By Indexopedia Research Team | January 8, 2025 | In

The quest for a “perfect allocation” can be misleading. There’s no universal formula for investing success–what works for one investor may not suit another. The ideal allocation depends on individual goals, circumstances, and tolerance for risk. Instead of chasing perfection, the focus should be on finding an approach that aligns with your unique needs.

Investors often categorize themselves as aggressive or conservative, but markets often test these labels. One could say they’re aggressive, but when the markets are down and the media is saying things will get worse, it’s tough to stomach. Seeing your portfolio going down, considering the markets may get worse, and not knowing when the recovery will take place, will test whether an investor is truly comfortable with their allocation. Likewise, when investors say they are conservative and allocate accordingly, they may wonder why everyone around them seems to be doing better when the markets are booming. This could make you want to adopt a more aggressive approach. Consider this: no matter what kind of investor you are, you will never be fully satisfied. In fact, there’s a bible verse that tells us our flesh will never be satisfied.

“The eyes of man are never satisfied.”

~ Proverbs 27:20

Knowing this, what do we do? Do we abandon trying to categorize ourselves? No, we just need to consider the worst-case-scenario before we allocate our portfolio. For example, if you’re aggressive, don’t just consider the long-term rewards of building wealth, consider the pains of getting there. You will have many down-markets, because markets are two-sided. As an aggressive investor, you may experience the worst of bad markets, and the whole time the media will be telling you it’s getting worse. As a conservative investor, you should expect others to outperform you during up-markets. The resilience of a conservative portfolio will only reveal itself during bad times. By considering the pros and cons of different allocations and your personal risk preferences, you’ll be better prepared to avoid the mistakes investors make. Poor investment behavior is often one of the biggest reasons investors achieve poor results.

