintentionally concentrate their risks. The success of an asset class, such as tech stocks or emerging markets, can make an investor with a balanced portfolio feel that they are missing out on the rally. Unfortunately, by selling their underperforming holdings to purchase the “hot” asset class, they may be selling low and buying high. The spectacular returns the investor wants have already taken place, and the investor could be buying right before the trend reverses. For instance, take a look at the average returns for emerging markets and fixed income in 2007:

Source: Zephyr. EM Equity: MSCI EME. Fixed Income: Bloomberg U.S. Aggregate. An index is unmanaged, and you cannot directly invest in an index. Past performance is no guarantee of future results.

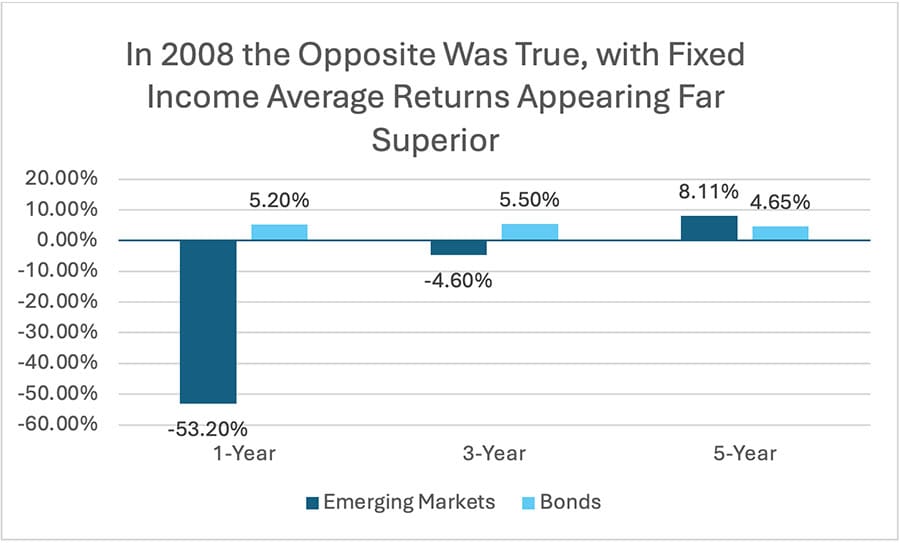

A balanced investor could see this chart and conclude they should sell their fixed income holdings to purchase more emerging markets stock. After all, emerging market stocks returned more than 27% higher over the previous five years. Unfortunately, the investor who sells their fixed income holdings to increase their emerging market allocation in late 2007 is in for a rude awakening in 2008:

Source: Zephyr. EM Equity: MSCI EME. Fixed Income: Bloomberg U.S. Aggregate. An index is unmanaged, and you cannot directly invest in an index. Past performance is no guarantee of future results.

Making comparisons between asset classes during a market rally can tempt investors to abandon traditionally conservative sectors and be more aggressive. While it can be easy to take on more risk during a rally, downturns can make investors question their risk tolerance. By holding a balanced portfolio, investors can be confident they’ll participate in sector rallies without risking severe losses when fortunes change. Down-markets can happen when investors least expect them, which makes maintaining a balanced portfolio over time critical to success and peace of mind.

