Pooled index funds have become very popular over the last three decades. This is due in part to the ease of access it provides small investors who want a diversified basket of stocks for a low initial investment. While pooled index funds and ETFs (exchange-traded-funds) may be appropriate for small investors, there are a few considerations affluent investors should keep in mind before using these products.

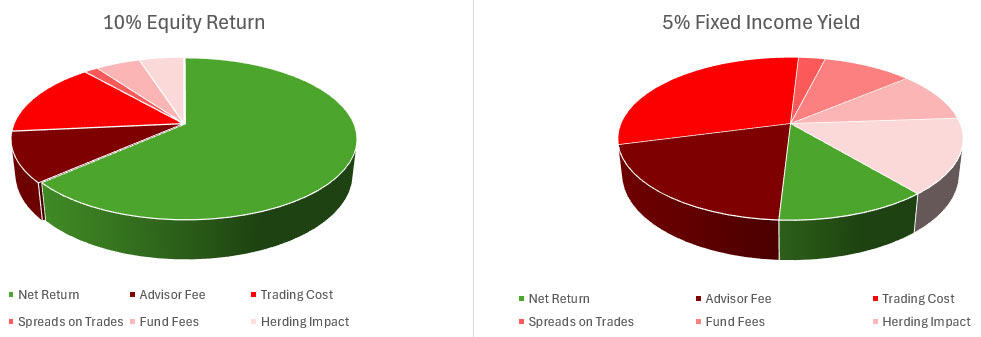

Index funds have several drawbacks due to their pooling of different investors’ funds. It’s important to understand these disadvantages before investing in a pooled index fund product. The chart shows below how these disadvantages can impact the investors results with a market-cap equity fund or a pooled bond fund:

Hypothetical Illustration of Pooled Funds’ High Cost

*Fees and cost are hypothetical and not reflective of any specific cost associated with a particular fund.

A brief explanation of these costs can be found below:

Investment Advisor Fee:

Advisors charge a fee for asset allocation or portfolio construction, but simply invest their clients into mutual funds or ETFs that the advisor has no part in constructing or managing. This effectively means the investor is paying two levels of fees on the same assets.

Internal Trading Costs:

Also known as turnover costs, these expenses arise from the buying and selling of securities within a pooled fund’s portfolio. Mutual funds and ETFs with higher turnover ratios have higher internal trading fees, as more frequent buying and selling of securities leads to increased transaction costs.

Spreads on Trades:

The spread is the difference between the bid price (the price at which someone is willing to buy a security) and the ask price (the price at which someone is willing to sell a security). The fund may be selling assets for less than an individual investor would, and buying assets for more than an individual investor would, due to the typically large size of each trade. The result is a drag on the fund’s performance.

Pricing Disadvantages:

These typically exist in pooled bond funds and pooled balanced funds. Pricing disadvantages happen when the pooled funds purchase bonds in the years prior to an investor’s entry into the fund. The bonds will have high prices and low yields-to-maturity, meaning that the investor is achieving low net-cashflow results. After the fund’s expenses and the investment advisor costs, there may not be much left over for the investor.

Fund Fees:

Also known as expense ratios, these cover costs for a pooled fund’s portfolio management, administrative costs, marketing expenses, legal fees, custodial services, and other operational overhead. Essentially, the expense ratio covers the costs of running the pooled fund and is deducted directly from the fund’s assets. The expense ratio is expressed as a percentage of the net asset value and is available for all public pooled funds. Many investors are shocked to learn that the expense ratio doesn’t include internal trading costs and herding impacts.

Herding Impacts:

As small investors move into and out of the pooled fund every day, it creates more costs as positions may be sold to fund redemptions. Oftentimes, this leaves fund managers hostage to small investor behavior, requiring them to maintain a stockpile of cash to fund the redemptions. This cash earns very little return but is still subject to the expense ratio and other pooled investment costs.