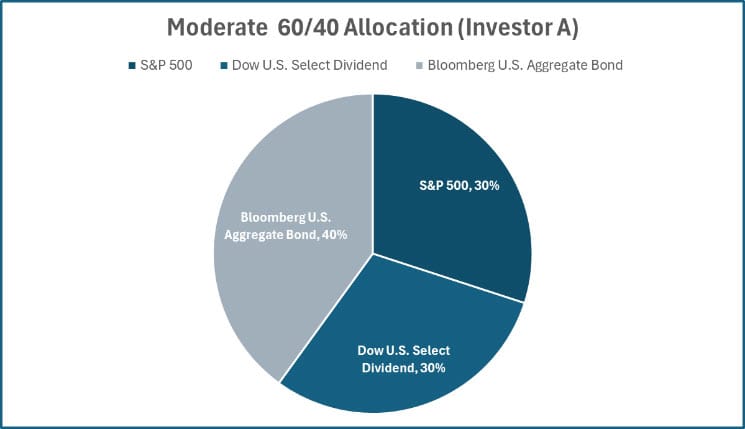

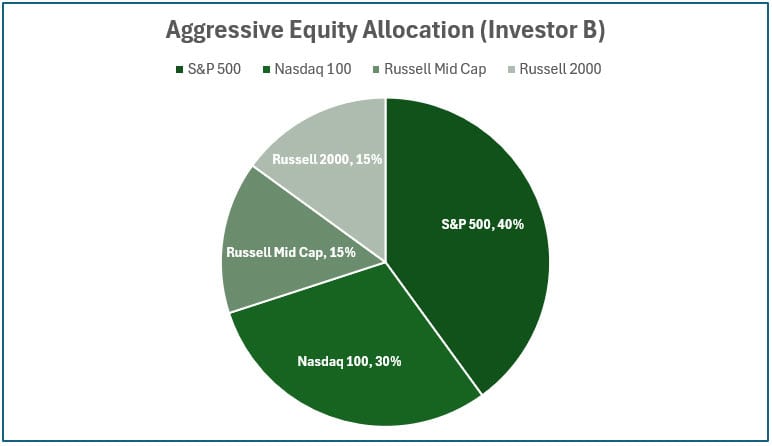

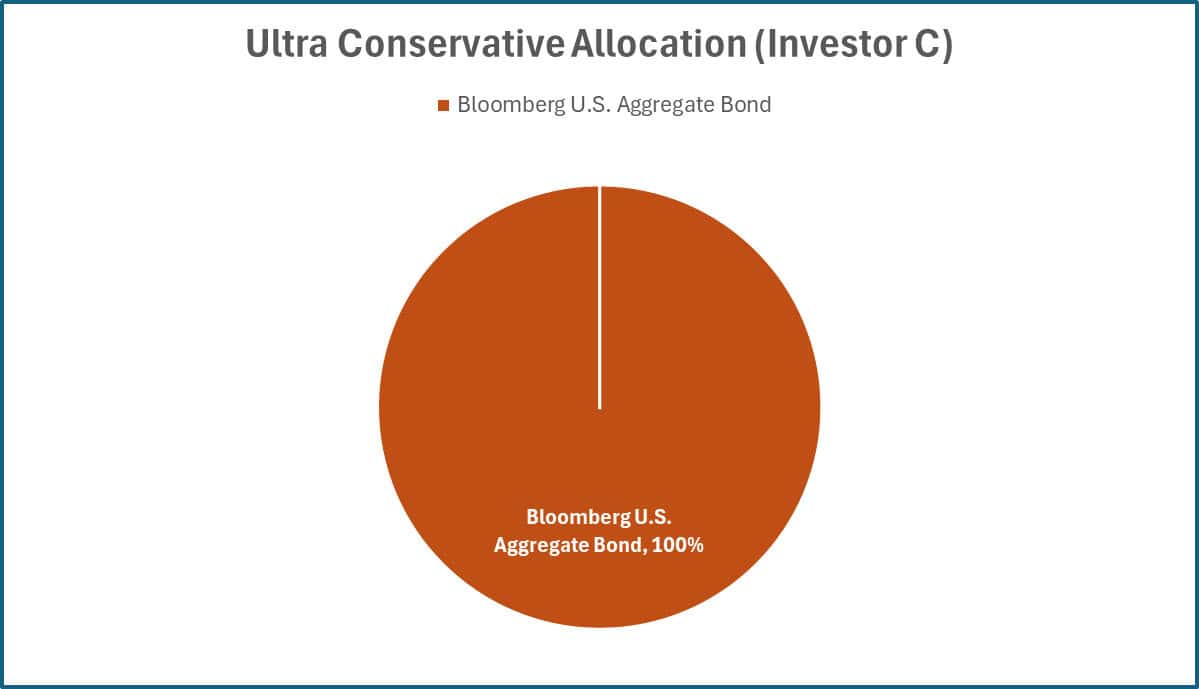

Example of 3 Portfolios

Consider three contrasting allocations: a 60/40 portfolio, a 100% equity portfolio, and a portfolio made up entirely of bonds. The 60/40 mix offers moderate growth with reduced volatility, combining 60% equities and 40% fixed income. In contrast, a 100% equity portfolio targets maximum growth but entails higher risk. On the other end of the spectrum is the 100% bond portfolio which exhibits lower risk and correspondingly a lower return. Each has strengths and weaknesses, and their suitability depends on your goals, time horizon, and ability to weather market fluctuations. See their allocations below:

Over the long term, the growth potential of different allocations becomes evident. Starting with a $2 million investment in March 2000, the aggressive 100% equity portfolio grew to $11.64 million by March 2024. Meanwhile, the defensive 60/40 portfolio reached $9.21 million over the same period. Using the ultra conservative allocation, the original $2 million investment would have grown to just over $5 million. While a 100% bond portfolio had the lowest return over this period, it made steady progress and didn’t experience the same volatility. These results demonstrate the potential for higher returns in a more growth-focused strategy, while still showing significant gains from a balanced approach.