Why Bond Ownership is Important in Down-Markets

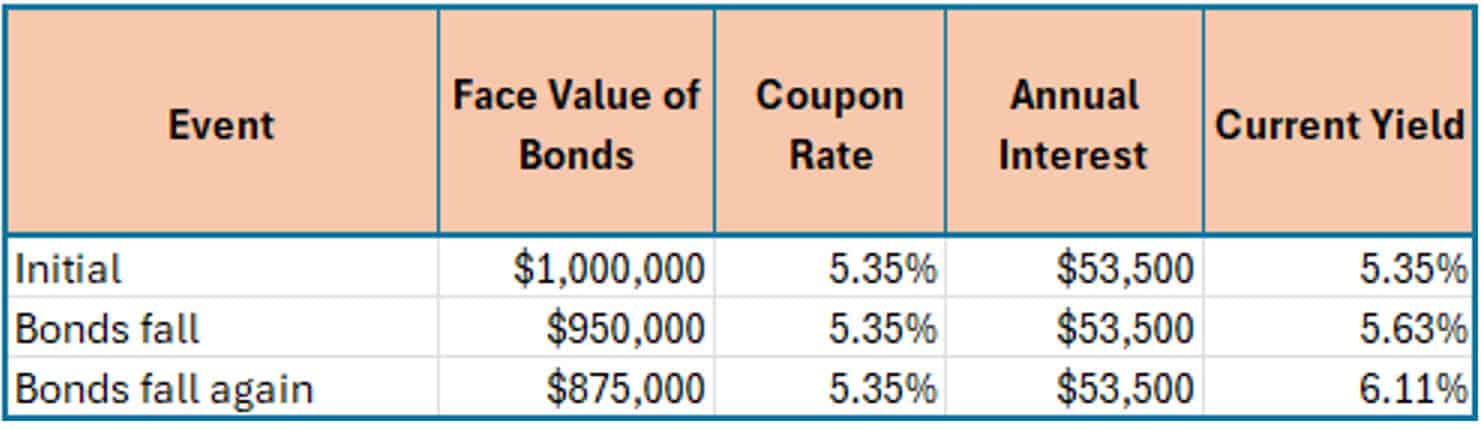

Bonds are included in most portfolios due primarily to add diversification, but having a steady stream of bond income can be a useful tool when investing. This income helps stabilize the portfolio, and during down-markets can provide a means for buying shares at lower prices. If interest rates increase, bond prices decrease, but the income from old bonds can be used to continually reinvest into bonds with higher interest rates. Even when bond prices decline, the coupon payments and payments at maturity for the bonds you already own don’t change. Bond market pullbacks give the investor the opportunity to buy more bonds with better yields, as you can see below:

These are hypothetical figures.

Down-Markets Strike When You Least Expect It

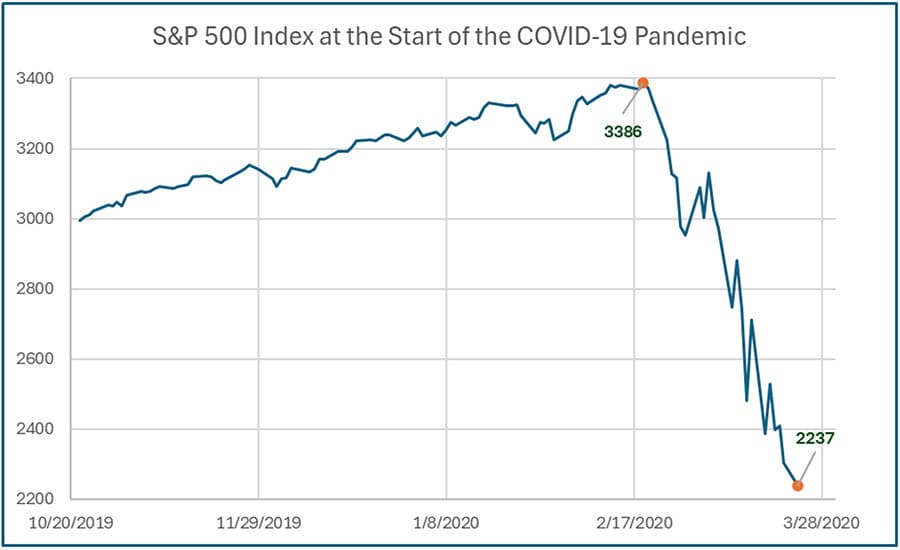

Following the lows of the Great Recession, the S&P 500 had steadily grown until 2020. Before the pandemic the U.S.’s interest rates, inflation, and unemployment figures were low, and the economy’s growth was strong. The COVID pullback caught many investors by surprise, with the S&P 500 falling over 33% in a little over a month:

Source: Zephyr. An index is unmanaged, and you cannot directly invest in an index. Past performance is no guarantee of future results.