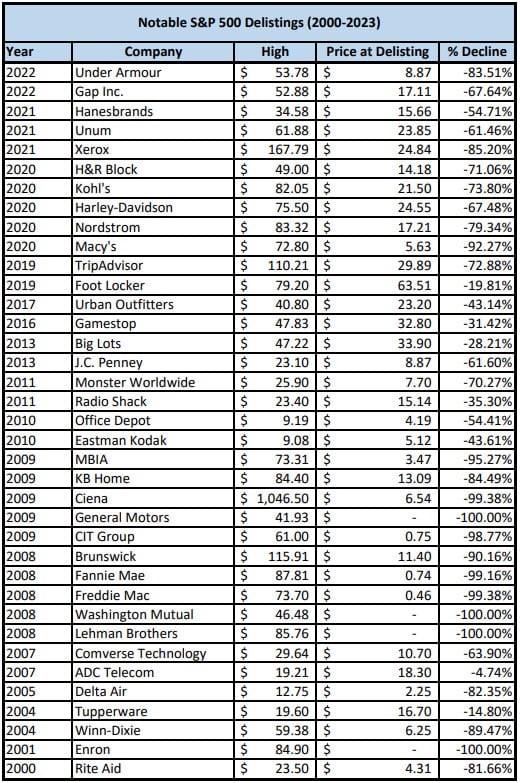

Delistings:

Delistings, or the removal of stocks from an index, can have a considerable impact on pooled index funds’ performance. A company can be delisted from an index for several reasons, such as a merger, acquisition, bankruptcy, or failure to meet listing requirements. When a shrinking company falls below the requirements it is removed from the index, and any losses are realized. Since companies are included based on their size, rather than their quality, many companies aren’t removed from an index until after investors have suffered losses. There have been dozens of examples of this over the years, as can be seen in the below chart:

While these costs directly impact returns, there are advantages to institutional direct beyond just reduced costs:

Tailored:

Direct indexing provides a higher degree of customization. Like a tailor adjusts a suit to fit its wearer, investors can build tailored portfolios and exclude specific stocks or incorporate personal preferences (like excluding tobacco stocks, for example). By building the portfolio focused on the investor’s income needs, time horizon, and risk tolerance, institutional direct indexing can help achieve investor goals.

Transparency:

Unlike pooled mutual funds, institutional direct indexing gives affluent investors total control and total transparency, allowing them to make the choices that best meet their needs. Combined with the ability for customization, transparency into performance and holdings allows investors to make informed decisions about what changes might be needed in their portfolio.

Control:

Institutional indexing isn’t built by pooling investors’ assets, instead each investor owns and controls their stocks directly. Indexing with individual equities means that investors are not hostages to small investors’ bad behavior. With direct indexing, investors can take advantage of down-markets by adding to positions at lower prices. Institutional direct investors aren’t “along for the ride” with other investors who may be generating increased trading fees and phantom taxes through their constant movement into and out of the fund. This level of control can also lead to increased tax efficiency, by providing the ability to harvest tax losses or gift appreciated shares.

Voting Proxies:

As a shareholder, you have certain rights, including the right to vote on important matters that affect the company’s future. Shareholders can give a proxy explicit instructions on how to vote on specific issues or give their proxy discretionary authority to vote as they see fit. By appointing a proxy, shareholders can ensure that their vote is still counted and that their voice is heard. Additionally, proxy voting can also help to promote transparency and accountability in corporate governance by giving shareholders a say in how the company is run.

Ability to Screen for Quality:

While many of the most popular index funds select holdings solely based on the size of a company, institutional direct indexing can be used to create indexes screened for quality. This means instead of buying companies just based on size, you can select the best companies from each sector. This ability can increase upside and downside capture, and ultimately result in more return to the investor.