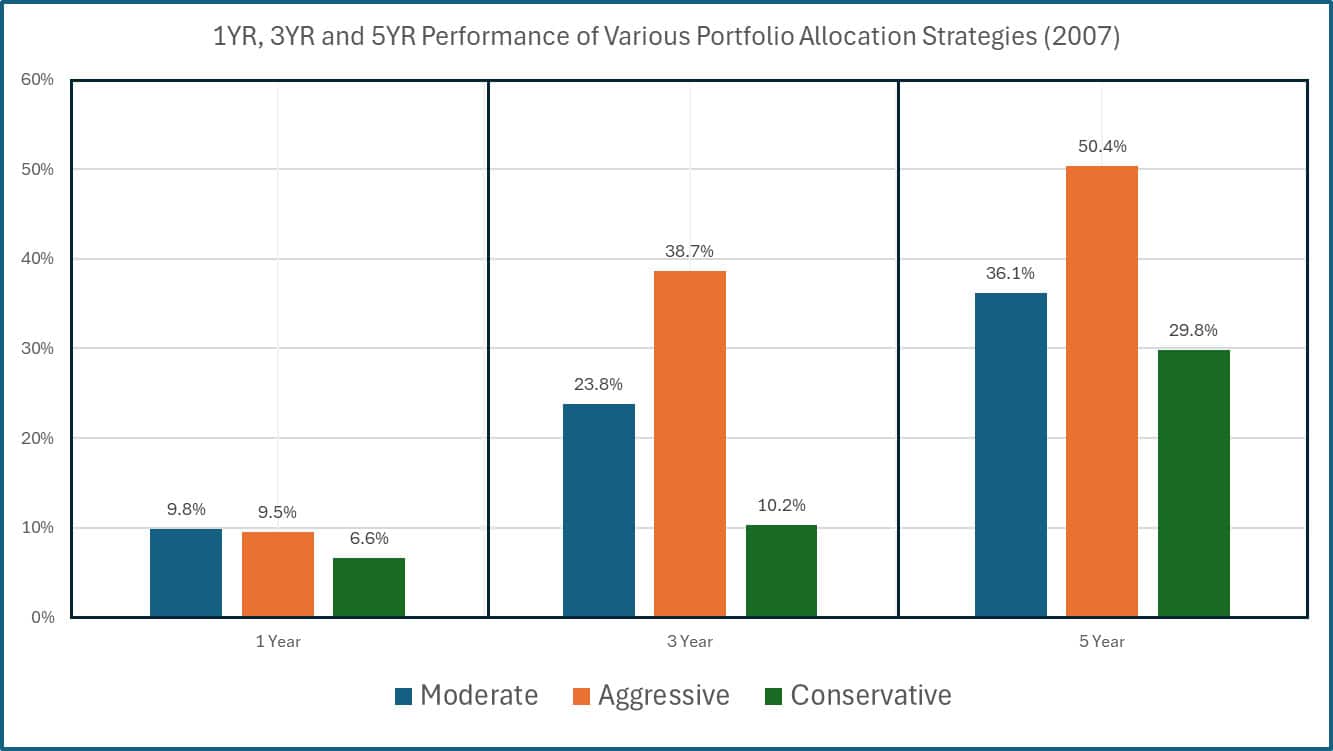

If the investor wasn’t thoughtful about their risk tolerance when allocating, they might have had second thoughts about their strategy. In March of 2007, bond (conservative) investors might think they are missing out when seeing these average returns:

*Measured 3/31/2007.