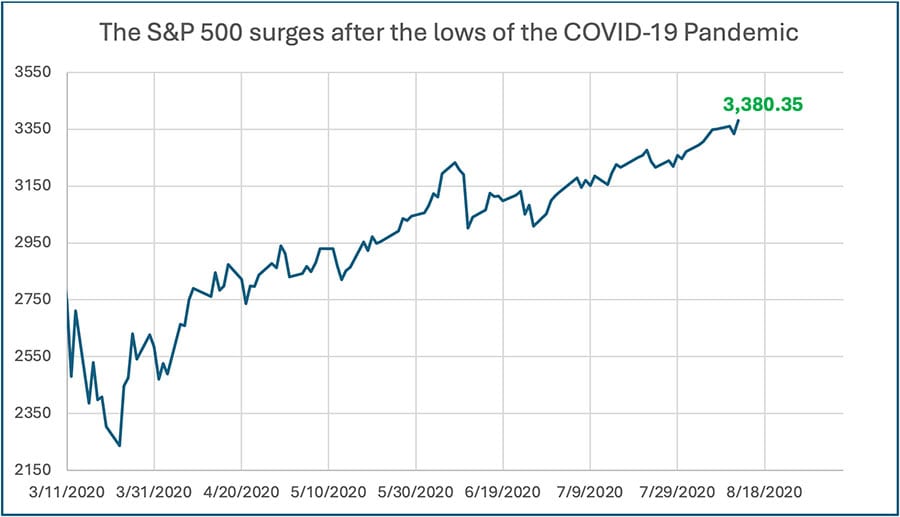

No one can predict market pullbacks and rallies with any real accuracy, and it can be equally difficult to predict the market’s recovery. The S&P 500 actually gained value in 2020, despite the severe pullback and negativity earlier in the year. Even if investors had sold their holdings at the right time, many would’ve still been on the sidelines and missed the subsequent recovery. Even as cases of COVID were continuing to increase, the market was climbing its way back:

Source: Zephyr. An index is unmanaged, and you cannot directly invest in an index. Past performance is no guarantee of future results.

Markets are notoriously hard to predict. Over the long term, the markets trend upward, with new market highs coming nearly every year. From 1961 to 2025, the S&P 500 reached an all-time high more than 1,100 times. If an investor is on the sidelines because of new highs, they may end up missing significant opportunities.

Growth and Value During Rallies & Pullbacks

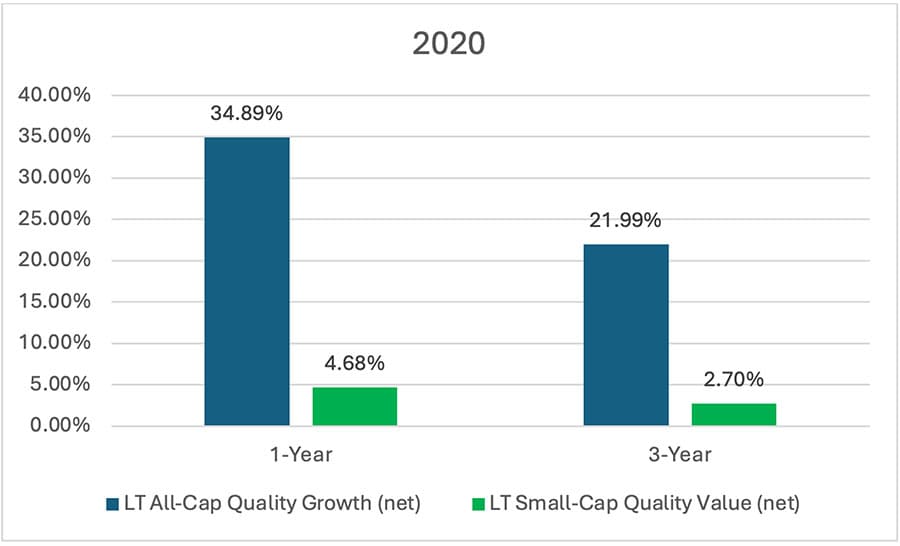

Rallies can tempt investors to leave value stocks in favor of growth stocks. Take a look at how much the Linden Thomas US All-Cap Quality Growth 150 Index outperformed the Linden Thomas Small Cap Quality Value 50 Index in the years before 2021:

Source: Zephyr. You cannot invest directly in an index.