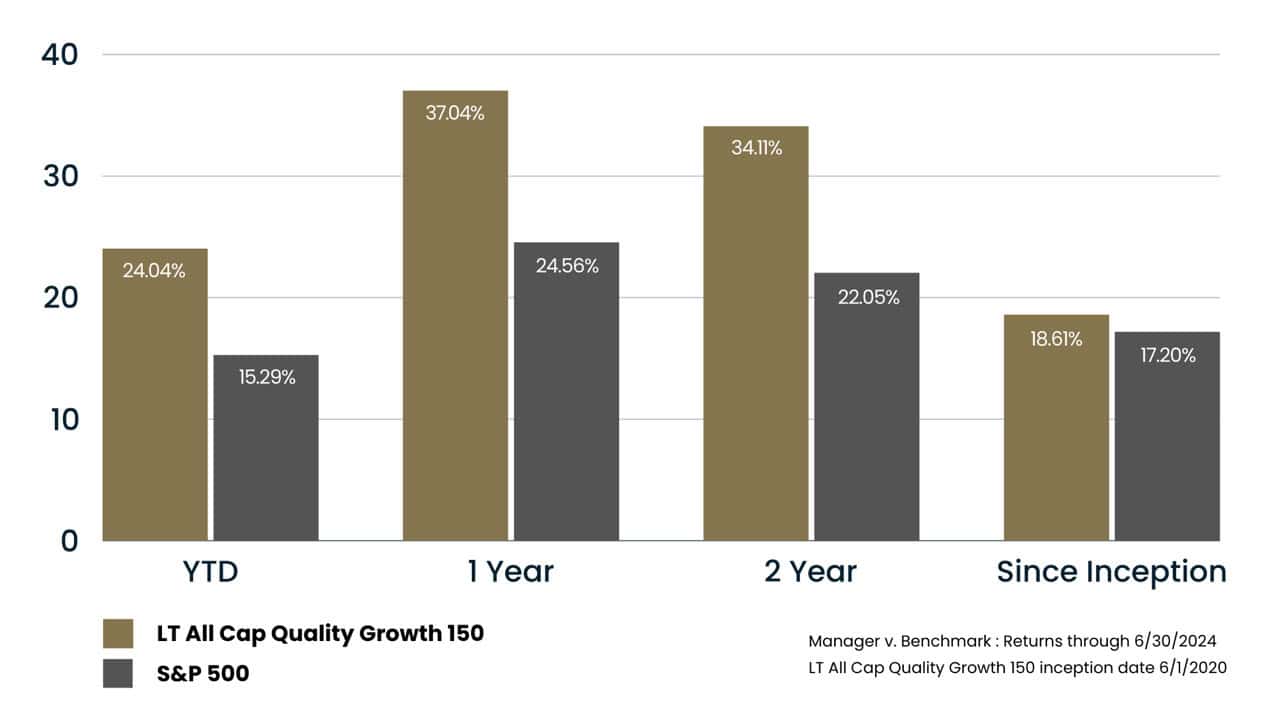

While pooled index funds aren’t a bad investment for small investors, Institutional Indexing with tailored portfolios has offered more efficiency with better results over time. Below shows the Linden Thomas All-Cap Growth 150 compared to the S&P 500, a market-cap index:

Pooled funds provide instant diversification and simplicity, making them suitable for small investors. On the other hand, institutional direct indexing offers customization, potential tax advantages, and the ability to align investments with personal values. It is more suitable for investors with larger portfolios who seek greater control. Ultimately, the choice between these two approaches depends on an individual investor’s goals, preferences, and circumstances. However, overall institutional direct is built for the individual, while retail indexing is built for the institution.

Disclosures:

The performance results shown are those of a proprietary account at Linden Thomas invested using real dollars based upon the application of Linden Thomas’s Proprietary Linden Thomas All Cap Quality Growth 150 Index and include a .85% advisory fee. The performance does not reflect the deduction of other fees or expenses, including but not limited to brokerage fees, custodial fees, fees and expenses charged by other investment companies, and any other fee or expenses a client may incur in the management of such client’s investment advisory account. The return with respect to an investment would be reduced by any fees or expenses a client may incur in the management of its investment advisory account. The performance results are unaudited and are not an estimate of any specific investors’ actual performance, which may be materially different from such performance depending on numerous factors. No representations or warranties whatsoever are made by Linden Thomas or any other person or entity as to the future profitability of an investment account or the results of making an investment. Past performance is not a guarantee of future results.

The S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. Past performance of an index is not an indication or guarantee of future results. It is not possible to invest directly in an index. All information provided by S&P Dow Jones Indices is impersonal and not tailored to the needs of any person, entity or group. Exposure to an asset class represented by an index may be available through investable instruments based on that index. The market index is unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

Related Articles

What is the real cost of index funds?

Index Investing,

Top Index FAQs,

Types of Indexes,

October 21, 2024

Should Affluent Investors Invest in Index Funds?

Index Investing,

Indexing for the Affluent,

Top Index FAQs,

October 21, 2024

What is the Difference Between Market-Cap Index Funds and Equal Weighted Index Funds?

Investment Principles,

November 19, 2024