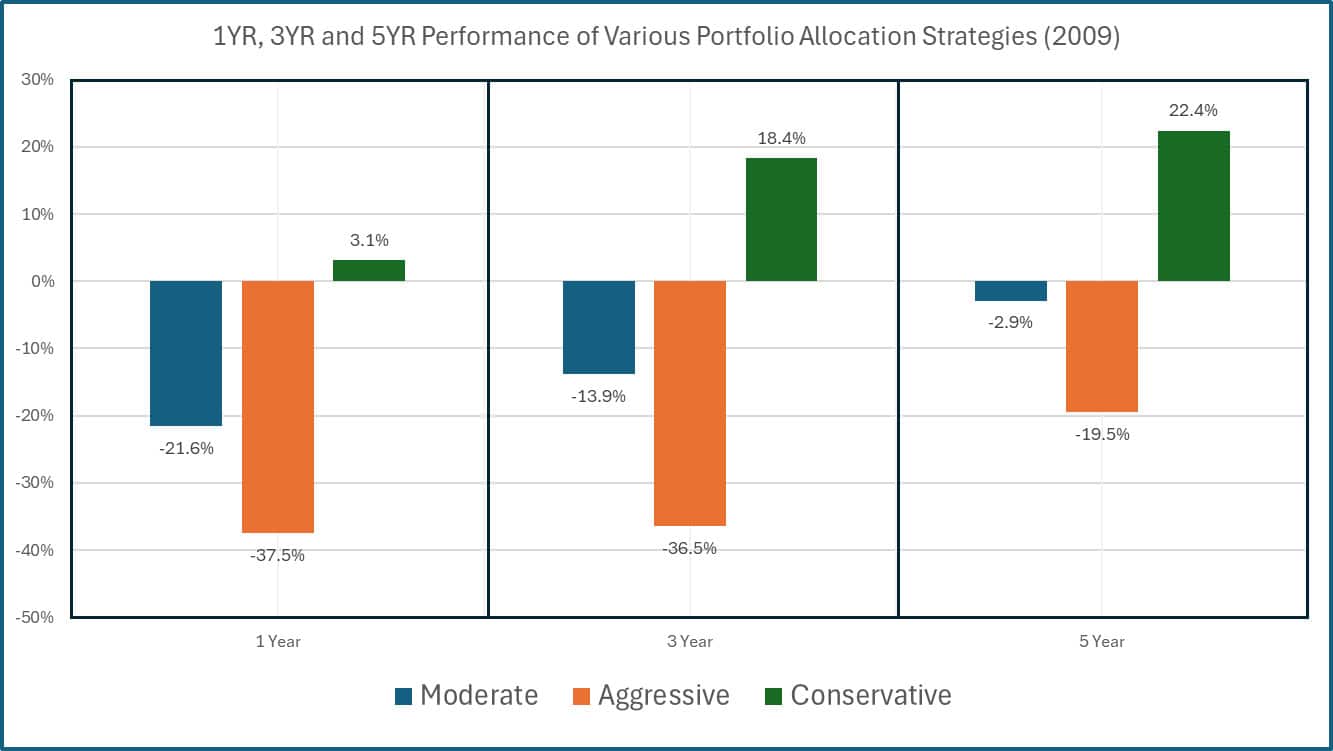

Some of these investors might have considered switching to a 60/40 allocation or even 100% equity. But two years later, they would be thankful they stuck to their conservative portfolio:

*Measured 3/31/2009.