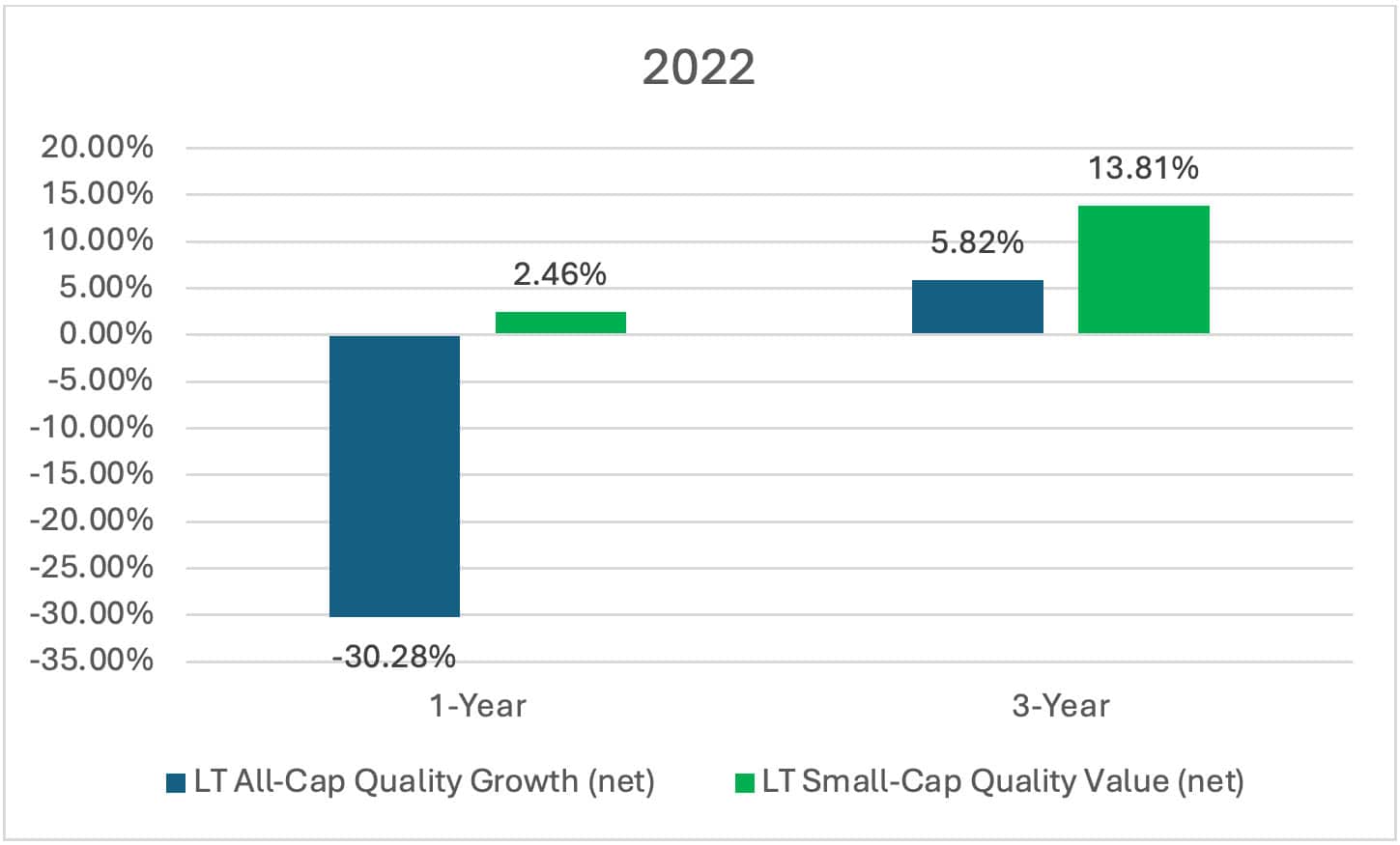

By 2022, an investor who sought greater returns by switching to the growth index would have regretted their decision, as value stocks showed greater resilience in the face of a pullback:

Source: Zephyr. You cannot invest directly in an index.