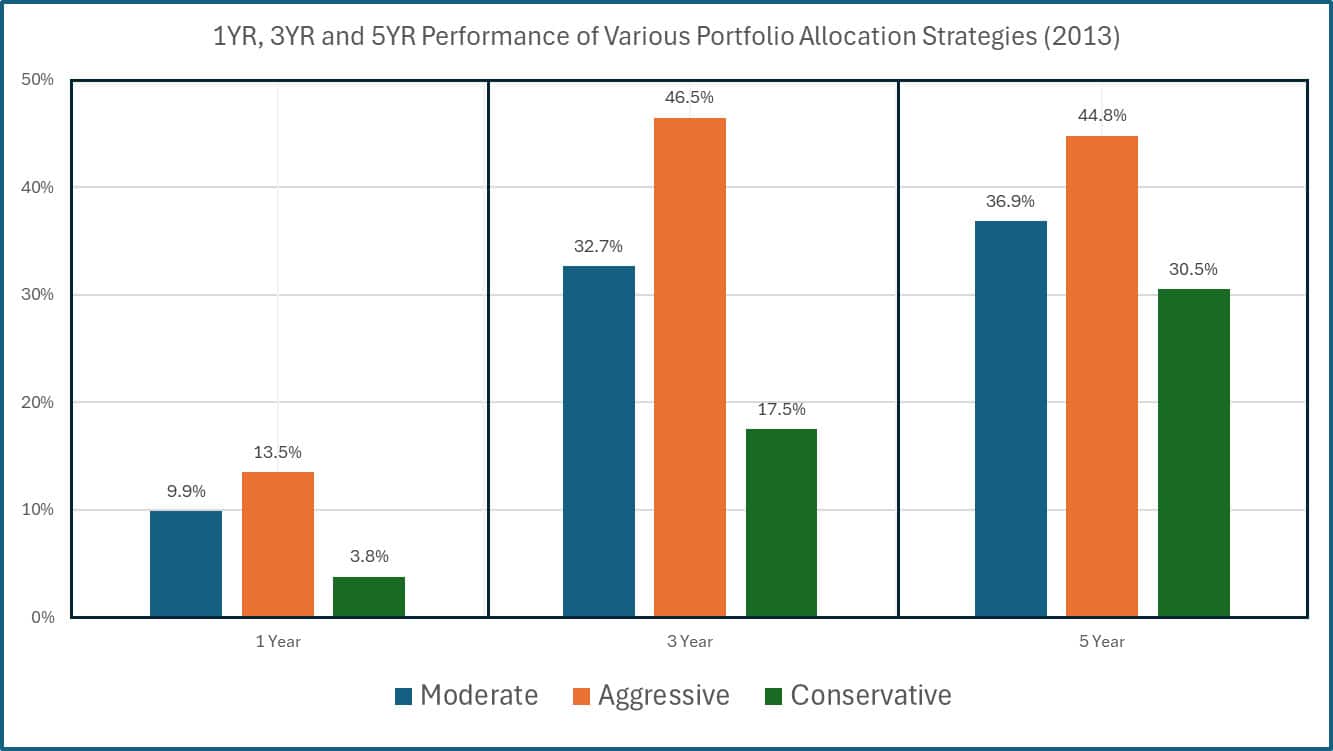

Aggressive investors could look at the chart above and decide to be more conservative, selling their equities at a loss to buy more bonds. This type of behavior can also be a mistake. By 2013 they might be regretting having made the change and fear of missing out on equity returns drives them to change courses again:

*Measured 3/31/2013.

Between September 2007 and March 2012, the moderate 60/40 portfolio lost less value and even outperformed the aggressive 100% equity portfolio, while the ultra-conservative 100% bond portfolio outperformed both (in fact, this portfolio actually gained value throughout the duration of the crisis). While the aggressive allocation eventually recovered and delivered higher long-term returns these difficult years highlight the emotional and financial strain that investors may face.

Investors must also consider their time horizon and income needs when determining asset allocation. A 30-year-old with adequate savings might be okay with the aggressive portfolio’s losses during the banking crisis, since there is still plenty of time to recover value. A retiree that is dependent on the income from their portfolio to pay living expenses might find themselves in a tight spot. Being forced to sell assets at a discount is a recipe for financial disaster.

No Right or Wrong Answer

When it comes to portfolio allocation, there is no universally correct choice–what matters most is being honest about your own needs and limitations. Risk tolerance isn’t just about how much risk you think you can handle; it’s about accepting both the advantages and disadvantages of your chosen allocation. For example, a higher-risk portfolio often offers greater long-term growth potential but demands the patience to endure steep declines, while a conservative portfolio may provide stability but could underperform during market rallies. Allocation decisions should not be based solely on age or conventional wisdom but should reflect a thoughtful assessment of your risk tolerance, income needs, investment timeline, and personal goals. The right allocation is one that aligns with your ability to stick to the plan, no matter the market conditions.

Chasing the results of a single asset or portfolio is a recipe for disaster. The results you’re looking at are already in the past, and so you may be buying high and selling low. It’s better to build a portfolio that is prepared for various market conditions, and then stick to the plan.

Finding the right portfolio allocation is deeply personal and requires a clear understanding of your financial goals, emotional resilience, and long-term priorities. It’s not about chasing an ideal mix or adhering to one-size-fits-all strategies, but about crafting an approach that you can commit to through market highs and lows. By embracing an allocation that reflects your unique circumstances and risk tolerance, you can build confidence in your plan and stay focused on what matters most–achieving your financial objectives.

Related Articles

Rose Colored Glasses: Why Investing During the Good Times Can Create Poor Allocation Tilts

Investment Principles,

Top Investor Mistakes,

March 6, 2025

What does Age have to do with Asset Allocation?

Investment Principles,

Personal Finance,

Top Personal Finance FAQs,

October 23, 2023

How Often Should I Change My Asset Allocation?

Personal Finance,

Top Personal Finance FAQs,

January 8, 2025