Chasing Average Returns Can Get You Hurt

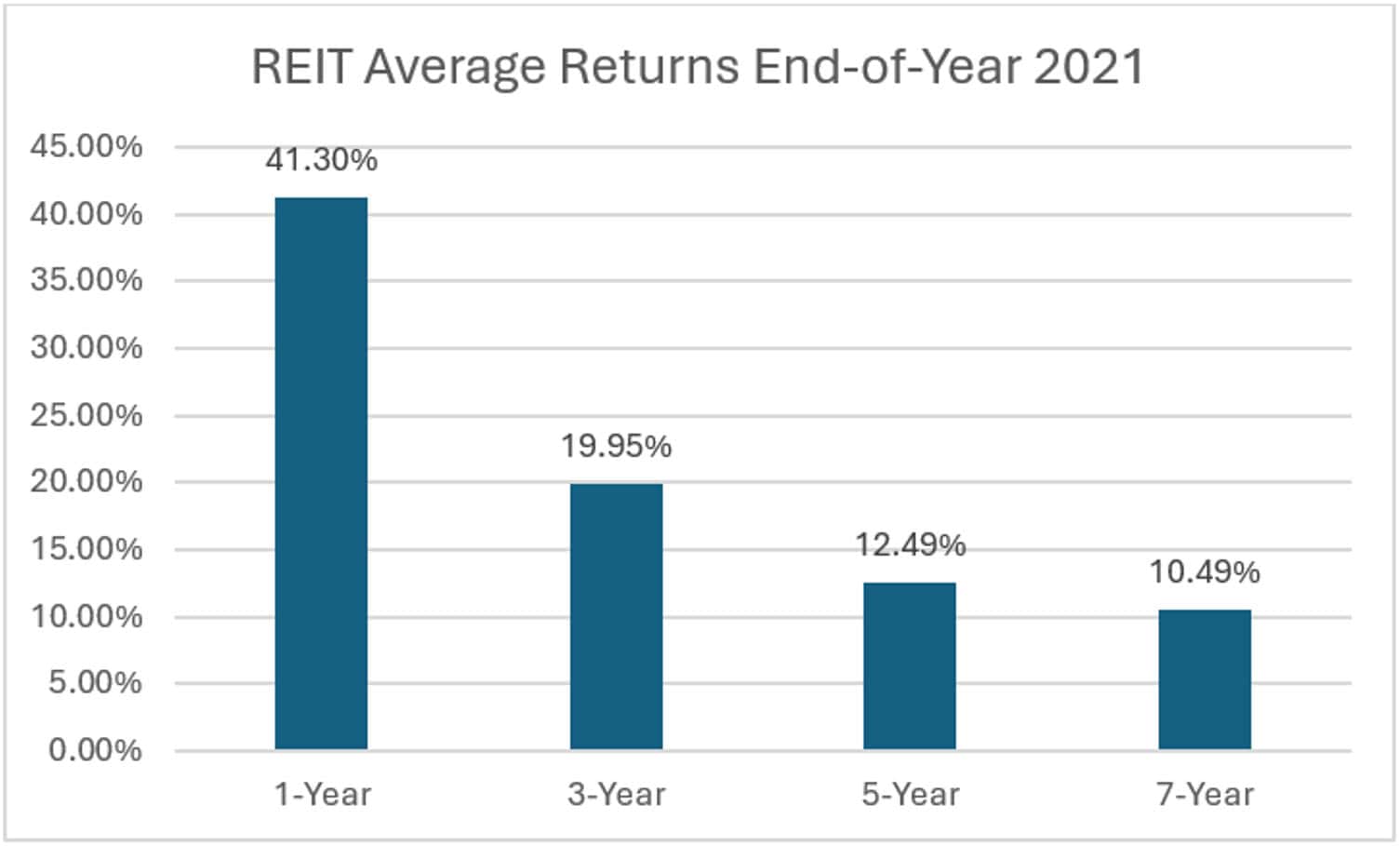

The relationship between annual and average annual returns can also feed into an investor’s bad behavior. While a single year’s results may not be enough to convince an investor to change course, the single year’s results impact the trailing averages as well. Take a look at what REITs average returns looked like at the end of 2021:

Source: JP Morgan Guide to the Markets (NAREIT Equity REIT Index)

(an index is unmanaged, and you cannot directly invest in an index)

(Past performance is no guarantee of future results)

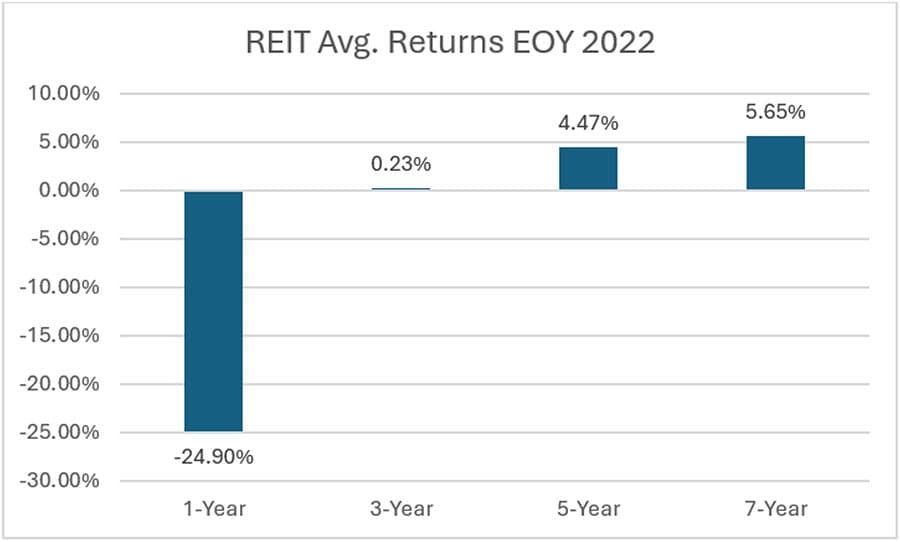

An uninformed investor could view these average returns as proof of REITs (Real Estate Investment Trusts) dominance over several years and decide to sell their other holdings to increase exposure to REITs. If the investor built their initial portfolio with a focus on diversification, quality, and direct ownership, they shouldn’t change course just because of recent results. The next year’s average returns could tell a very different story:

Source: JP Morgan Guide to the Markets (NAREIT Equity REIT Index)

(an index is unmanaged, and you cannot directly invest in an index)

(Past performance is no guarantee of future results)

It only takes one exceptional year to significantly change average returns, so investors should be cautious in changing their allocation due to short term fluctuations. All sectors have rallies and pullbacks, and full cycles can take 10-20 years to run their course.

The key is to stay diversified and avoid chasing hot sectors. During market dips, it’s often better to add to weaker-performing sectors rather than abandoning them. Quality holdings, direct ownership, and time are essential elements to successful investing. This applies not only to stocks but also to bonds, where the income from high-quality bonds can provide long-term stability, even when bond prices decline. Despite the evidence, most investors fail to realize that the best results are achieved over long periods of time. It should be no surprise that time in the market is more important than timing the market.

Related Articles

The Market Is Like a Coin—It Has Two Sides: Up and Down

Investment Principles,

Knowledge & Insights,

Markets,

Understanding Results,

September 17, 2024

Building a portfolio with a correction in mind vs timing the correction

Investment Principles,

Markets,

Portfolio Considerations,

October 1, 2024

Historical examples of hot sectors that didn’t end well

History of Markets,

Investment Principles,

Knowledge & Insights,

Markets,

Top Investor Mistakes,

July 11, 2024